Corporates who continuously utilize their cash balances carry an incisive tool for optimizing cash management costs & revenue. Creating a plan for managing those balances and the yield that is inherently created is a necessity in a market that is unlike ones in recent history. For treasury professionals, this means optimizing costs & interest earnings and strategically positioning this channel as a significant point of influence within banking relationships.

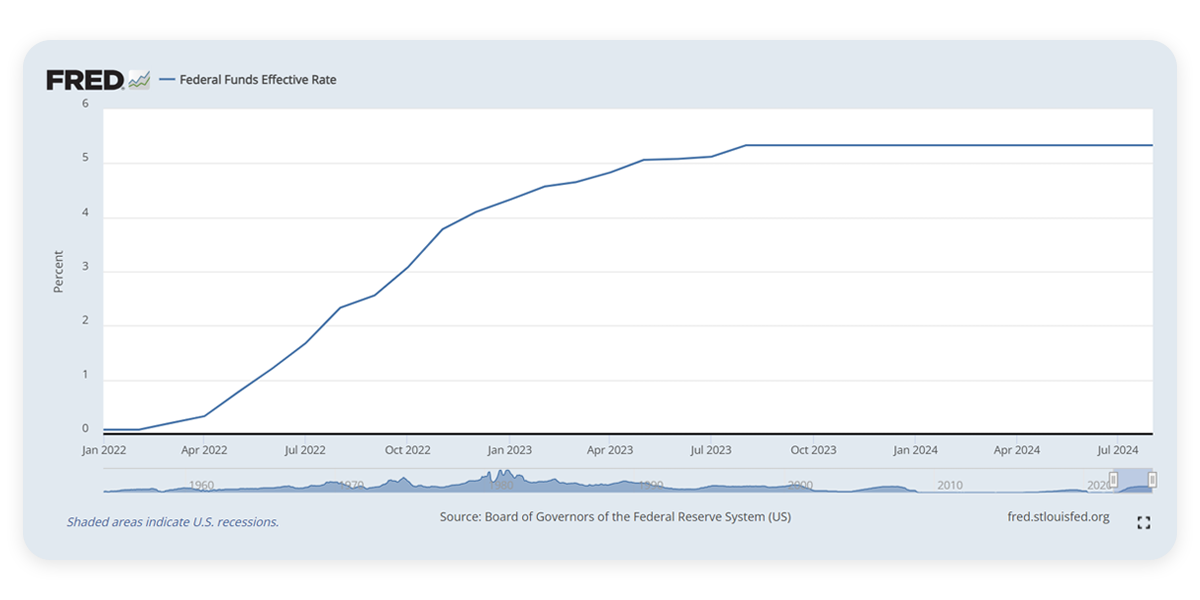

From January 2022 to August 2023, interest rates rose at an unprecedented pace, stabilizing only in the past year.

This rapid escalation required corporates to reassess their yield strategies to take advantage of the prospective beneficial circumstances. Initially, banks were slow to react to these hikes, often requiring their clients to initiate discussions to secure better rates. Whether implementing rate structures that indexed to the increases, or manually discussing new rates at every inflection, it was essential to capture the opportunity monthly. At Redbridge Debt & Treasury Advisory, we’ve assisted numerous businesses in implementing strategies to secure the best industry rates and yield structure during this critical period, understanding that these favorable conditions were temporary. For insights into how these strategies have been applied, consider reading about maximizing interest on cash deposits in our previous article.

Anticipating Changes: The Future of Bank Responses and Rate Declines

As 2024 ends and with it the long stable period of a maximized Fed target interest rate, the big question is: How will banks respond when interest rates begin to descend?

Unlike the gradual increase in Earnings Credit Rates (ECR) observed when rates were climbing, we anticipate that any decreases will be swiftly passed on to corporates. Unfortunately, banks may not inform clients of these rate changes unless asked. To mitigate the impact of these changes, it’s crucial for businesses to:

- Ensure clear communication with banks to establish proportional responses to changes in ECR and interest rates, ideally documented in writing.

- Negotiate terms that reflect a fair percentage of the rate decrease if applicable. ECR and/or interest rates should only be affected within fair judgement. If a client remains with a low Earnings Credit Rate compared to the FFR, it should not be expected that an initial decease of a quarter or half point will effect the ECR.

- Agree on timing for these changes to aid in financial planning, potentially negotiating a grace period to adjust to new rates.

- If a bank requires a predetermined target balance (PEG Balance), make sure that these are reviewed monthly as rates fluctuate. A decrease in ECR will require a higher PEG balance.

Exploring Alternatives and Strategic Adjustments

As the benefit of Earnings Credit Rate (ECR) diminishes with falling interest rates, corporations will need to adjust their strategy by reevaluating their current banking relationships and fee structures and service offerings. The attention shift will require banks to provide more attractive terms or additional or alternative services to help maintain profitability for their corporate clients. Furthermore, as diminishing ECR focuses more attention on treasury EBITDA, other financial aspects such as cash management services and associated fees will need reevaluation. Because of these changes, it becomes more important than ever to:

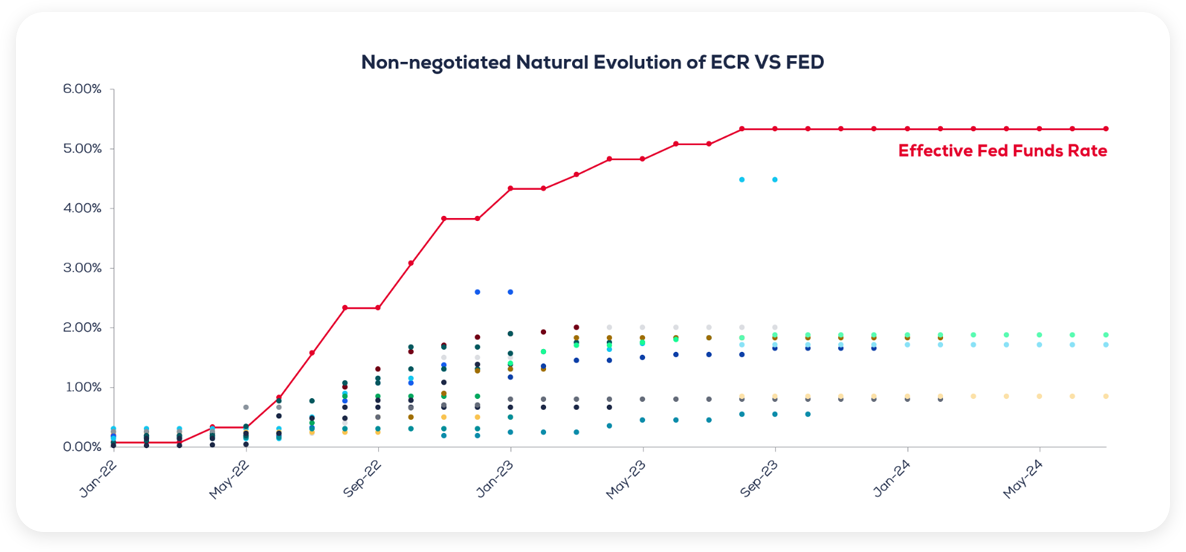

Maintain ECR in the spotlight, ensuring it remains a competitive factor across industries, pressuring banks to uphold strong rates. Rates are always negotiable. Even when FED targets are decreasing, it’s not too late to strengthen this corner of the Cash Management landscape. There are many situations where rates have not been negotiated and remain low. It is the responsibility of the organization and not the bank to keep this conversation in the forefront. The chart below shows Redbridge’s observation of rates left unnegotiated:

Review and negotiate fees for services like cash management, as these could become much more impactful in a lower interest environment, potentially impacting the EBITDA.

Moving Forward

As the interest rates evolve, so too should corporate strategies for managing yield and treasury operations. By anticipating rate changes, communicating effectively with financial institutions, and exploring alternative financial solutions, businesses can safeguard their financial health and continue to thrive.

For those looking to understand more about yield optimization and how it can be tailored to your corporate needs, reach out to our team at Redbridge Debt & Treasury Advisory. Let us help you navigate the complexities of cash management and ensure your strategies are aligned with the best industry practices.