Understanding Visa’s Commercial Enhanced Data Program (CEDP)

Dan Carter

Senior Director, Payments

In an effort to improve the accuracy and integrity of Level 3 transaction data, Visa has launched the Commercial Enhanced Data Program (CEDP) – a major update that will have real implications for merchants who accept commercial card payments.

This guide outlines what the program entails, key deadlines, and how your business can prepare to maintain optimal interchange qualification and reduce potential cost increases.

What Is Visa’s CEDP?

As of April 12, 2025, Visa introduced a new compliance program targeting Level 3 data integrity. This program is designed to ensure that the enhanced transaction data submitted by merchants, such as line-item details, tax amounts, and purchase order numbers, is accurate and can be validated by Visa Commercial Solutions.

Merchants will be categorized into two groups:

- Verified: Merchants whose Level 3 data is deemed accurate and validated.

- Non-verified: Merchants with data discrepancies or integrity issues.

Only verified merchants will be eligible for Visa’s new Product 3 interchange program, which offers improved interchange rates based on enhanced data submission.

Key Dates and Deadlines

April 12, 2025: The Visa CEDP program goes live. From this point, merchants should start receiving data integrity notifications.

October 17, 2025: The new interchange rates take effect, and merchants must be verified by this date to qualify for the Product 3 rates.

April 17, 2026: Visa will phase out its legacy Level 2 interchange program for Commercial and Small Business cards, with the exception of the Fleet fuel-only Level 2 program.

If a merchant is flagged as non-verified, they will have until October 17 to resolve any issues. While Visa has not specified whether these classifications are permanent, it’s expected that reversing a non-verified status may be a lengthy and complex process.

How Do I Know If I’m Impacted by Visa’s CEDP?

If your business submits Level 3 enhanced data for commercial card transactions, your eligibility for optimized interchange rates under the CEDP will depend on the accuracy and consistency of that data. A review of your current data setup, such as through an interchange scorecard or audit, can help determine whether you’re aligned with Visa’s new standards.

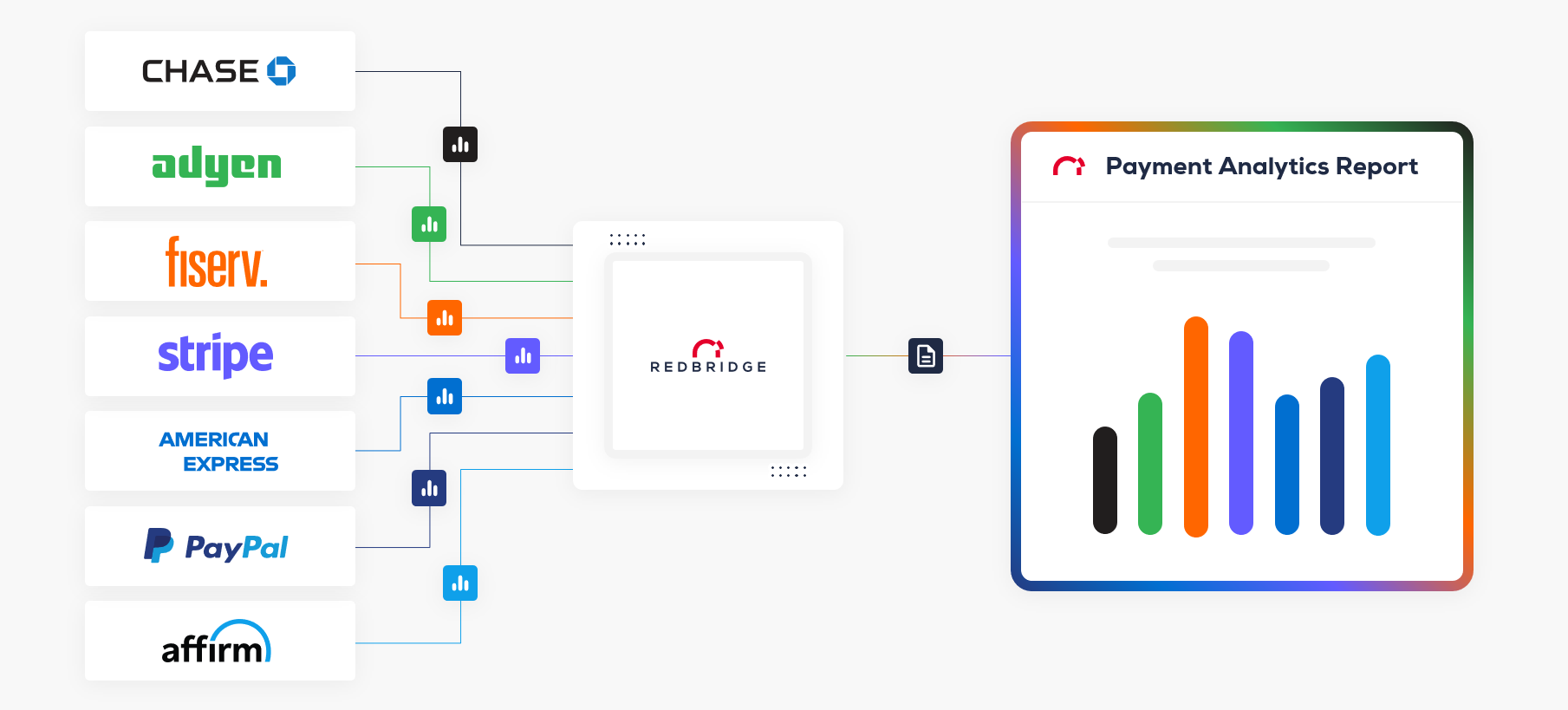

Redbridge has experience in enhanced data validation and can assist in identifying potential issues or opportunities ahead of the October deadline.

What Should Merchants Do Now?

Here are key steps your business can take to stay ahead of Visa’s CEDP requirements:

- Verify your status: Contact your acquiring partner or payment processor to confirm whether you are classified as a verified or non-verified merchant.

- Monitor data integrity alerts: Make sure you have Visa data integrity alerts enabled, and that the right stakeholders in your organization are receiving and reviewing them.

- Assess your current processes: If you’re unsure about your compliance or want an objective review, Redbridge can provide guidance based on industry benchmarks and best practices.

The Impact of Visa’s CEDP

Visa’s Commercial Enhanced Data Program represents a significant change in how Level 3 data is reviewed and rewarded. For merchants, it introduces both risk and opportunity, particularly when it comes to qualifying for optimized interchange rates.

With the October deadline approaching, now is the time to evaluate your current data processes, confirm your verification status, and address any flagged issues.

If you need help understanding how CEDP might impact your business or want to explore where improvements can be made, Redbridge can support you with data validation expertise and analysis tools to guide the way.

To see what this looks like in practice, check out our recent case study on improving interchange efficiency with enhanced data.