While the last few years have created significant changes in the treasury landscape with a rapid push towards digitalization (e.g. the resurgence of the QR code), the pace of change within the depository environment is better described as a slow and steady march.

Treasury environments are slowly evolving

Depending on the types of deposits your company is making, there may be some space for change, but most of our depository clients are not seeing the same kind of digital revolution we see elsewhere in corporate treasury.

Treasurers around the globe are trying to push for electronic payments because they are faster, cheaper, and easier than cash and card payments. With this new shift, where does that leave retailers who deal with cash and coin deposits, or whose clientele still wants to write checks? While there are some alternatives to branch deposits out there, there is nothing disruptive in the market right now that would allow treasurers to radically change how they accept deposits. When we cannot count on digital disruption to reduce costs, optimization and a clear understanding of the options on the market today are the best way for treasurers to improve their bottom line.

One of the most consistent things Redbridge sees with our international retail clients is a strong reliance on armored couriers and, in nearly equal measure, dissatisfaction with their couriers. While talking with one retail client recently, their Assistant Treasurer told us how a lack of transparency in armored courier fees and a complicated workflow for depositing into their smart safe pushed them to explore other depository providers. Couriers would show up late, stay longer than anticipated, or show up on the wrong day and our client would get hit with the fees on their account analysis statement with no explanation of why the fees varied month to month.

Shifting depository strategies

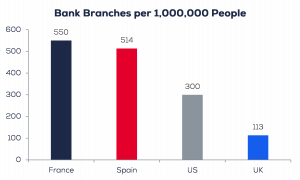

So where does that leave the retailer with cash and coin to deposit who is in a position to move away from their current armored courier? With banks in the US closing 5% of branches between 2017 and 2020 and the UK shuttering over 4,000 bank and building society branches in the last 6 years, companies around the world are coming to the same conclusion: going back to branch depository will not work.

Thankfully, though, there are some interesting options in the market that we see clients using with great success. For example, the retailer mentioned earlier opted to start making deposits with DTS Connex, a US provider with online cash management tools designed to work with any bank, courier, treasury, or ERP system. They are still storing cash onsite in a safe and waiting for a pickup, but a clear, easy-to-use bank agnostic deposit prep website and straightforward transparent pricing made the switch an easy decision. Another major retail client used DTS’s deposit-by-mail service for stores without a bank branch nearby.

For the retailer that receives a large amount of coins and doesn’t use a cash recycler, some stores have gotten even more creative. After all, it is hard to check out at the grocery store without seeing a box collecting coins for charity. Reduced coin deposits, a tax write-off at the end of the year, and social good? A win-win-win for those who use this strategy.

Globally, armored couriers can sometimes be the best option, especially in smaller or more remote countries. For those clients it may be best to reduce the number of pickups and work to negotiate a more transparent fee model with your courier and try to receive invoices you can review (and possibly challenge) instead of having the charges lumped into your bank fees.

Embracing in digitization

Your depository business is not only cash and coin, and luckily, there are a few more options out there for non-cash, non-electronic payments. For our US clients who rely on lockboxes but who would like to shift to a digital alternative, eLockboxes can use AI and machine learning to reduce the number of exceptions and drive down costs. In the US and EMEA we are seeing a proliferation of apps that enable agents in the field to automatically scan checks or take electronic payments, where they previously would have had to take cash or check. With these apps, as long as cellular data is available, payments can be deposited before the agent leaves the premises. Additionally, as your check scanner ages and needs to be replaced, a smart phone and an app may be a more cost-effective solution. These alternatives have the additional benefit of being a bit greener than traditional methods, allowing treasurers to enhance the services they are using while being able to contribute to a greener, less paper-dependent future.

The biggest trend we are seeing with our clients in the depository space, and the biggest trend we have seen in general, is a shift towards bank-agnostic providers to take over the business that banks are increasingly trying to move away from. While this does shift responsibility back onto clients to source providers and do some of the preparation and reconciliation they used to rely on the banks for, what they get is a more agile environment where changing banks doesn’t mean changing processes or system integrations. What once could have ballooned into a months-long project can be done with a few keystrokes on the back end of a third party system.

Innovation in LATAM

When we really try to look ahead to see what could be in store for our depository clients, we are looking at LATAM. While much of the world has spent the last two years figuring out the most efficient way to take contactless payment, LATAM had already leapt ahead and found a way to accept cash payments online. Customers can make their purchase via OXXO in Mexico, Boleto in Brazil, or Baloto in Colombia and then go to a centralized location to scan the bar code and pay for it with cash. Retailers and utility companies especially, we are curious – would you embrace this kind of change?

Constance Veron, Frederic Vincendon, & Sarah Gundle

A special report on the cash management & payment trends that will transform your treasury department in 2022

The growth and vitality of the payments industry has fascinated all observers during the past two years of the pandemic. Now with recent geopolitical developments arising from the Russia-Ukraine conflict, it is being tested again.

Our new publication analyzes the most prevalent trends and innovations in the treasury world today.

Included in this publication:

- The Global Resurgence of QR Codes

- Choosing the Right Payment Terminal in an Ever-Changing Environment

- The Rise of Buy Now, Pay Later

- PCI Compliance in an E-Commerce World

- Where Do Banks Stand in the Race for Digital?

- Virtual Accounts, Which Companies Should Implement Them?

- The Future & Alternatives to SWIFT GPI

- Global Digitization in the Depository Space

- “Switching Banks Was the Right Decision”: An Interview with Olivier Bouillaud from Albéa

Download the full publication