The use of cash and coin is not only declining, it is becoming more expensive each year. Large corporations required to receive payment in cash constantly look to reduce the cost of this service and manage the associated risks. Read here for some of the latest trends in cash and coin collection.

The shift in the market is both from the armored carriers and the bank side where corporate servicing is increasingly more costly at the bank’s “retail” branches. This is because organizationally, within a typical large bank, the physical branches are run by the ‘retail’ side of the bank, catering to consumers and small businesses. Costs to service large corporations’ coin and currency must be tracked by these branches and allocated back to the corporate side of the bank. This is becoming more and more costly for banks to manage and therefore servicing cash and coin for corporate clients is either diminishing in availability or becoming exceptionally expensive.

Armored carriers are increasing their own service capabilities to address these needs and corporations have the challenge of determining the best mix of branch deposits and armored carriers to service their needs.

Increasing Regulations on Cash Handling

The ability to comply with regulations may determine whether a bank can accept any client’s depository business. Some businesses that accept large volumes of cash may be highly regulated and a company’s industry might predetermine a bank’s ability or desire to accept and process their deposits. Due to the possibility of money-laundering, counterfeit currency, terrorist and other illegal activity, banks servicing coin and currency clients must adhere to the due-diligence required to be absolutely certain that they properly can onboard and continually service those cash-heavy clients within all Anti-Money Laundering (AML) regulations. For example, clients in the gaming industry can expect to endure a very detailed process that entails questionnaires, background checks, or gathering information on internal securities and controls, prior to a bank agreeing to accept their depository business. Clients in the check-cashing business or those that sit in certain geographic areas are likely to face the same scrutiny. Some banks have decided to not do business with cash intensive customers due to the regulatory compliance and reputational risk involved. In an RFP that was conducted for a gaming client, one bank declined to bid on the cash depository business due to the fact that the company accepted cash from gaming activities.

Branch Deposits

Large commercial banks have long been shifting away from paper depository business. In two separate recent RFPs issued for clients requiring branch network services, the clients’ existing bank decided to increase pricing for several depository elements! That same bank also provided information on cash vault options as an alternative. Two other banks that were invited to the RFP declined to bid on the depository piece altogether. Increased costs, but more importantly, a desire to fully separate the retail banking business from the large corporate bank are driving this behavior. Recently it was noted two of the largest US banks have increased branch depository fees as much as 40 percent, forcing clients to either select another bank or consider an armored carrier service. Coupling high branch costs with technological advances allowing alternative ways for customers to make deposits such as remote deposit and mobile deposit, is also driving some banks to close down branches. Wells Fargo recently announced the closure of 450 bank branches by the end of 2018 however Wells will remain the leader in number of bank branch locations (see Figure A).

One question clients should raise to banks during initial discussions is whether they have any branches slated to close in the coming years. Figure B shows the change in the number of bank branches from 2012 to 2017[1]. Another consideration is the length of implementation given the potential for extensive internal bank approvals that might be required to use that bank’s branch network.

Vault Deposits

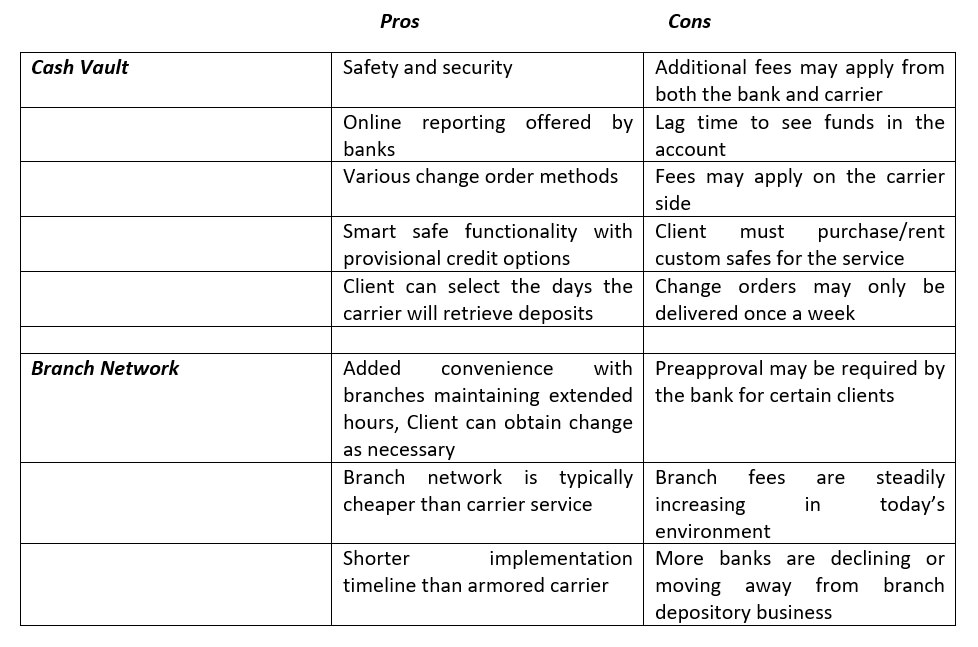

A significant shift in the past decade has been for banks to completely outsource the delivery and processing of the cash and coin to armored carriers and cash vaults. Several advantages come with utilizing an armored carrier and cash vault. Employee safety is one reason companies choose this option. While banks typically charge less for handling cash deposits made at their own bank vault location vs at a branch location, the added safety and convenience may be valued enough to use an armored carrier. Armored carriers can deposit either at the bank’s vault or at the armored carrier’s own vault. Costs should be weighed to determine the best alternative and geography and distance may be the driving consideration. Safety of staff is another consideration. Many Risk and Compliance departments prohibit employees from walking or driving deposits to a branch due to the potential danger involved when carrying large sums of cash. Armored carriers also deliver coin orders directly to the retail locations to replenish cash tills. Many banks who partner with armored carriers also may offer a cash vault module with an online portal that allows a company or retail location to track deposits, place change orders, order supplies, among other services. Additional benefits of using an armored carrier can be found in Table 1.

Currently, there are three major carriers that cover a wider, national footprint as well as several smaller, regional carriers to choose from. Each of the largest three may cover geographical areas differently so a detailed analysis is likely required for a large company’s solution. Quality of service in any particular area is also a variable that might best be addressed through obtaining references in the RFP process.

Smart Safes

Another popular service in today’s cash vault environment are smart safes. These can be provided by either the bank or by the armored carriers. Smart safes allow a store to deposit bills into an automated safe that electronically sends a notification to the bank to credit the customer’s account. The bank, in turn, provides provisional credit for the cash deposited prior to it being removed by the armored carrier and verified at a cash vault site.

The cost of smart safes has been a real barrier to their broad adoption but some banks are breaking down this barrier by starting to subsidize the cost of the hardware. Purchasing used equipment with a maintenance plan to help reduce the initial investment is an alternative to consider. Installing smart safes reduces the number of trips from the armored carrier which positively impacts the net cost. One Fortune 500 client of Redbridge recently advised it is piloting a smart safe “bundled solution” with its bank where bank serves as the company’s primary contact for all inquiries related to smart safes despite the armored carrier’s involvement. The client has been very satisfied with this solution and is considering transitioning additional stores to this type of setup. This bundled solution could have a positive impact on the acceptance of smart safes.

Conclusion

While branch services still make the most sense for small businesses and some mid-size corporations, the large corporate space has clearly transitioned to armored carrier vault services in the past 10 years. These armored carriers are partnering more with selected banks and we expect this trend to continue. Similar to the lockbox industry, corporations should not underestimate the role 3rd party providers will continue to play in cash and coin servicing in the near future.

Ultimately, companies need to balance cost, convenience, safety and risk when evaluating their options to supply and deposit cash and coin to their locations. Redbridge recommends considering a thorough analysis of the right combination of bank branches, armored carriers, and possibly smart safes, to achieve the best solution for their company’s long term coin and currency needs.

Table 1

[1] Source: www.usbanklocations.com