While credit rating agencies have not yet changed their central scenarios for credit default rates, they appear to be growing more nervous in the face of changes in the economic cycle and the resurgence of volatility against a backdrop of greater geopolitical uncertainty.

Sectors that are particularly sensitive to “macro” changes (e.g., consumer goods and services, foodservice distributors), as well as the oil sector, have already suffered from this.

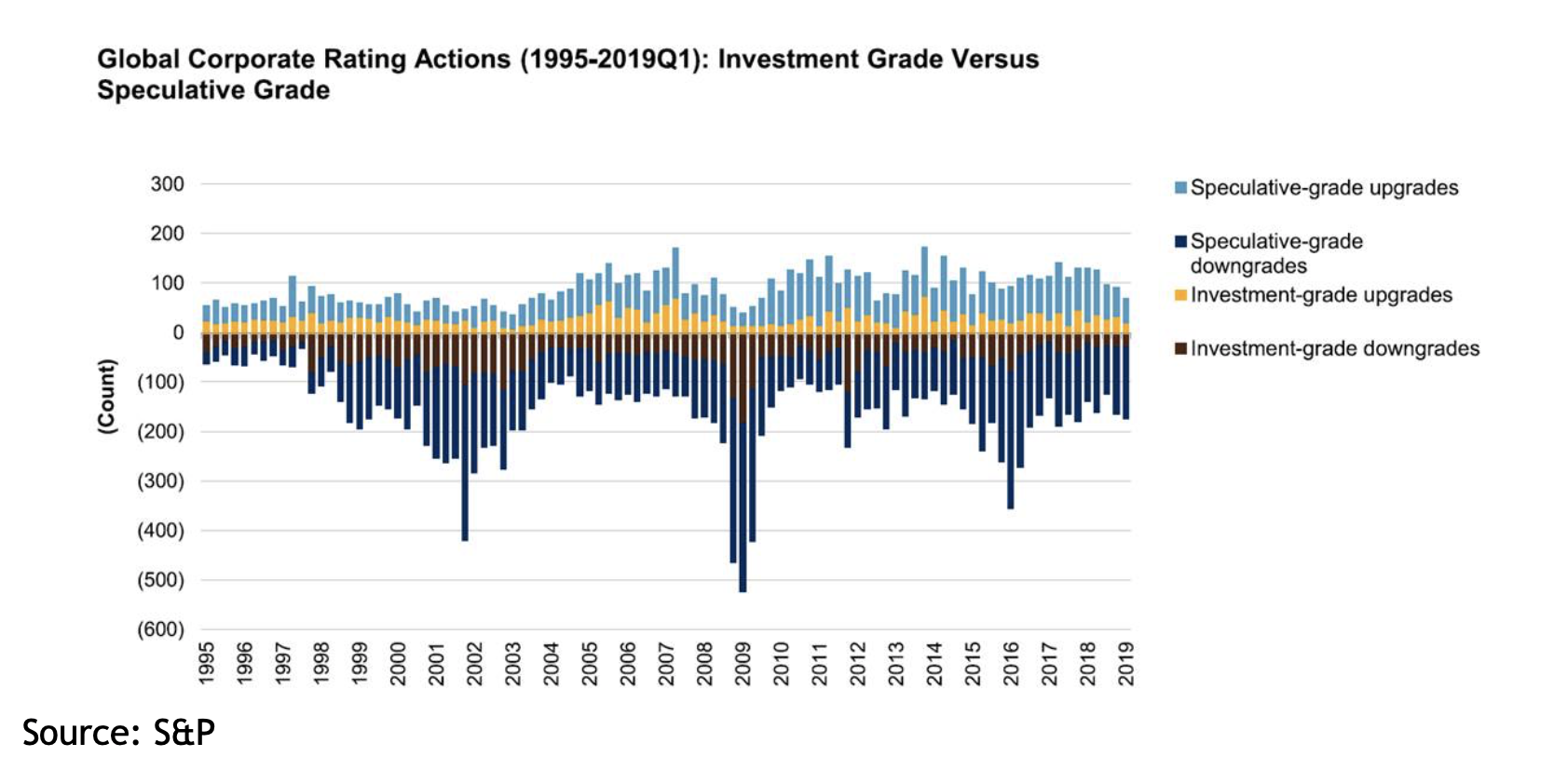

The ratio of rating downgrades to upgrades is at its highest in three years. For example, Standard & Poor’s (S&P) rating downgrade ratio reached 72% at the end of the first quarter in 2019, meaning that downgrades represented 72% of the agency’s total rating actions.

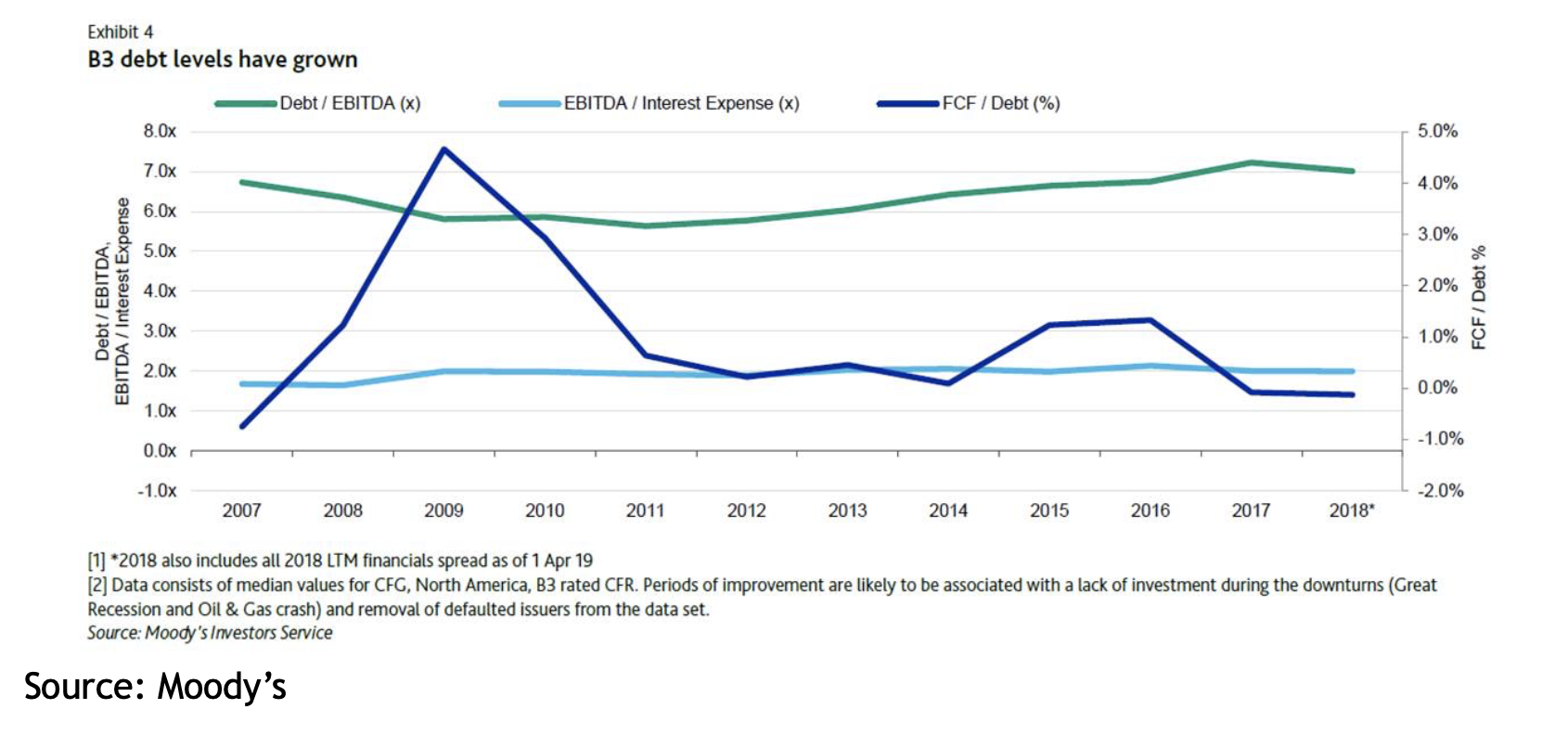

Unsurprisingly, the credits considered the most fragile are the most affected. The most heavily indebted issuers have been under increased scrutiny for several months. Lower B-rated issuers are facing increasing pressure on operational performance, especially on free cash flows.

The graph below, based on U.S. issuers with a B3 rating, illustrates this trend, which is mainly affected by the increasing weight of leveraged buyouts (LBOs) in this rating category.

In this context, Moody’s appears more cautious than S&P. For several months, Moody’s has taken a more negative approach than S&P in the heavily indebted issuer segment. The agency tends to organize committees as soon as it notices a deviation from the initial scenario.

Similarly, if free cash flows appear low, Moody’s is not inclined to include in its analysis new management initiatives (i.e., reorganization, disposals) whose benefits will only be felt in the medium term. S&P seems to be giving management teams the benefit of the doubt and granting them more time.

Redbridge believes that split ratings between agencies could increase. For example, based on a global, non-representative sample of 900 issuers in the BB-/B- category, Moody’s rates one-third of issuers more severely than S&P and gives the same rating as its counterpart to 55% of issuers.

B-rated issuers must manage their ratings with the greatest care. This involves:

- Understanding how rating agencies perceive their industry.

- Proactively identifying potential challenges (e.g., ratio adjustments, generation of free cash flows after restructuring costs).

- Building a relationship based on trust with rating agencies.

- Considering a third rating.

If you have any questions, please feel free to contact us at 346 207-0250.