4 faster payment methods for businesses and how each one can benefit your brand

Over the last few years, the number of corporates and banks seeking faster payment methods in the U.S. has spiked. COVID-19 has pushed many corporates further in this direction, and it has highlighted the need for quick, contactless payment methods. With branch closures and employees working from home, companies are looking for faster, safer, and more convenient ways to make payments. As a result, the popularity of same-day ACH, real-time payments (RTP), mobile payments, Zelle transactions, and other types of electronic payments have grown rapidly.

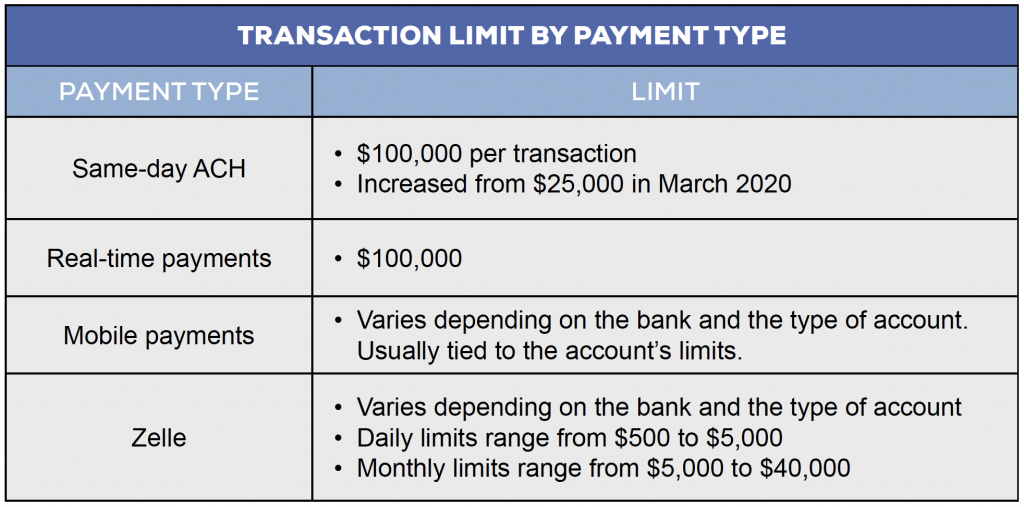

Same-day ACH

Corporates familiar with ACH payments know that they are electronic bank-to-bank funds transfers processed through the Automated Clearing House network. These payments have different settlement times, depending on the premium the corporate is willing to pay. Because it has the fastest settlement times, same-day ACH is the most expensive payment type. However, despite its higher price, same-day ACH has clear benefits that could entice a company to use them more frequently.

Its primary benefit is the speed at which the payment is settled. As the name says, the settlement occurs the same day. This is great for corporates that are under a time constraint when it comes to making payments. On the receivables side, same-day ACH could be a great alternative for card acceptance because businesses would not have to pay other fees like interchange or assessment fees.

Beyond the higher price tag, the same-day settlement can also be a disadvantage. For example, it can put pressure on a payroll team to have all the files sent and settled the same day. Any issues with the file or its contents could cause a delay in the payment.

Real-time payments

The RTP® Network was launched in November 2017. At first, financial institutions and corporates were slow to adopt this new technology because it required significant updates to internal systems and processes to enable the payments. However, as organizations started to understand the many benefits to implementing this new payment type, both the number of financial institutions and the number of transactions sent over the network increased substantially.

-

Benefits of sending and receiving payments through the RTP Network:

- RTPs can be made and received from existing accounts, so there is no need to open new accounts.

- Corporates can send and receive money 24/7, with immediate availability of funds received.

- If there is an outstanding invoice to your company, you can send a “request for payment” via the network.

- Being able to send and receive money instantaneously keeps corporates more in control of their cash flow and working capital needs.

- Once the payment is sent over the network, the payer cannot recall or cancel the payment. This provides the payee settlement finality.

- The network only “pushes” money, which mitigates fraud from someone being able to pull money from an account.

Real-time payments also assist with straight-through processing and automated reconciliation. Reconciliation can be a large pain point for many corporates. Each payment sent through the network is accompanied by enriched data, which makes it easy to match a payment to a specific invoice and allows corporates to dedicate less time to receivables reconciliation.

Mobile payments

Many global and domestic banks have mobile banking solutions. This gives companies the ability to authorize payments from their mobile phones. Corporates have slowly been shifting to mobile banking over the past few years, and over the last year, banks have seen an increase in the use of this solution due to the pandemic. Mobile banking allows employees to send payments from any location, and with the majority of employees working from home, this is a new convenience.

Mobile banking solutions are very secure with passcodes, touch ID capabilities, and tokenization. Tokenization safeguards the payee’s bank details so when a transaction is sent the actual account number is not shared. Not only do the mobile banking solutions let corporates make payments on the go, but they also can provide visibility of real-time balances across accounts and cash positioning. As banks continue to see interest in this solution, the innovation and capabilities will expand.

Zelle

Zelle is one of the newer payment methods being widely used by small businesses and consumers. Zelle payments can be made directly between two bank accounts with the use of an email or mobile phone number. Consumers have been the primary users of Zelle payments, but businesses are slowly starting to adopt it. So far, the transaction path for business-related transactions have mostly been business to consumer; however, it is only a matter of time before there is more consumer-to-business traffic.

One of the advantages of this payment option is the fact that account numbers are not exchanged between the parties. Transactions are quick and easy, and they can be sent and received either online or through a mobile banking application. Zelle transactions are best used when the sender has to make a quick, low-dollar amount transaction.

Fraud implications should be considered with Zelle payments. The fact that only an email address or mobile phone number is used is both its biggest advantage and disadvantage. If, for example, the sender accidentally misspells the receiver’s email or types the wrong phone number, they could potentially lose their money. Currently, there is no way to “undo” a payment. Once the payment is submitted, the sender cannot cancel it, unless the receiver has not yet been registered with Zelle. Another thing to consider is that this might be more difficult for larger companies to use because linking an account to an employee’s mobile phone number or email could be risky. Although these concerns have yet to be completely resolved, we do expect banks will find a way to address them soon.

RELATED RESOURCE

2020: The Year In Review

An Insights From the Field exclusive report on the treasury trends and innovations that swept 2020

This new publication analyzes the trends and innovations in the treasury world that were already in motion before this crisis began and that either accelerated or gained tremendous publicity during the pandemic.

Included in this report:

- Deposit Strategies in a Changing Banking Landscape

- The Pros and Cons of Faster Electronic Payments

- COVID-19 Forced My Digital Transformation. Now What?

- Where We’ve Been and Where We’re Going: An Overview of 2020-2021 Card Brand Changes

- Transitions in the Global Payments Market