Treasurers fear that efforts to negotiate bank fees might cause a punitive reaction from their banks. This story we tell ourselves isn’t true.

Imagine you are lost in a desert with only a compass to help you navigate. It’s an old compass, and you decided to head North without being totally sure that you are actually heading North. This uncomfortable situation is the best way to describe the hazards of managing a banking relationship.

You quantify your business the best you can, but you rely on your banking partners to tell you if your relationships are fair or not. Worse, you fear that if you’re not giving your banks enough business, there will be consequences.

When the time comes for negotiations, many corporate treasurers fear that efforts to lower or negotiate bank fees might cause a punitive reaction from their banks, even the loss of a capital source.

When talking specifically about cash management or, holistically-speaking, transaction banking, treasurers and CFOs tend to underestimate the value transaction banking provides to banks and the banks’ appetite for it.

The importance of transaction banking to banks

Bank billing is complex and confusing. Looking at the sheer volume of AFP Service Codes©, we estimate there are approximately 2,500 ways to price transaction banking, creating a Gordian knot of costs almost impossible for treasurers to decipher and track. While a rise in an individual fee may be slight, total fees get higher each year – a financial equivalent of death by a thousand cuts.

Whenever the subject of bank fees arises between corporate treasurers and banks, bankers justify bank fees by the complexity of the billing system, the constant increase in regulation, the cost of payment factories, and the investments they represent. In discussions to lower fees, banks often claim that due to the high cost of the credit relationship, they need side or ancillary business to compensate for the cost of risk and – the biggest loss-maker – the credit facility. Sometimes, they imply that it might not be possible to maintain a credit relationship with a reduced rate.

Though the threat can be daunting to a corporate treasurer, it is most likely all bark and no bite.

In our experience from 20 years of negotiating bank fees and providing risk-adjusted return on capital (RAROC) analyses for global Fortune 500 companies, we’ve never seen an impact on the lending side because a corporation negotiated their bank fees domestically or globally. Never.

On the contrary, we’ve seen banks offer a “bank fee holiday” just to keep a client’s business. (A bank fee holiday is when the client doesn’t have to pay bank fees for a given period.) Why would banks offer this to their clients if bank fees weren’t attractive from a capital, liquidity ratio, day-to-day proximity with the client, and long-term recurring revenue standpoint?

The question is not, “Should I negotiate?” but, “How should I negotiate?” Being prepared and making negotiations a clear strategic project for your business is key.

On the other hand, banks might claim that transaction banking or payments and collections are barely breakeven on a cost-to-income ratio.

Every bank argument is right, and, at the same time, every bank argument is misleading and incomplete for several reasons:

- Favored access

Banks providing cash management services to a corporation have a natural advantage over their competitors through an existing relationship with the client – a day-to-day contact that is priceless for banks. (Not to mention that a conversation with the treasury team can also lead to a big M&A transaction.) From a treasurer’s perspective, a history of working together and long-standing banking relationships favor the in-place bank over the unknown qualities of a new banking relationship. But how much is the relationship worth? - Sustainable and growing income

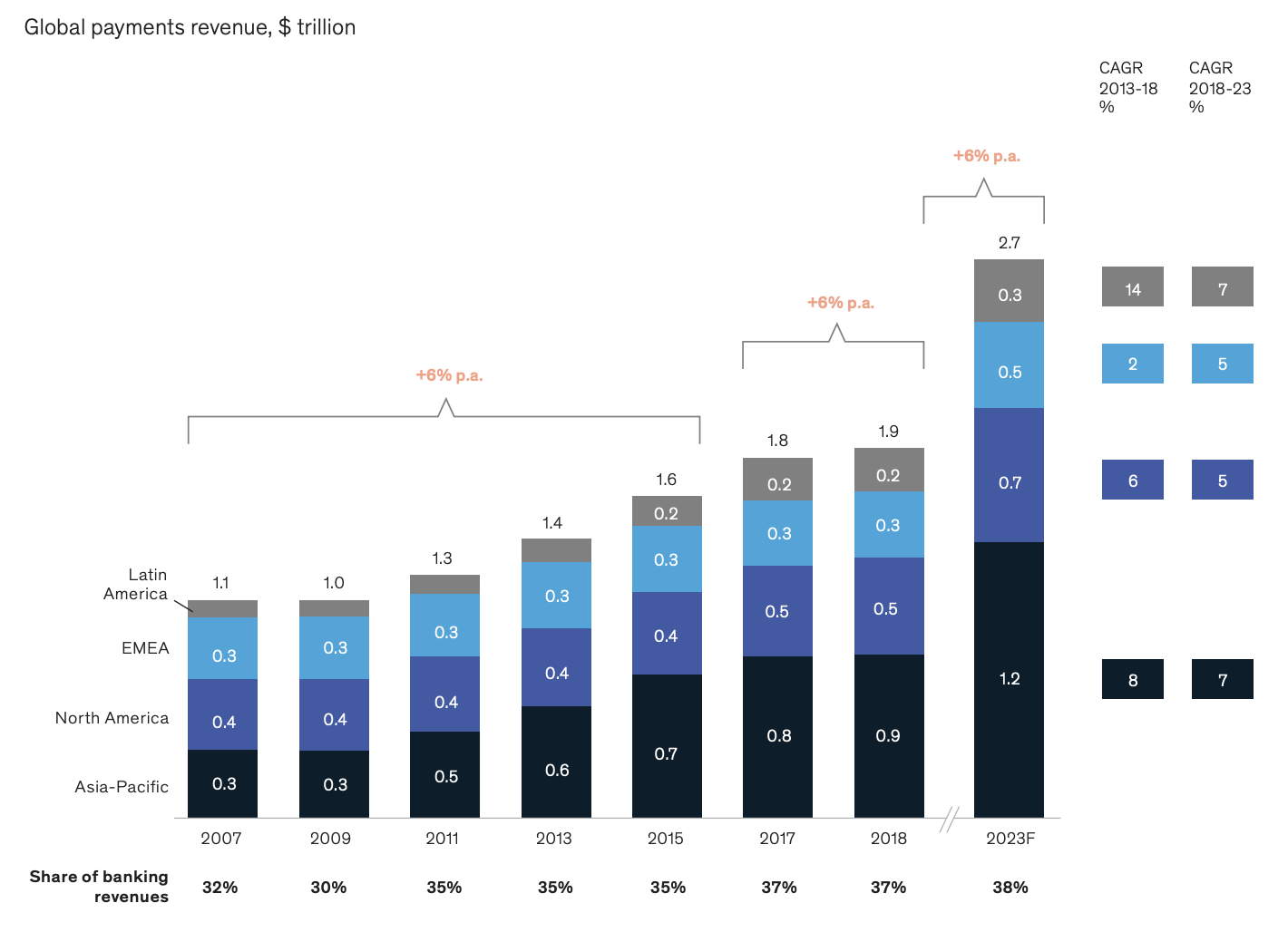

Unlike other types of revenue-generating side business – M&A, debt capital markets, equity capital markets – transaction banking and bank fees provide banks a growing, reliable and recurring source of low-risk and non-capital-consuming revenues. According to a 2019 report by McKinsey & Company, global payments returned to its “established pattern of steady yet strong performance,” with revenues totaling $1.9 trillion in 2018, a 6% increase from 2017 (Exhibit 1). Global transaction banking accounts for roughly 50% of global payments revenues, according to the report. North America is the second-largest region for bank fees in the world and one of the most profitable for banks. Just check how your bank account statements inflate every year. An efficient bank fee negotiation is a negotiation that locks in every single price point (there’s 280 on average per billing statement) in your account analysis statement for at least three years.

Exhibit 1

Source: McKinsey Global Payments Map

- Increased profit margins

Most of the bank’s transaction processing costs are fixed, i.e., facilities, equipment, staff, software, and network. As the volume of transactions processed by a bank grows, the per-unit cost of each transaction declines. After reaching breakeven, the difference between fees and marginal or direct processing costs is all profits. Accordingly, the loss of a large corporation’s transaction fees can significantly affect the bank’s financial position more than the loss of the direct fee revenue. Our research suggests that the intrinsic profitability of global transaction banking – letters of credit, payments, balances, short-term lending – is about a 25% return on equity. - Liquidity relief

Concerns about the international banking system’s financial stability led to the establishment of the Committee on Banking Regulations and Supervisory Practices in Basel, Switzerland, in 1974. Since its establishment, the committee has adopted three different sets of regulations (Basel I in 1988, Basel II in 2004, and Basel III in 2010) to reduce excessive risk-taking by international banks. A constant and stable bank-client relationship can deleverage regulatory pressure on liquidity ratios. The liquidity coverage ratio (LCR) and the net stable funding ratio (NSFR) are two main liquidity ratios stressing bank balance sheets to an extreme. Corporations that have a stable, long-term relationship with their banks enable the latter to deleverage the pressure of these ratios. This is never factored into the pricing. It should. Corporate treasurers purposely omit transaction banking in negotiations with their banks because of a perceived link between fees and capital availability. Many corporates mistakenly associate their willingness to accept higher fees with increased liquidity and loans. In many cases, corporate teams do not know how much the relationship serves the bank. Our research shows the average return on equity in a relationship is about 15%, while banks need about 10% to cover the cost of equity. We have seen studies where corporations paid as high as a 40% return on the bank’s equity and thought they did a good job by negotiating everything but transaction fees.

Negotiating transaction services

Fair agreements result from complete knowledge and transparency. Most corporations are in the dark about the returns they provide to their banking partners. Banks are not obligated to supply the information, so it is up to the corporation to recognize the costs and adjust its negotiation strategy.

Whether or not a corporation elects to negotiate transaction fees should be a strategic decision that’s made when there is an understanding of the importance of each issue to the opposite party and its impact on company outcomes. Corporations spend millions of dollars each year to squeeze excess costs from their operations. Transaction fees are no different than any other operating cost.

Treasurers should not let the bankers’ crying and gnashing of teeth disguise the importance of transaction services to the institution. It has been and will remain an attractive business for banks, especially in the era of Basel II and III. We recommend corporate leaders treat bank services as they do all other vendors and suppliers to ensure their business is getting the right services at the right prices.

But as always, when the best strategies and tactics fail, it’s typically due to poor execution. Bank pricing is complicated on purpose. Think outside the box and negotiate your fees with process and methodology. And always remember, if you don’t ask, you don’t get.