At some banks, paper Account Analysis Statements are still priced lower than electronic versions of the same report in PDF, CSV, or EDI 822. One bank is actually charging its corporate clients up to $175 per account monthly to receive an electronic version of the same report that comes in paper form for $25! That does not make sense! writes Bridget Meyer, senior director at Redbridge.

Back in the 1980’s, banks began to offer new types of accounts designated to track and report balances, transaction volume and pricing for distribution to its clients for a monthly manual review. These reports known as Account Analysis Statements have become a standard business practice for all major banks doing business with large corporations. This is also considered the bill corporations receive showing all account activity and unit pricing. And since banks could no longer pay interest on checking account balances, the Earnings Credit Rate, or ECR, became a competitive feature offered to offset the fees a company might be charged for transactional services. This encouraged deposits which the banks used to lend out in the form of loans. Basic ABC’s of banking! The Account Analysis Statement helped companies understand their bank fees which had always just been deducted from their balance once a month.

Almost 40 years later, banks are trying to reduce their costs by eliminating paper reports, which seems to be the norm with banks in the United States. It might seem that all bank statements and notices are moving to electronic and that is great! Not so fast! It might surprise you that at some banks, paper Account Analysis Statements are still priced lower than electronic versions of the same report in PDF, CSV (Comma-Separated Value), or EDI 822 (Electronic Data Interchange). Well, at least one bank is actually charging its corporate clients up to $175 per company ID monthly to receive an electronic version of the same report that comes in paper form for $25! Wow, that does not make sense!

Isn’t it a lot cheaper for the bank to produce electronic versions? Yes, but some questions have been raised as to the willingness of some banks to encourage transparency and reconciliation of monthly bills. These would allow clients to easily identify incorrect charges, new charges, errors in services, etc. Some banks actually have 4,200 priced services for corporations in the U.S. alone. Finding errors in the billing is extremely difficult if not impossible with paper analysis statements. The most desired format for the largest customers is the EDI 822 file, received via transmission without any human intervention on a monthly basis. These can be uploaded into bank billing systems or sent to third parties to reconcile.

Not all banks are guilty of steering customers away from electronic versions, but you want to be sure your banks are not one of those charging $175 a month per account. Some banks actually offer all electronic formats for free just to reduce cost of production and mailing. That is great. But some electronic formats are better than others. And some offer only one electronic format for free, and that format is typically a PDF format, probably downloadable from the bank’s website.

A PDF formatted account analysis is basically a visual photo of the paper statement, leaving any electronic review impossible. The PDF (and paper) version of a statement is legally considered the ‘statement of record’ describing accurately will actually be debited from a customer’s account.

Receiving a CSV or PDF is not always free. One large regional bank, charges $5.00 to download a PDF and $10.00 per month for a CSV version of their invoice with no available ‘free’ option. The average account analysis statement is hundreds of pages for a large corporation. Reviewing the charges each month is not only a chore, it requires significant data entry. Most of the large banks are now offering a Comma-Separated Value (CSV) version of the analysis statement for added convenience but customers beware. Excel will round the numbers and create slight variances from the PDF version.

So the motives of any bank that only allows a free or very low cost PDF or CSV formatted account analysis statement might be questioned. Are they worried its customers might find errors? Perhaps.

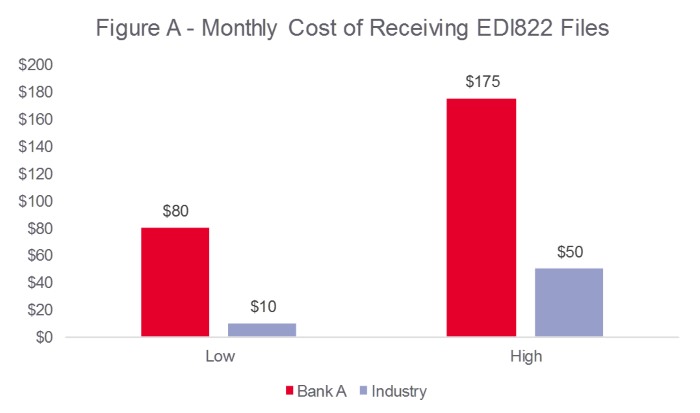

Figure A shows the average monthly cost to receive an EDI 822 electronic account analysis statement from the largest 16 banks in the United States. The differentiation should surprise you. Two of the big money center banks offer free downloads of customer bills in any format (EDI, PDF, or CSV). Another money center (who the author is referencing as Bank A) charges $175.00 per month per Customer ID to send the billing information in EDI format and provides CSV’s to a very limited few. Even if a bank does charge a standard price to provide electronic statements, customers have a 44% chance of getting that fee waived from all but one bank – the one charging $175, according to Redbridge Analytics.

You might be surprised that some of the major banks actually have ‘product managers’ assigned to the revenue generated from Account Analysis Statements. Those banks are very closely managing their services and might be motivated to price their most efficient and lowest cost alternative at a very high price to boost profitability. They might also be enjoying the lack of transparency.

With all of this talk of about prices of a bank’s invoice to you, you may now be asking the philosophical question: why do banks actually charge their corporate customers to receive that very bill, or Account Analysis? It does seem odd from an Accounts Payable perspective, but that is another story for another time.

Since some banks are steering cost conscious clients to download a PDF version of their 450-900 pages bill and happily auto-debiting their fees each month, the need for due diligence of bank charges is great. Billing errors are incredibly common. And bank fees could be very significant… if not one of the highest vendor costs in a corporation. It is time for all banks to become transparent and price EDI 822 electronic Account Analysis Statements so that the corporate treasurer has a reasonable electronic method of reviewing these bills at a reasonable cost.