The Association for Financial Professionals releases the largest update to the code set to date

While the world was shutting down due to COVID-19, an AFP task force of 19 bankers, corporates, and software vendors embarked on a massive project, led by Redbridge, to update the AFP Service Codes©.

The last update to the code set was in 2013, and feedback from the community was that it was necessary to improve the code set to properly reflect today’s rapidly evolving treasury services market.

The AFP task force completed an 8-week project of reviewing all 2,000+ active service codes and made the largest update to the code set to date. “I have been involved in every code update since 2001, and this is by far the largest improvement,” said Bridget Meyer, Senior Director at Redbridge and task force leader. “We left no stone unturned.”

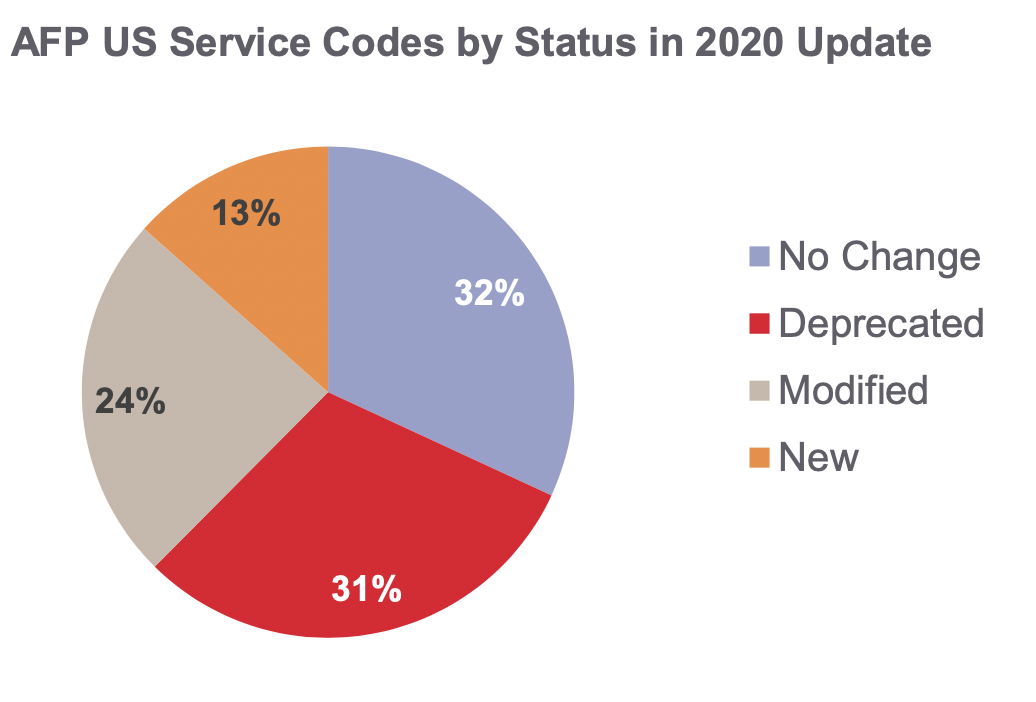

Only 32% of the codes remain unchanged. Figure 1 shows a breakdown of the update.

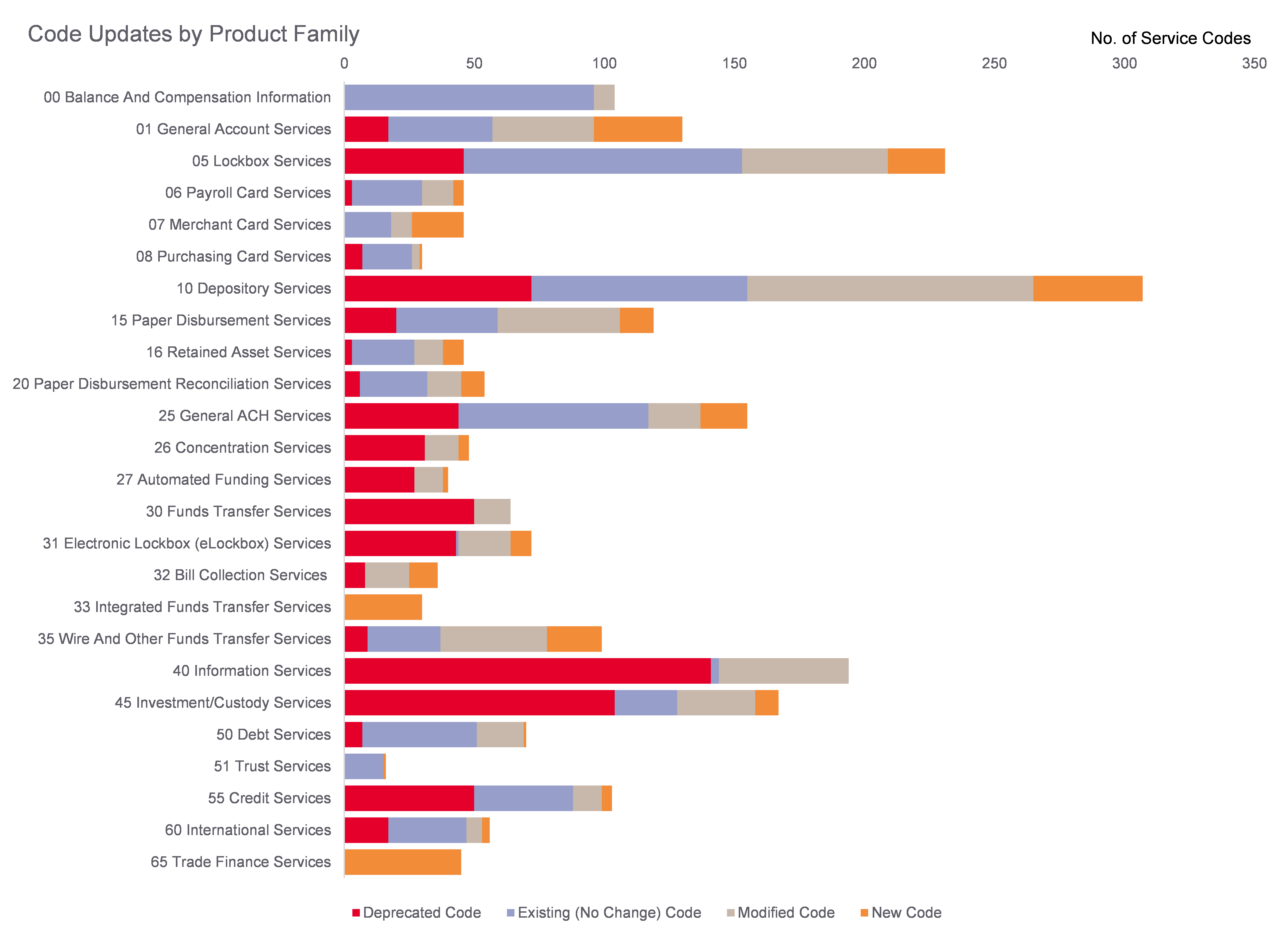

Summary of Code Changes by Product

New Product Families

The taskforce added two completely new product families during its review.

The first new product family is 33 Integrated Funds Transfer Services, which includes services related to integrated payables and receivables. The committee and the industry define integrated payables as “the ability for a corporation to send a single file to the bank containing more than one type of payment (such as check, ACH, wire or instant payment) for the bank to translate into the appropriate format and release.”

Similarly, integrated receivables combine remittance information from multiple payment types into a single file for posting. Companies can provide banks with an open accounts receivable file for automated matching by the bank for increased, straight-through processing.

Accounts receivable matching, or A/R Match, codes were added in the 05 Lockbox Services, 31 Electronic Lockbox (eLockbox) Services, and 33 Integrated Funds Transfer Services product families.

The second new product family is 65 Trade Finance Services. Previously, letters of credit and documentary collections were broken out between two separate product families: 60 International Services and 55 Credit Services. The committee’s position was that these services, whether domestic or international, are maintained by the same group at the bank and, therefore, deserve their own product family, similar to the AFP global code structure.

Modifications by Product Family

Account Services

Many banks have started differentiating between debit and credit posting charges based on electronic or paper transactions, so new codes were added to further clarify this.

Imaging services and charges have spiked and more and more banks are billing for access to a single portal for all images (e.g., checks paid, lockbox, etc.), rather than separating them by product. Therefore, we added a new “0120 Multiproduct Imaging” product group.

Similarly, on the transmission and channel services side, some banks have stopped separating file transmission services by product, so we added a new “0140 Multiproduct Transmission Services” product group. Throughout the code set, we added language to include data exchange via application programming interface (API) as a part of data transmission to accommodate for growth in this sector.

We also added new codes for artificial intelligence services, mobile authorizations, and account validation services to the 01 General Account Services product family.

Lockbox Services

Lockboxes are still the workhorse for most large corporations in America, and the services are still evolving based on task force feedback. New services for A/R Match, stop files, multi-demand deposit account (multi-DDA) lockbox deposit services, and even address changes were added to the 2020 code set.

The distinction between black and white versus color imaging was removed. Data capture and sorting services were simplified, and reporting evolved to the delivery method versus the different types of content within a report.

Depository Services

The largest product family, 10 Depository Services, had major modifications in the AFP 2020 code set to better reflect today’s cash vault and image deposit environment.

With the advent of image clearing, rather than physical clearing, by the Fed, check clearing charges were simplified to either “on-us” or “other bank” by most financial institutions.

The remote deposit codes were modified to distinguish image cash letter transmission services from desktop deposits with low-volume scanners.

The 1012 product group for “Contract Vault Services” was modified and repurposed to only apply to cash vaults that are “expanded” or “extended” from the primary bank network. While many banks (if not most) subcontract their cash vault services to a third party, usually, this is not transparent to a customer. Moreover, the assignment of a “contracted” vault service code was confusing. Additional codes for vault maintenance fees, armored carrier charges, depository tracking services, and smart safes were added or clarified in the new 10 Depository Services code set.

Paper Disbursements and Reconciliation

Corporations in the U.S. still love to write checks, but more and more are outsourcing this service. The 1518 product group for “Disbursement Outsourcing” was renamed to “Check Print Services” now that the 33 Integrated Funds Transfer Services product family exists. Check paid imaging, retention, and archiving were modified to be consistent with imaging services in other product families, and the task force removed outdated physical check return services that banks no longer offer.

Banks have created every combination of positive pay, payee verification, and reconciliation services, so more codes were added to accommodate. In line with its mission to rework all reporting services to be organized by delivery method (i.e., transmission, internet, electronic message, or manual), the task force took great care to clarify reconciliation reports.

“Banks adopting the new codes should pay attention to the additional information provided in the definitions of all modified and new codes,” explained Bridget. “The task force added more direction within the descriptions, even provided examples, to help with the proper assignment of codes.”

Card (Payroll, Purchasing, Merchant Card)

While most banks in the U.S. do not report card fees using an industry-standard format, outside of the U.S., cash management banks can be more involved in the processing and reporting of these fees. There is a movement globally to move merchant fee reporting under the ISO 20022 umbrella and leverage the camt.086 message type to encompass all fees charged by banks, not just cash management services. Therefore, the task force reviewed and improved even lesser-used product families to make them consistent with the global AFP code set and to have relevant codes for banks that choose to use them domestically.

Information Reporting

Information reporting used to be the most confusing and difficult product to map due to the detail required. Before finally mapping to the correct delivery method of the report, one had to know if the report was domestic or global, previous day or intraday, and summary or detail.

The task force removed the distinction between global or domestic and summary or detail in the 2020 version, greatly reducing the complexity and sheer number of codes in this section.

ACH Services

- Product family 26 ACH Concentration was renamed to Concentration Services in preparation for the fact that corporations may soon have a choice when concentrating funds and domestic pooling across banks using instant payments.

- Product family 27 was renamed from ACH Standing Order Services to Automated Funding Services, and ACH standing order charges were moved to the 25 General ACH Services product family. Previous task forces had combined standing orders and automated funding, but it was identified that this was incorrect.

- The distinction by ACH payment type (e.g., CCD, PPD, etc.) was removed from the codes, and the ACH reporting section was reworked to be by delivery method rather than content.

Instant Payments and Wires

After much discussion, the task force added a new product group for “Instant Payments” within the existing 35 Wire and Other Funds Transfer Services product family. The 35 product family now includes all electronic payments and receipts except those cleared by the ACH Network.

Real-time (or near real-time) payments (RTP) are exploding in the U.S., with the continued expansion of The Clearing House. The Euro Retail Payments Board (ERPB) – a strategic body tasked with fostering the integration, innovation and competitiveness of euro retail payments in the EU – defines instant payments as “electronic retail payment solutions that process payments in real time, 24 hours a day, 365 days a year, where funds are made available immediately for use by the recipient.” Examples of instant payments are RTP, Zelle®, and Venmo in the United States. The task force decided to adopt this term and call these emerging payment types “Instant Payments” in the AFP 2020 code set.

Electronic Bill Payment and Presentment (EBPP)

Product family 32 Internet Payment Initiation Portal was renamed to Bill Collection Services. This product family includes services that provide additional options for large corporations to give to their customers to pay their bills or invoices. This includes websites or apps to collect and process payments branded to look like the corporation’s, interactive voice response (IVR) systems, and over-the-counter merchant solutions. Bill pay aggregation services, such as electronic lockbox, are not included in this group as they are considered extensions of traditional lockbox services and are now coded in the newly revised product family 31 Electronic Lockbox (eLockbox) Services.

Electronic Lockbox

The 31 product family was renamed Electronic Lockbox (eLockbox) Services and includes bill pay aggregation (with or without presentment) services, otherwise known as electronic lockbox or EBIP. Remitters go to their online banking portals to initiate payments to the customer (biller). The electronic payments are then aggregated by the bank and settled in a single daily transaction. As online bill pay portals for consumers have advanced, the code set needed to be cleaned to remove antiquated software and presentment services to receive these consumer payments.

Electronic Data Interchange (EDI)

Most of the EDI product family was deprecated due to the addition of funds transfer file transmission services being added to each relative product family, the new 33 integrated payables and receivables service codes, and the new 0140 “Multiproduct Transmission Services” group added to the 01 General Account Services product family. Banks should only use the remaining EDI service codes (which have been renamed to Funds Transfer File Transmission services) when the fee is for generating or receiving files that result in the movement of funds, regardless of product (i.e., ACH, wire, checks, etc.).

In Summary

All product families were touched by this update to the AFP Service Code set. Task force members met with subject matter experts in retained assets, payment cards, trade, debt and credit, and custody services to ensure that whoever chooses to use these codes internally for data analytics, pricing exercises, or externally for an RFP or account analysis, the best options are available to reflect today’s treasury environment.

So, When Can I See the New Codes on My Statements?

That depends on your bank. Task force member banks mentioned adoption anywhere from this fall to spring 2022. During this adoption period, it is incredibly important to ask your banks which code set they are using and to ask them to adopt the new codes. Otherwise, you will have a large potential for apples mixed with oranges.

AFP Service Codes Accredited Providers will be updated during their next renewal cycle. This means BMO Harris, Capital One, Citibank, City National Bank, Hancock Whitney, People’s United, Signature Bank, and Wintrust Financial will be among the first to adopt the codes.

This Is Where HawkeyeBSB Is So Valuable

If you are a Redbridge HawkeyeBSB customer, we have you covered. Regardless of the bank you use, all HawkeyeBSB AFP codes will be updated by Redbridge as a user benefit.

About the AFP Service Codes

There are two different sets of AFP codes used by the financial industry: AFP Service Codes and AFP Global Service Codes.

AFP Service Codes are industry standard codes assigned by all major banks to their cash management services billed to large corporations on their account analysis statements. Proper assignment of the codes allows a corporate treasurer who uses multiple banks to perform analytics, cross-bank comparisons, and RFPs effectively. In this big data day and age where every corporate and bank alike are looking to implement business intelligence (BI) tools, classification of data is not only necessary – it is critical to the success of the analytics and insights expected in these projects.

The AFP Global Service Codes were created in 2011 and recently updated in 2018 thanks to efforts by the CGI-MP Swift Work Group 5, a global task force (also led by Redbridge) dedicated to a common global implementation of the international bank fee reporting (ISO 20022 BSB) standard. The global codes were designed specifically for the international community, based largely on the original AFP Service Codes created in the U.S. for use in the EDI 822 standard in 1986. In the U.S., over 800 mid- and large-sized corporations currently receive their bank analysis statements electronically using the ANSI X12 EDI 822 Transaction Set in which the U.S. AFP Service Code is a mandatory field.