April 2026 Update: Visa’s Commercial Enhanced Data Program (CEDP) – What Merchants Are Really Facing

Chelsey Kukuk

Director, Payments

The new CEDP pricing structure is now live, and the impact should be visible on April statements. For many merchants, particularly those with high volumes of Visa Small Business and Level II card transactions, it’s not a welcome sight.

How We Got Here

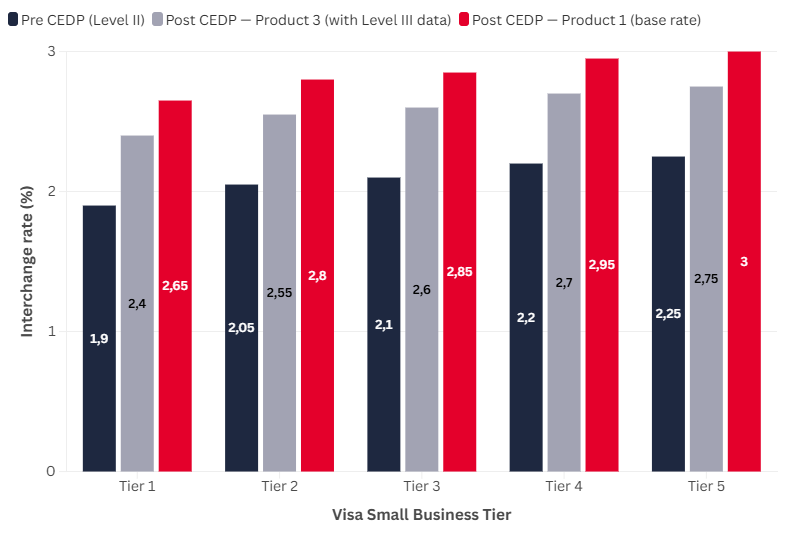

April 2025 – Visa first announced CEDP, the premise was straightforward and promising: merchants processing Visa Small Business card transactions (Tiers 1–5) with verified Level III data would qualify for a new Product 3 interchange rate that offered genuine cost savings over existing Level II rates. That promise didn’t hold.

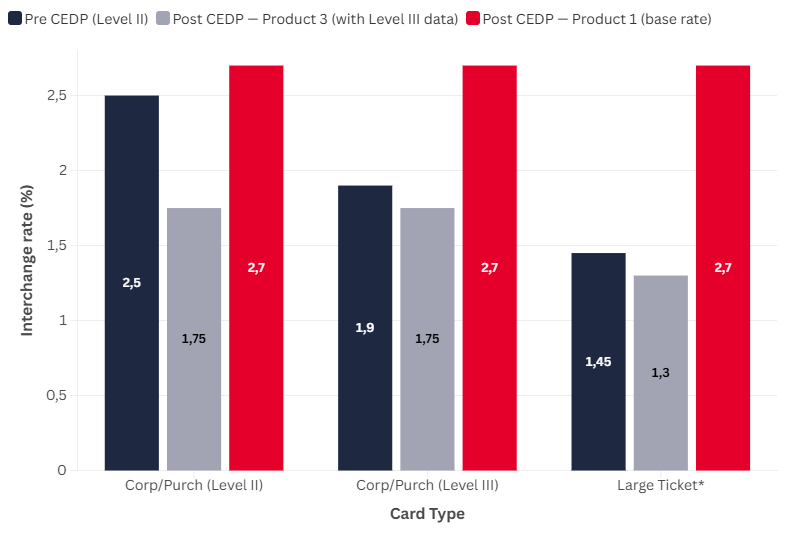

November 2025 – Visa announced a significant revision: the proposed Product 3 rates for Small Business would increase by 65 basis points, with the change taking effect January 2026. Critically, Visa also eliminated the Level II rate category for Small Business cards entirely. Those transactions no longer have a Level II fallback — merchants either qualify for Product 3 by sending Level III data, or their transactions process at the higher Product 1 base rate.

April 2026 – Visa also retired Level II discounts for Purchasing and Corporate cards, an additional headwind for merchants processing those transaction types. Fleet cards retain a Level II category for now.

The Merchant’s Dilemma

The elimination of Level II rates means every affected merchant now faces the same binary choice, but the outcome looks very different depending on card type.

For Corporate and Purchasing cards, the transition to Product 3 still represents a meaningful savings opportunity. Merchants who invest in Level III data compliance can achieve rates that justify the effort.

For Small Business Tiers 1–5, the calculus is much harder. The Product 3 rates for Small Business are significantly higher than what Level II used to provide, meaning even merchants who successfully send Level III data cannot fully recover the rates they previously enjoyed. And those who don’t send Level III data face the full Product 1 base rate, a substantial step up in cost.

Merchants processing Visa Small Business card transactions now face a binary choice:

- Send Level III data: Send Level III data and qualify for Product 3 rates, which offer some savings relative to Product 1, but fall well short of what Level II used to provide.

- Don’t send Level III data: Don’t send Level III data and transactions at the higher Product 1 base rate.

What makes this particularly burdensome is the dramatic increase in compliance complexity. Under the old Level II program, merchants needed only two additional data fields: sales tax and an invoice number. Simple, sustainable, and easy to maintain at scale. Under CEDP, qualifying for Product 3 requires numerous data fields — and Visa’s verification systems actively scrutinize whether the data being submitted is accurate and complete. Merchants flagged for discrepancies risk reclassification, meaning compliance isn’t a one-time achievement. It requires continuous monitoring of every transaction, indefinitely.

For Small Business card merchants in particular, this means being asked to do exponentially more work to achieve rates that are still worse than what Level II used to provide.

Case Study: The $8 Million Invoice

For some merchants, the impact was immediate and drastic. When Visa Small Business Tier 1–5 Level II rates were eliminated in January 2026, one large U.S. manufacturer saw its annual card acceptance costs rise by roughly $8 million. This merchant processes a significant volume of Visa Small Business card transactions across its customer base and felt the rate increase immediately and at scale. The April 2026 retirement of Level II for Purchasing and Corporate cards adds further pressure on top of that.

In summary, any company processing a high volume of Visa Small Business or Corporate card transactions faces similar exposure and may not yet fully understand why their processing costs have increased.

What Can You Still Do?

Redbridge recommends a thorough review of your monthly interchange qualification and merchant statement data. On top of that, and for many merchants, there are offsetting savings opportunities across the broader payments ecosystem that can help absorb these new costs.

Redbridge works with leading merchants to assess CEDP compliance readiness, identify qualification gaps, and build a sustainable monitoring strategy to secure and protect preferential interchange rates over the long term.

Optimize Your Payments Strategy Today

Reduce costs, grow sales, and increase transparency with expert payments consulting.