Get up to speed on the fall 2019 card brand updates and how they may affect your business

The fall 2019 card brand changes will likely have little to no impact on your business financially; however, they may impact your operations and back-end acceptance processes. If you have questions or would like to discuss the changes in further detail, please contact your Redbridge advisor.

1. Visa

1.1.1 Visa deferred authorization indicator

This is not a new category. Rather, Visa has changed the timeline. Authorizations that are deferred must be identified as deferred.

- April 2019: Deferred authorization indicator is optional for acquirers and merchants

- October 2019: Acquirers must be able to support the indicator if submitted by merchant

- April 2021: Acquirers and merchants are required to send the deferred authorization indicator on all deferred authorization requests

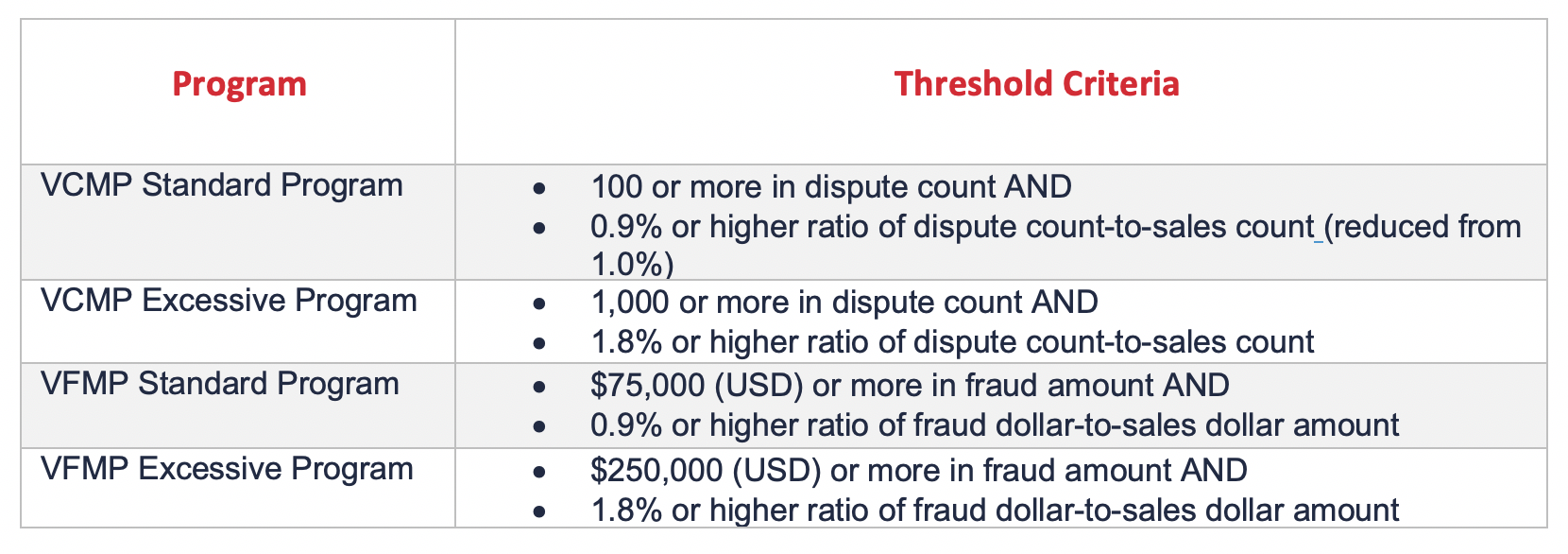

1.1.2 Visa monitoring programs

Effective October 2019, Visa will be modifying the existing Visa Chargeback Monitoring Program (VCMP) and Visa Fraud Monitoring Program (VFMP). Please refer to the table below for the new thresholds.

1.1.3 Visa 3-D Secure

Visa is rebranding the Verified by Visa (VbV) program name to Visa 3-D Secure.

1.1.4 Contactless acceptance – EMV support timeline

As of October 2019, magnetic strip data (MSD) contactless acceptance must be discontinued. Visa will begin monitoring contactless transactions to ensure support. If you are unable to meet the timeline, do not disable MSD contactless. Instead, please contact your acquirer to discuss a migration plan.

1.1.5 Interlink in the U.S. and Puerto Rico

In July 2019, the processing fees on the switch fee reversal, adjustment, late adjustment, chargeback and representment were updated.

1.1.6 Guam domestic interchange and fees

In July 2019, some existing products were changed and new categories were added for Guam domestic transactions. Additionally, changes were made to the domestic and interregional fees for ISA, license fee, merchant service fee and some new categories.

2. Mastercard

2.1.1 The Mastercard Processing Integrity Program will rebrand to the Transaction Processing Excellence (TPE) Program

This program will introduce two new authorization monitoring programs with the following criteria:

- Excessive Authorization Attempts: Excessive account testing of a single account number, from the same card acceptor, within a 24-hour period.

- Nominal Amount Authorization: An approved nominal amount authorization with a subsequent renewal for transactions with the equivalent of 1 USD, 1 EUR, or under one full until of currency. This is for CNP transactions.

- The fees are forthcoming.

2.1.2 Transaction Integrity Classification (TIC) Processing

Mastercard is delaying the implementation of TIC processing to a future release. Additional information is forthcoming.

2.1.3 Contactless acceptance – EMV support timelines

As of October 2019, new contactless card and card access devices must be enabled for EMV contactless and MSD contactless. On the newly deployed POS terminals that support contactless, they must only support EMV mode, and not MSD. The final deadline for only EMV contactless support is April 2023. At this point, all terminals supporting contactless must only support EMV contactless, and MSD contactless must no longer be utilized or supported.

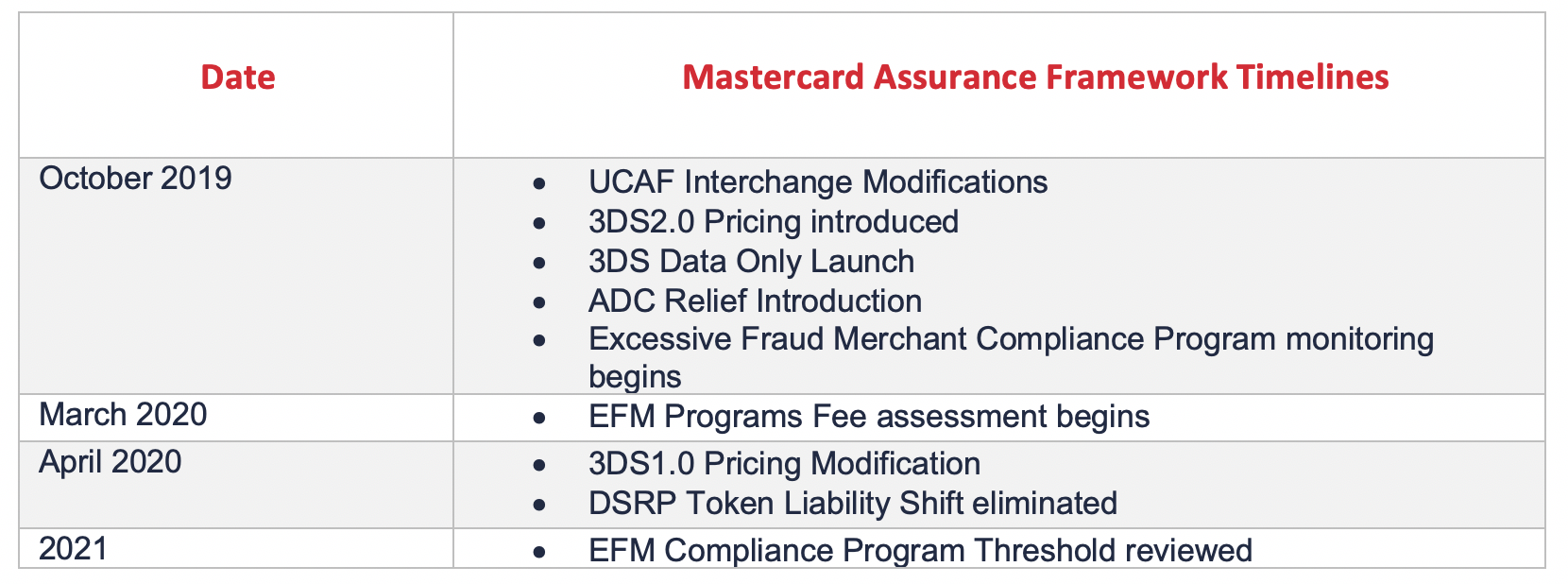

2.1.4 Assurance framework

This is a new program encompassing pricing and token technology. It will be introduced in a multiyear approach starting October 2019.

UCAF rates will be modified on transactions submitted with 3DS/SecureCode/Identify Check attempt and authentication data. These rates will align with other existing e-commerce rates.

2.1.5 Merchant location fee billing change

This billing term will be modified from annually to quarterly. The third quarter will be billed in October 2019 and the fourth quarter in January 2020.

2.1.6 Interregional refund transaction interchange modification

This is applicable to refund transactions when the merchant is located in the U.S. and the card is issued from another region. There will be two new rates: consumer and commercial.

2.1.7 Maestro international support fee

This took effect July 2019 and applies to cross-border Maestro PIN debit transactions. It applies to U.S. merchants accepting non–U.S. issued Maestro cards.

2.1.8 Mastercard cross-border commercial purchasing

Beginning October 2019, Mastercard will eliminate certain commercial purchasing interchange categories. These are detailed below.

- Interregional Commercial Purchasing Large Ticket – all regions

- Interregional Commercial Purchasing Data Rate II – all regions

- Intraregional Commercial Purchasing Large Ticket – Asia Pacific and Latin America

- Intraregional Commercial Purchasing Data Rate II – Asia Pacific and Latin America

3. EEA Interchange

3.1.1 Visa and Mastercard respond to European Commission’s review

Both Visa and Mastercard will modify interchange fees in response to the European Commission’s acceptance of proposals that were submitted in early 2019.

The rates will be changed on applicable transactions when an EEA merchant accepts cards from non-EEA cardholders. These will apply to consumer debit/prepaid and credit transactions. There will be rates created for card present and card not present transactions.

4. Canada

4.1.1 Mastercard

There are a few changes to the interchange items in Canada. Please find these detailed below.

- A new prepaid card product will be released to support electronic delivery of humanitarian aid. There will be specific interchange and fees associated with the category.

- A new commercial Freight Program will be released for Mastercard Enterprise Solutions (MES). This will be a virtual card applicable to commercial freight transactions. The program will be for certain merchant segments including airlines, shipping and government. These rates will apply when accepted at freight programs coded with the applicable MCC code. If this card is processed at another MCC, the existing rate will apply.

- Beginning November 2019, there will be a pre-authorization fee. It will be a basis point fee applied based on the authorization amount.