Visa announces interim rate changes, effective July 2020

The latest: Visa has changed the implementation date for its rate changes for a third time. The changes – originally slated for April 2020 – were initially postponed until July 2020, then further delayed until April 2021. Some of its changes will now take effect in July 2020. Furthermore, Visa has announced that it will be implementing an “interim” fee modification to its new non-qualified rate, effective July 17, 2020. This interim fee modification will remain in place until the previously published rates take effect in April 2021.

[MORE: The Definitive Guide to the 2020-2021 Card Brand Changes]

What can merchants expect in 2020?

In short, we will be faced with the most sweeping and transformative changes in more than a decade. While these changes have been touted by the brands to alleviate the cost of acceptance in certain sectors, most organizations can expect to see increases in cost along with a myriad of modifications.

The sole intent appears to be to further obfuscate what is already a complex web of interchange rates, network fees and qualification criteria. The increased cost and opaque nature of these changes could not come at a worse time, as most organizations are already struggling just to keep afloat in a tide of COVID-19 related disruption and devastation.

As merchants struggle with simply maintaining their business, they will also need to begin thinking about the card brand changes and the impact these changes will have on their payment acceptance environments.

This year, all of the brands will introduce changes, but the most significant impact appears to be delivered by Visa. These changes are not limited to the rates themselves but also the structure as a whole.

Here are some of the more the significant changes we expect to see from Visa, Mastercard and Discover.

Visa

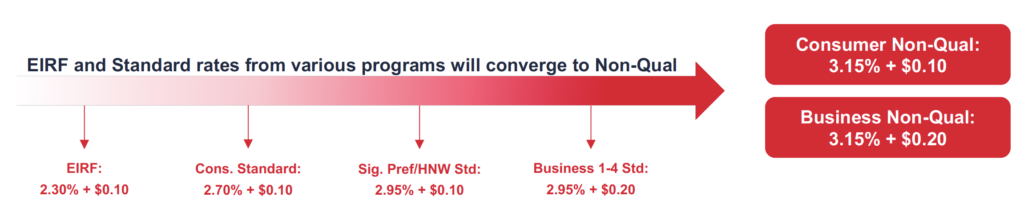

- Elimination of Electronic Interchange Reimbursement Fee (EIRF) rates

- Elimination of several Standard rate categories

- Introduction of non-qualified categories to replace EIRF and Standard rate categories; new rates are as much as 85 basis points (bps) higher than historical rates

- Elimination of the interchange benefits associated with many of its B2B merchant category code (MCC) designations

- Visa is doing away with its legacy custom payment service (CPS) categories and replacing them with Product 1 and Product 2 designations

- Modification and expansion of Visa’s supermarket interchange tiers

Mastercard

- Introduction of a Transaction Integrity Classification (TIC) which will become an interchange qualification requirement

- Introduction of a new day care consumer credit interchange category

- Introduction of a cap for real estate Merit I interchange

- Consumer credit purchase refund rate modifications

Discover, Mastercard and Visa

- Discover, Mastercard, and Visa will require an authorization approval code for processing purchase return (refund) transactions

- Discover, Mastercard and Visa are all updating their stored credential transaction requirements

- Discover is also introducing small ticket pricing for transactions less than $5

What should merchants do to prepare and mitigate avoidable cost increases?

To stave off cost increases, organizations will have to be vigilant in understanding the new complexities of the April 2020 interchange and card brand fee structures.

A successful outcome will require, at a minimum, that the following key components be addressed thoroughly:

- Data: Accessibility is key. Data must be normalized across channels and providers in order to draw meaningful and timely conclusions about the current acceptance environment and associated fees.

- Infrastructure: It’s crucial that the organization has the necessary processes and systems in place, whether it be homegrown applications or third-party solutions, to effectively review and track their payments data.

- Establishing key performance indicators (KPIs) and managing those KPIs is critical

- Understanding where the organization is in relation to its current interchange qualification efficiency ratios

- Establishing target ratios

- Ensuring there is a system and process reconcile fees to ensure accuracy

- Execution: Organizations must have a well-defined plan including the right resources, tools and technology to transition from its current state to its desired future state.

- Technology must be able to support the current business needs, while satisfying new card brand requirements

- Vendors must be assessed to ensure they are able to provide the necessary level of technology and support

- Account hierarchy and architecture must be closely reviewed to ensure it is yielding the most optimal outcome

- Fraud and risk exposure and acceptable tolerance thresholds must be constantly evaluated

Conclusion

In short, what the card brands are doing is simple. They are seeking to take what is already a complex and convoluted web of fees and further obscure the structure to make it more difficult for organizations to proactively manage their costs.

It is up to the organization to fight back by taking control, closely managing its payments strategy and continuing to evolve said strategy to stay current with best practices.

An effective strategy is one that is robust, holistic and multi-faceted. This includes:

- Evaluating and aligning payment methods across payment channels

- Reviewing merchant account structures and leveraging merchant category classifications

- Staying ahead of the data and timeliness requirements

- Ensuring that the organization adheres to best practices in its payment collection and return processes

Effectively managed, an organization can expect to contain its costs and prevent superfluous increases. The right tools, processes, systems and knowledge base is key in winning this fight.

For more information or questions on how to take action, please contact your Redbridge advisor.