An operational analysis of the European market for bank financing for large corporations reveals major pricing disparities among lenders, with indicative spreads that can vary by up to 100% within the same facility.

Due to a lack of public information on existing deals, bank financing is not subjected to the competitive forces necessary for a truly efficient market. The syndicated loan market reflects the challenges borrowers face in a non-transparent environment since such conditions seriously impede a corporation’s ability to accurately benchmark the relative value of a transaction.

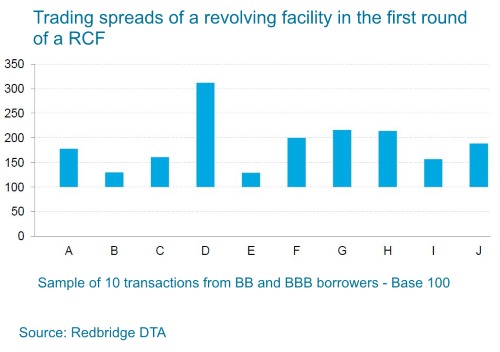

To create an optimal funding strategy, corporations must understand the nuances within the bank debt market, including knowledge of the most competitive terms and conditions for similar corporations. To this end, Redbridge DTA analyzed 10 financial transactions of BB and BBB rated companies over the last 12 months. Each company initiated an RFP to establish a revolving credit facility (RCF).

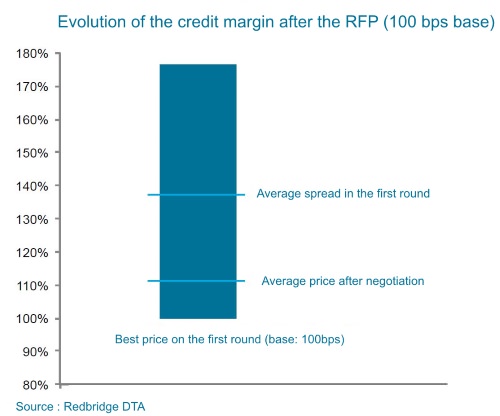

The results of the exercise revealed large pricing disparities among banks. Despite conditions generally favorable to borrowers and in an environment with tight spreads, the first round of quotes showed significantly divergent levels among the banks.

Credit Risk

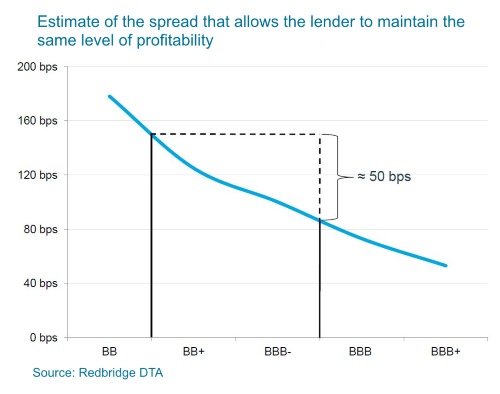

Why such differences? According to the sample, banks do not appear to share similar assessments of borrowers’ credit risks. The differing views can create rating disparities of up to two notches.

Based on a proprietary model for allocating bank capital, the different assessments of a borrower’s risk can create a 50bps gap between the two notch differential of a BB+ and a BBB rated corporation. This explains half of the observed spreads between the tightest and widest levels of initial pricing.

The perception of credit risk varies among lenders and is difficult for borrowers to understand, yet it is at the foundation of bank negotiations. It is therefore essential that a corporation obtains its internal rating from each prospective lender. And, if necessary, the corporation should conduct bilateral discussions with each credit team to ensure the perceived risks of each of the lenders in the pool are aligned.

Negotiation levers

Renegotiating credit terms requires a clear strategy. There are numerous variables that factor into negotiations, such as side-business allocation, quality of relationship, and competitive dynamics. All factors, including terms within the credit documentation, must be part of the price negotiation. Borrowers should also strive to engage in bilateral dialogue with lenders to ensure the maximum level of transparency.

In addition, the composition of the banking pool must be aligned with the group’s strategy for growth. The borrower should also identify past and future side business with each of the lenders in order to analyze the overall profitability of each bank. Doing so enables the borrower to successfully address pricing issues with empirically supported data.