Card Acquiring – Innovation Without Increased Costs

Chelsey Kukuk

Director, Payments

Pressure from the sales, marketing, as well as digitization, teams to adopt innovative payment solutions and access multiple card networks must make sense from a financial as well as security standpoint. An interview with our experts Mélina Le Sauze and Anthony Schulhof.– What challenges do merchants face with acquiring and processing American Express (AMEX) card transactions?

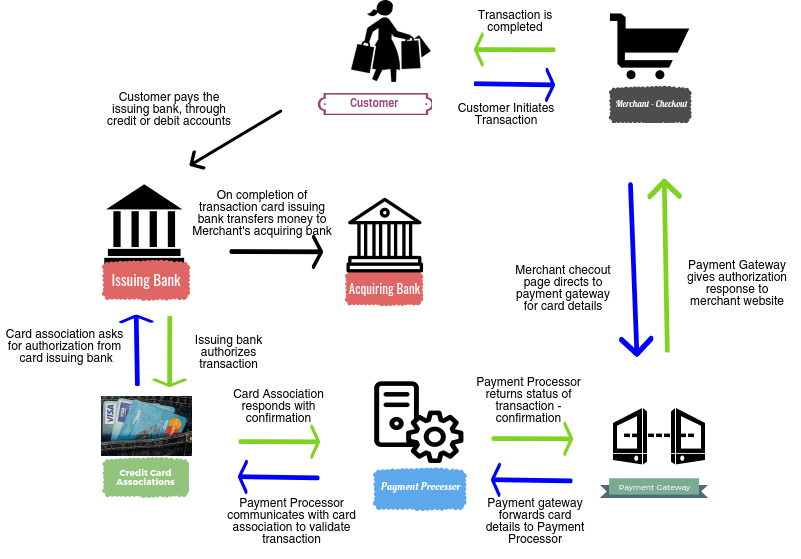

The cost of managing cash for large retailers generally runs into the millions of euros and, on average, 70% of these relate to card acquiring and processing. Historically, banks in France were key players in merchant card processing. However, in the last 10 years, their hegemony has been challenged by the emergence of non-bank providers in charge of terminal maintenance, the provision of acceptance platforms, not to mention FinTechs and Payment Service Providers (PSP), who have invested heavily in the world of electronic banking. The list is not exhaustive, but companies such as Adyen, Ingenico, Hipay, Stripe or Worldline are driving changes in the merchant card acquiring market today.

Furthermore, AMEX Cards, who are one of the leaders in consumer card issuance, are of interest to merchants wishing to attract new customers or retain segments whose purchasing power is generally higher than average. The payments industry has recently developed solutions to facilitate the acceptance of AMEX cards on terminals to meet a wider demand from the large retailers and niche players.

In Germany, Switzerland, as well as the United Kingdom, AMEX and PSPs are key players in the card acquiring chain. In France, they represent an increasing share of the total overall cost of merchant payments.

Whereas in times of crisis, the natural instinct of companies is to preserve the relationship with their banks who commit their balance sheet by providing financing, this does not apply to either AMEX or PSPs. Challenging these providers, therefore, represents a tantalizing route to generate savings.

– What is the added-value of these non-bank providers?

– The new payment service providers, led by Adyen and Stripe, have developed propositions that meet more than just the needs of the finance team. These providers offer agile solutions combining innovative customer journeys, speed of execution and a wider range of accepted payment methods. In addition, they meet the needs of major retailers seeking unique payment solutions on an international scale.

Banks largely cater to the domestic acquiring needs of their customers and do not offer much by way of international solutions. Even banks represented across Europe cannot provide a single unique solution as each local affiliate has its own technical capability and discretion.

Furthermore, in a world where consumer payment habits are evolving fast, banks are struggling to drive the digitalization of payments, preferring, instead, to invest in young start-ups, such as PayPlug and Dalenys, who were acquired by BPCE Group in France between 2016 and 2018.

In companies today, digitalization or marketing teams lead the decisions of innovative payment methods and solutions, with input from the finance team to ensure the profitability of the project, as well as compliance with payment security standards and regulations.

The finance team is, therefore, not the only decision maker in the choice of payment service provider. Nevertheless, for those thinking of selecting a non-bank service provider, there are areas that need to be considered;

From a financial point of view, they can be between 30% and 50% more expensive than those of banks.

The solutions from non-bank providers are frequently integrated from the cash register system right through to the credit on your account. It is therefore very complicated to “back out” and change providers after the implementation of such solutions.

– What is the added-value of Amex?

– Accepting AMEX cards does not have the same importance depending on the sector of the company’s activities. Indispensable in the hotel industry, air transport and the luxury goods sector, its’ wider acceptance is driven more by a desire not to stand in the way of a purchase or to attract new customers for large retailers or specialized outlets.

The pricing schedule of AMEX incorporates many subtleties (inbound fees, wholesale vs retail rates, etc.) which are not always easy for the merchant to comprehend. The central element of this grid is a commission rate, which is unique in that it is never the same from one country to another (AMEX speaks of the market), not from one sector to another. The different commission rates according to economic sectors and countries is justified by the fact that the AMEX network brings a different added-value depending on the type and location of the merchant.

This pricing model makes it possible to apply high rates to merchants in the luxury and hotel sectors. Conversely, when AMEX wants to set up in a sector where its added-value is less compelling, it does not hesitate in offering competitive prices, similar to the grid prevailing in the mass retailers. Depending on the industry, the AMEX commission rate varies from simple to three times, or even more.

– How to optimize the non-bank service providers along the processing chain?

– Competition between non-bank service providers is increasing every year, with the appearance of new entrants offering services across the value chain. To optimize your relationship, it is essential to identify the services required so as not to have an inferior offer or have to asses a wide panel of providers. Often, PSPs propose an all-encompassing offer, where any service gives rise to a transaction fee or subscription; acquisition, processing, fraud prevention … This grid is negotiable for those who compete.

– And what about Amex?

With no real equivalent, AMEX is a provider relatively closed to negotiation. Their reluctance is based on the pricing integrity rule, according to which the network guarantees to apply a single commission rate within the same sector.

This “a sector equals a price” rule is more a matter of commercial policy than reality. Experience has shown that within the same sector, there are price differences in the range of 33% to 50% depending on merchants.

The fact is that, in today’s world, AMEX needs to gain market share amongst new merchants and at the same time acquire a maximum of “physical” customers using their consumer cards to legitimize their potential to merchants. This situation leads AMEX to rebalance its relationship with merchants and makes it possible to open an effective negotiation, which can yield significant savings, when accompanied by precise and formal analysis.

Achieving the conditions of a most favored client is not easy and requires:

– Solid arguments

– An extensive knowledge of the internal organization of AMEX and its decision-making process

– A precise and exhaustive analysis of the situation (volumes currently processed, evolution of volumes over the last years versus evolutions of total turnover and acquiring turnover, type of end customers, breakdown of goods purchased from the merchant by AMEX card holders, average transaction amount, …)

– An extensive experience to conduct a quick and efficient negotiation.