When fuel prices rise and fall consumers expect airline tickets and other prices to follow suit. With the recent reduction in FDIC surcharges, many large corporations are wondering if their banks’ “deposit assessment fees” will also be reduced.

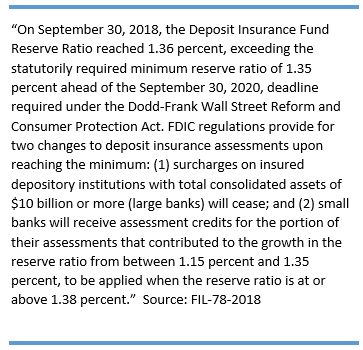

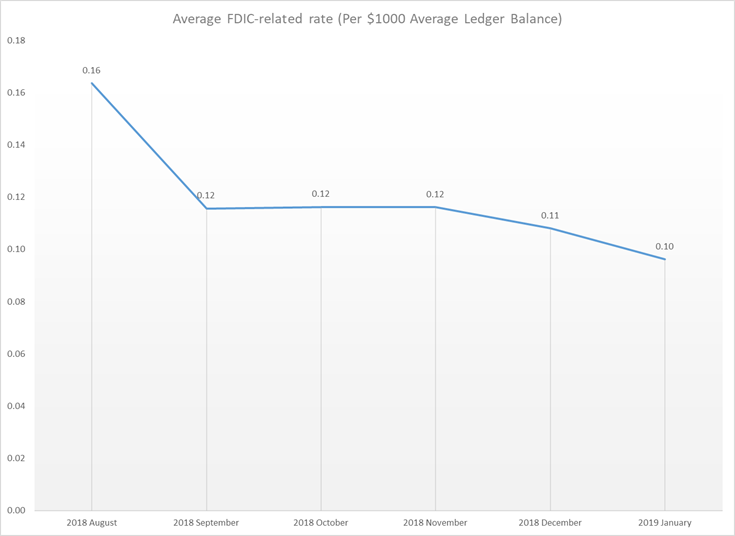

At Redbridge, we monitor the deposit assessment fees charged by large corporate banks on a monthly basis and have seen a rapid decline since November 2018. In fact, four large institutions have completely done away with the fees or reduced them by half since the FDIC decision in November. Banks, of course, have the right to charge customers however they want but I have always felt that the way banks ‘pass through’ FDIC related fees is unfair to the large corporate community, especially given the recent reductions in FDIC surcharges (Image FIL-78-2018) – reductions not being passed on to the corporations bearing the burden of these fees. Only 4 of the 20 major US banks that we monitor have reduced or eliminated the fee since the FDIC eliminated the surcharge a few months ago. The others are continuing to charge between eleven and fifteen basis points on each $1000 in ledger balances held in DDA accounts. Banks should explain why they are continuing to make large corporations pay hefty insurance fees on millions of dollars when only $250k is actually insured.

Reviewing these fees brings up some fundamental questions as to the overall fairness of why only large corporations are charged FDIC assessments or “balance” assessments when other high net worth individuals or other types of accounts are not charged these fees but their money is insured and regulated in the same way as large corporate accounts.

The FDIC may have done the corporations a disservice when they mandated that all banks remove their name from deposit assessments in response to the corporate backlash in 2011 and 2012 when the deposit insurance fund was at an all-time low and the FDIC implemented surcharges to replenish the Deposit Insurance Fund. By removing the name and association officially between the FDIC fee and deposit assessment charges, banks were forced to come up with new definitions for this discretionary fee. One definition is “A monthly administrative fee assessed to address various regulatory and other charges affecting the bank. The fee is set by the bank, in its sole discretion, and is subject to periodic review and adjustment.” With broad definitions like this, the banks now have an excuse NOT to reduce the fees formerly known as “FDIC Fees”. Therefore, the clarification made by the FDIC to stop claiming that these fees were direct pass-throughs (they are not) to help the corporate community may, in fact, backfire. By breaking free from a direct correlation to the FDIC, the fees can rise and fall completely at the banks’ discretion. Therefore, the question you should ask your bank is whether they will or will not reduce their FDIC assessment to corporations now that the surcharge has been lifted. Kudos to banks such as Bank of New York Mellon, KeyBank, Northern Trust, UMB, Deutsche Bank, BOK Financial, and others who have already passed this benefit to their corporate clients.

Will yours do the same?

*Based on Redbridge’s BankScore™ of Global Rates & Fees Source: Redbridge

The Insights from the Data Series

The Insights from the Data is a continuous content series of industry hot topics. In each installment, we share Redbridge knowledge directly from the experts. Visit the Insights section of our website regularly to read about other trending issues.