For many corporate treasury teams, Treasurers and CFOs, optimizing bank fees often doesn’t top their priority list. Yet, left unexamined, these fees can accumulate unnecessary expenses and create inefficiencies in cash management.

If your company encounters any of the following scenarios, it’s time to reassess your bank fees and services. A structured, objective assessment of your bank and services can uncover savings, streamline services, and align banking costs with your company’s needs – as well as improving your overall banking relationships due to improved transparency across your bank fees and services.

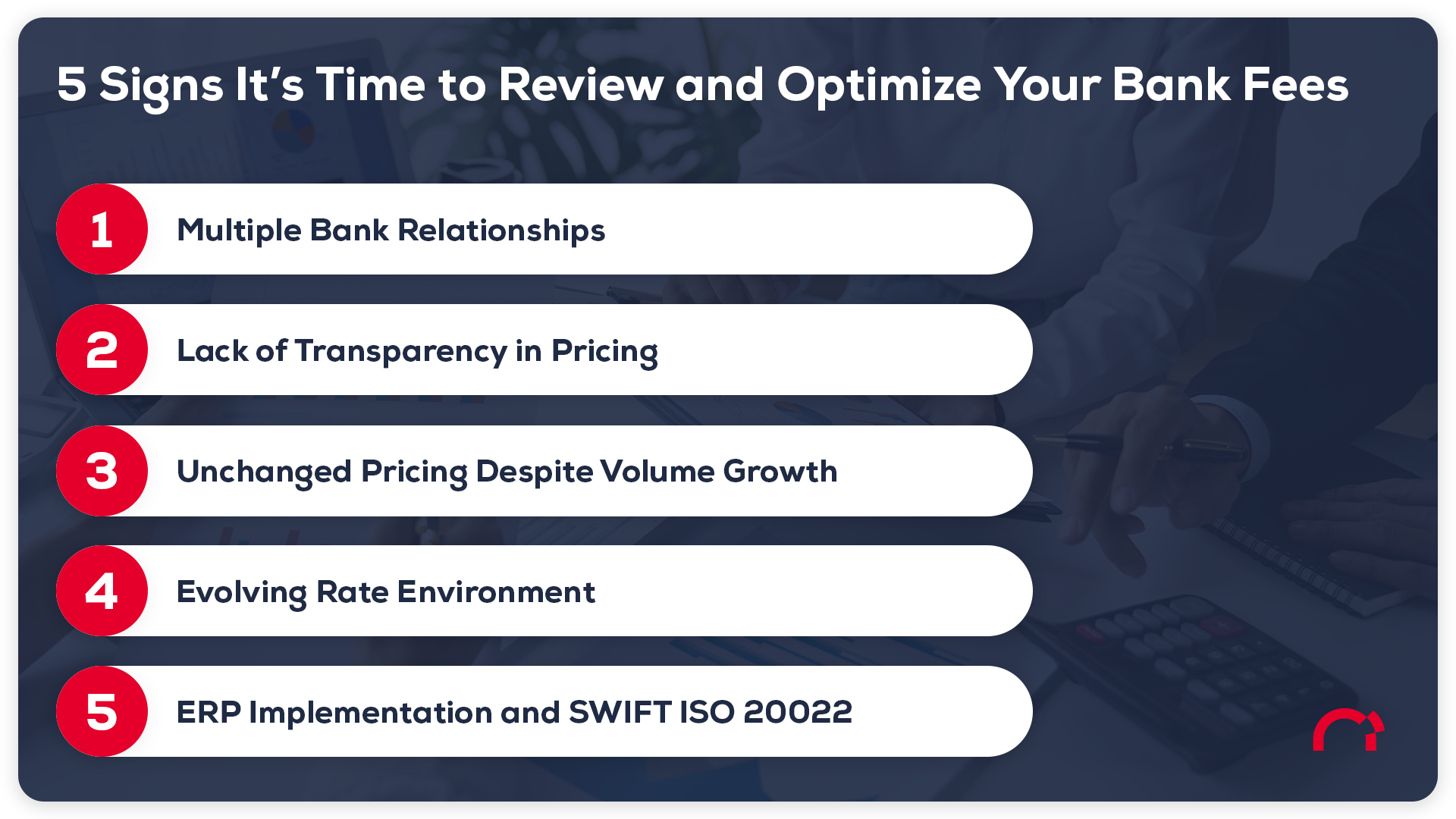

Here’s how to tell if it’s time to take action:

1. Multiple Bank Relationships

When companies grow through acquisitions or maintain legacy systems, they often retain multiple bank relationships each with multiple accounts—sometimes more than necessary. This can lead to duplicate services, redundant fees, missed volume discount opportunities and a lack of unified oversight on bank accounts. With hundreds of accounts spanning multiple banks and countries, it’s easy for treasury teams to lose visibility, and fees multiply unnoticed.

A treasury department’s trust in existing banking relationships can sometimes lead to replicating services and settings for new accounts without assessing actual needs. This practice may result in unnecessary and inefficient services, such as printed statements, CDs, and paper check return fees.

Optimizing bank relationships means reviewing the necessity of each account, understanding individual bank service line strengths and weaknesses and consolidating wherever possible. Cleaning up accounts and services can yield immediate cost savings and streamline cash management practices, especially when aiming for centralized oversight across the organization.

2. Lack of Transparency in Pricing

A common pain point for treasury departments is inconsistent or unclear pricing. It’s not unusual for companies to find disparate rates for identical services, even when using the same bank across different entities. Without a detailed pricing grid that maps out service costs across banking relationships in different countries, these discrepancies can become costly.

Creating a transparent and consistent pricing grid is essential for informed financial decision-making. Understanding exactly what you are paying for – as well as what fair market prices are – can help avoid unnecessary fees, clarify service value, and equip your team for stronger negotiations with banking partners.

3. Unchanged Pricing Despite Volume Growth

As transaction volumes increase, pricing should reflect this growth by offering unit rate reductions. Many organizations miss this opportunity, instead paying the same (or even higher) fees per transaction despite higher volumes. When bank service costs don’t account for volume discounts, companies may face fees that don’t align with the scale of their business activities.

Treasury teams should leverage their higher transaction volumes to negotiate better rates. Banks benefit from this increased volume, and it’s reasonable to expect corresponding reductions in fees. It is recommended to review bank fee pricing every 3 years and renegotiating terms based on volume to maximize savings as your company grows.

4. Evolving Rate Environment

Interest rate trends directly affect bank fees. In the past, higher interest rates may have allowed companies to offset significant portions of their bank fees with earnings credits. However, as rates decrease, these credits may fall short of covering fees, resulting in higher out-of-pocket expenses.

Reviewing bank fees in light of changing rates is essential. Companies previously unaffected by fee changes due to offsetting credits may find themselves newly exposed to these costs. Adapting to the current rate environment allows treasury teams to maintain cost-effective banking arrangements that align with both their cash flow and interest rate conditions.

5. ERP Implementation and SWIFT ISO 20022 Compliance

Updating ERP systems to meet new SWIFT ISO 20022 standards or consolidating disparate ERP systems across entities can bring significant benefits to treasury departments—but also added complexity. When implementing a new ERP, companies have a unique opportunity to reassess their bank fees and eliminate redundant or unnecessary services.

The ERP setup process is typically long and involved. Taking the time to identify and correct inefficiencies and streamline bank accounts before or during ERP implementation can save both time and resources. Treasury teams that align bank fee structures with ERP capabilities can avoid duplicate setup costs and achieve a more efficient, transparent system from the start.

How Redbridge Can Help

If any of these scenarios resonate, it’s a good indication that your company could benefit from a comprehensive bank fee and service review. Redbridge specializes in identifying optimization opportunities, improving transparency, and negotiating favorable terms that align with your company’s size, growth, and specific treasury needs. This requires only minimal effort on your part thanks to our unique delivery platform with dedicated teams that carry out the heavy lifting in the background so you can focus on your key priority areas.

Contact Redbridge today to see how we can help you optimize costs, improve efficiencies, and position your company for sustainable growth.