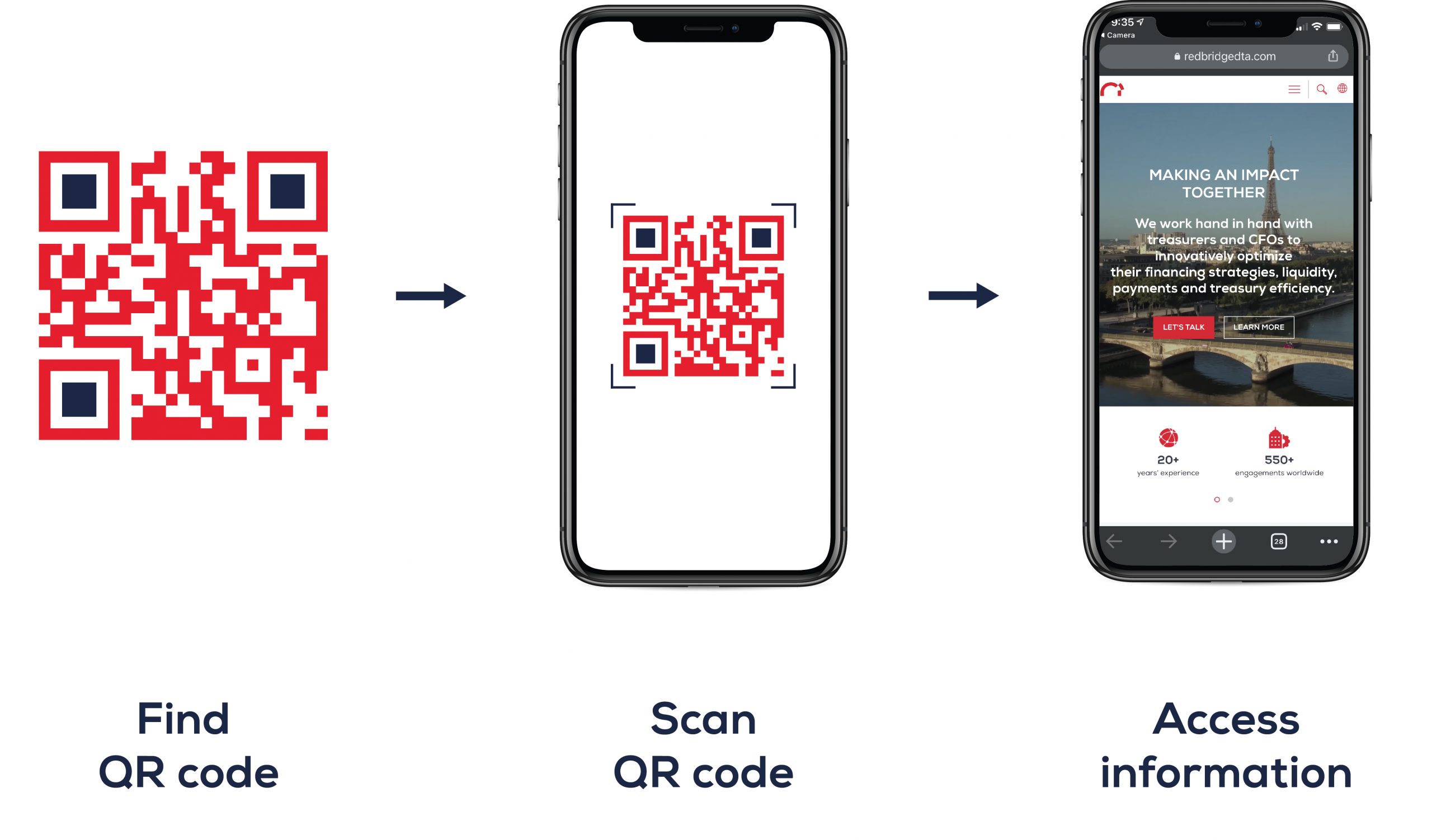

We have all seen QR (Quick Response) codes in our daily lives. These scannable, square-shaped, two-dimensional barcodes serve a similar purpose as traditional barcodes, but they can hold much more information.

What is a QR code?

QR codes store more than 4,000 characters or 7,000 numbers and are ten times faster to read than a traditional barcode. Most QR codes can be read even if they are partially damaged or incomplete because the data can be split across multiple segments that reconstruct the original content when scanned. Their square shape gives them the ability to be scanned and read either vertically or horizontally.

When did QR codes become mainstream?

Invented in the 1990s by a Japanese auto parts manufacturer to simplify inventory tasks, QR codes hold large amounts of data avoiding the need to use multiple bar codes. The codes evolved quickly to include uses geared toward business and marketing. Since the information held in QR codes can contain links to websites and store large volumes of data, marketers quickly recognized potential applications for using this technology.

Why did they fade in popularity?

As simple as it seems from the user perspective, the technology was a bit ahead of its time for mainstream adoption. Even in the early 2000s, when handheld mobile technology evolved quickly, people didn’t find it particularly easy to incorporate QR codes into their daily lives. It may not seem like it now, but there was a time not too long ago that even smartphones didn’t have the capabilities to quickly process the codes. A user would have to download or open a separate QR code reader app to scan them. Now our phones come equipped with necessary technology from the factory, which has created the perfect environment for the re-emergence of this seemingly simple technology.

Why are QR codes relevant again?

The QR code has reemerged in recent years. Smartphone technology has seamlessly incorporated QR readers into the base camera apps, and quick launch buttons make it easy for people to scan codes. But it wasn’t until the contactless revolution in the midst of a global pandemic that made QR codes became a household commodity.

What are their current uses?

QR code technology is currently experiencing a tremendous boom. Consumers and businesses throughout the world are creating new uses within a variety of industries, including marketing, accounting, logistics, tourism, IT, T&E and even banking. Because of the newly promoted ease of access, daily use applications — including touch-free payments, website links, and displaying multimedia — are propelling QR popularity to new levels. Nearly 3 decades later, the original developer, Hara Masahiro has spoken out, observing:

Is global adoption of QR codes the future for payments?

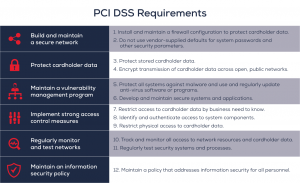

The benefits of using QR codes for e-commerce may seem less obvious. However, the security and cost advantages of scanning QR codes for payments could reduce the need for internal card data collection and retention. With QR code payments, the entire process takes place on the customer’s device and any data transferred is encrypted.

On top of the security aspect, businesses can use this contactless revolution as a way of collecting valuable customer information by attaching surveys or other forms to the code. In the days of gathering data and strengthening the KYC process through acquired information, businesses are amassing customer databases through QR codes to provide a more seamless customer experience.

For these reasons and others, QR codes may be the future of contactless payments. Many countries around the world are already adopting and standardizing QR code payments. For example, the Central Bank in Brazil announced a new national QR code standard to make mobile payments more universal during the pandemic. India is reducing the amount of cash circulating in its economy by implementing QR code payments.

The growing adoption of QR code payments and increasing demand for digitalized payments across emerging countries will create many opportunities in the next few years. Adoption of QR code payments among merchants will steer market growth and require fast, hassle-free transaction services among customers.

Where are they the most popular?

Convenient-to-use QR code generator tools are becoming more popular every day around the world. As the popularity continues to increase, more companies and consumers are taking advantage of the benefits that QR code technology offers.

Different countries are taking different approaches to integrate QR codes into everyday tasks. China has become a leader in QR code usage. QR code payment has been the long-standing norm in the country. Payment terminals do not exist, and more than half of the population in China use QR codes in their lives. In the US, businesses are experiencing a significant increase in contactless payments, and QR codes are definitely becoming increasingly popular in Europe. For example, Northern Ireland is implementing its own unique twist for contactless shopping in convenience stores. Through partnerships with frontline organizations, Malaysia and the Philippines are supporting QR code scanning as a standard procedure for donations.

Are there downsides to QR codes?

A large number of smartphone owners simply are not using QR codes. For example, a QR code on a poster that people routinely pass by could quickly take them to a website or registration page for an event upon scanning. However, even with such an easily accessible QR code available on the poster, few people are likely to stop and interact with it.

So let’s not overestimate the importance of QR codes. It’s just one way of encoding information. The downsides, in the public eye, come from the possible tracking capabilities of the website destinations connected to some QR codes. Many consumers do not enjoy the fact that when a QR code takes them to a website, they can be bombarded with privacy policies and take on the risk of third-party tracking when all they want is a drink menu. One solution to this issue is to use an anti-tracking browser, but that adds an inconvenience.

Security attacks are another risk. Malicious QR codes can initiate phishing scams on unsuspecting scanners. So let this be a warning — just like the ones from your work IT department on email links — do not haphazardly scan every code you encounter.

How long will their popularity last?

The longevity of QR codes resides literally (and figuratively) in the hands of the consumer. The people holding the mobile power will determine whether this technology becomes a staple for transferring information and initiating a payment process. The steep rise of mobile technology will be a hard one to turn back. Therefore, it’s quite possible that the only thing to limit the use of QR codes is the development of a similar technology that would directly replace their function.

However, just as barcodes have not driven numeric representations out of product packaging, it’s unlikely that QR technology will disappear. No longer seen as a revolutionary technology, QR codes have solidified their place in the daily lives of consumers and merchants. Current research predicts that the use of QR codes for electronic payments will surge more than 300% over the next five years.

Nate Guers & Lucie Kunesova

A special report on the cash management & payment trends that will transform your treasury department in 2022

The growth and vitality of the payments industry has fascinated all observers during the past two years of the pandemic. Now with recent geopolitical developments arising from the Russia-Ukraine conflict, it is being tested again.

Our new publication analyzes the most prevalent trends and innovations in the treasury world today.

Included in this publication:

- The Global Resurgence of QR Codes

- Choosing the Right Payment Terminal in an Ever-Changing Environment

- The Rise of Buy Now, Pay Later

- PCI Compliance in an E-Commerce World

- Where Do Banks Stand in the Race for Digital?

- Virtual Accounts, Which Companies Should Implement Them?

- The Future & Alternatives to SWIFT GPI

- Global Digitization in the Depository Space

- “Switching Banks Was the Right Decision”: An Interview with Olivier Bouillaud from Albéa

Download the full publication