CHICAGO AND HOUSTON — January 28, 2025 — Thoughtworks, a global technology consultancy that integrates strategy, design and engineering, has partnered with Redbridge Debt and Treasury Advisory (DTA), a leading provider of payments, treasury and debt advisory solutions, to modernize and scale the digital platform to provide more advanced data and analytics to elevate the advisory experience for clients across all markets.

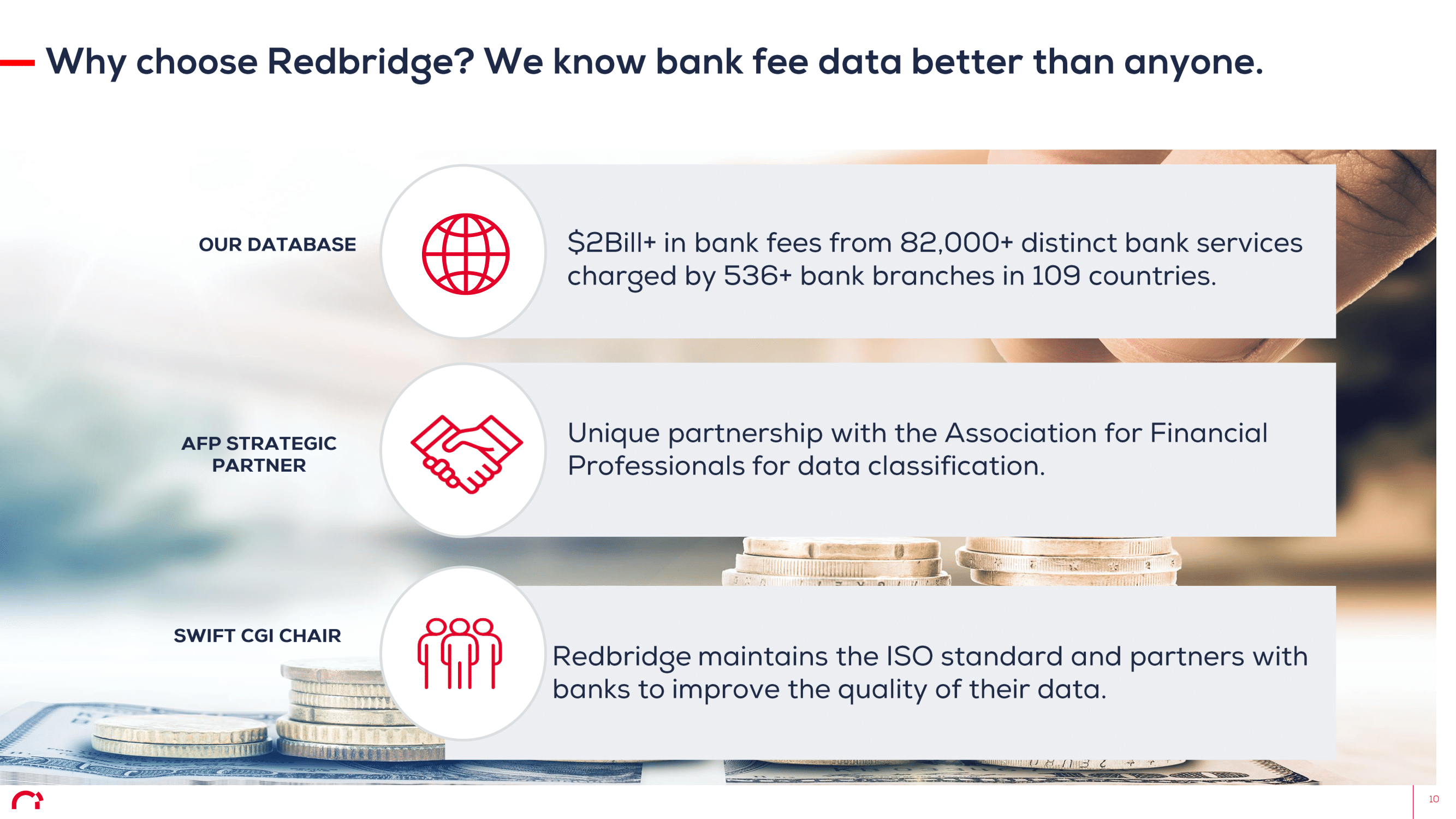

The Payments Industry exists in a state of constant flux. Redbridge helps its clients – companies navigating the world of credit card, debit card and other electronic payment forms – optimize all aspects of the payments value chain. With the rise of big data and competing interests of data privacy, Redbridge saw the opportunity to position itself as a leader in both analytics and advisory, delivering expertly crafted industry intelligence.

Redbridge Debt & Treasury Advisory has built its reputation on delivering best-in-class advisory services in payments, treasury and debt. With a clear vision on the future needs of payments advisory, Redbridge has partnered with Thoughtworks to engineer a cloud-based platform on the industry’s bleeding edge.

This collaboration will enable Redbridge to further streamline data ingestion aspects of machine learning, robotic process automation and other advanced processing capabilities, offering clients unparalleled transparency in payment transaction cost, fees, and interchange rates. The platform on AWS will provide Redbridge with rich, cross-market insights, allowing them to identify further areas for value creation and greater precision in cost-savings opportunities.

“Redbridge has always prioritized strategic investments to provide our clients with unmatched value,” said Dan Carter, Sr. Director & Head of Global Payment Strategy, Redbridge DTA. “Partnering with Thoughtworks will allow us to realize our strategic vision. This partnership brings together our goal of delivering deep learning, data-driven results with an expert interpretation allowing us to positively impact the bottom line for our clients.”

“Across the financial payments landscape, technology is driving business modernization. We’re seeing more clients adopt platform-thinking and cutting edge technology to remain at the forefront of innovation,” said Craig Stanley, Executive Vice President, Thoughtworks Americas. “We’re extremely pleased to bring our 30+ years of experience in integrating strategy and continuous delivery to leaders like Redbridge DTA who are always on the lookout for ways to deliver more value and data-based insights to their clients.”

This partnership marks a key milestone in Redbridge’s ongoing digital transformation strategy. By leveraging Thoughtworks’ global expertise in platform modernization and cutting-edge technology, Redbridge is positioned to deliver greater efficiency and a better client experience across its payments portfolio. As the payments industry continues to change while relying more and more on data, this effort continues to establish Redbridge’s role as a trusted partner as an extension of clients’ payment systems.

Supporting resources:

- Read more about Thoughtworks’ data and analytics portfolio.

- Keep up with Thoughtworks news by visiting the company’s website.

- Follow Thoughtworks on Twitter, LinkedIn and YouTube.

- Learn more about Redbridge by visiting the company’s website or LinkedIn.

About Thougtworks

Thoughtworks is a global technology consultancy that integrates strategy, design and engineering to drive digital innovation. We are over 10,000 Thoughtworkers strong across 48 offices in 19 countries. For 30+ years, we’ve delivered extraordinary impact together with our clients by helping them solve complex business problems with technology as the differentiator.

Media contact:

Linda Horiuchi, global head of public relations

Email: linda.horiuchi@thoughtworks.com

Phone: +1 (646) 581-2568

About Redbridge Debt & Treasury Advisory

Founded in 1999, Redbridge is an independent advisory firm providing comprehensive treasury operations and debt advice to corporations around the globe with teams in Geneva, Houston, Chicago, London, New York and Paris. Redbridge assists companies in optimizing financing and treasury, from strategic design of treasury organizations to creation and implementation of operational solutions. This includes bank and merchant processing fees, treasury systems and execution of debt financing structures.

Media contacts:

US – Michael Denison

mdenison@redbridgedta.com

EU – Emmanuel Léchère

elechere@redbridgedta.com