In this article, I would like to focus on four key topics:

- Why should clients pay positive rates on their short-term debt while their deposits are subject to negative rates?

- Is the bank best placed to support you when it comes to digitalizing your finance processes?

- Should you always try to optimize your working capital?

- Have we already seen the worst of Covid-19 and its impact on the economy?

Why should clients pay positive rates on their short-term debt, while their deposits are subject to negative rates?

– Let’s start with a normal day for an average corporate treasurer. Last week, they drew EUR 100m from their RCF, at, say, a 100bps margin for one-month tenor. However, today they’ve received the equivalent of EUR 50m from one of their Australian subsidiaries after an earlier-than-anticipated customer payment. Yet their policy requires them to convert that payment into euros and then deposit it with one of their euro banks. An early repayment of their RCF drawdown would come at a cost, but depositing EUR 50m also comes at a cost: 50bps. The reason for this is the ECB’s negative rate policy. So, the treasurer’s net cash position is negative by EUR 50m, but they have to pay interest on EUR 100m at 100bps plus 50bps on EUR 50m. Clearly not an ideal situation.

However, could things be different? Could you benefit from negative rates too?

Banks often forget to mention an alternative when it comes to euro short-term funding: the NEU Commercial Paper (CP) market. Even if banks are involved in the NEU CP market as investors, they rarely suggest it as an option to their corporate clients, even though funding rates have been negative for several months. Why is this? Often, the investing arm of the bank fails to discuss it with its corporate arm. This is regrettable, as advising customers to source more funding from the NEU CP market would not only help clients reduce their costs of funding but also help banks to reduce their exposure to low-return RWAs (ie Risk Weitghted Assets).

We have advised close to 40% of the new entrants in the NEU CP market, and all of them have enjoyed a major improvement in their funding costs.

Is the bank best placed to support you when it comes to digitalizing your finance processes?

– Let’s now consider a trendier subject within finance: digital transformation.

Everyone has heard examples of digitalization in finance. Think about the idea of Amazon becoming a bank, offering corporate loans, accounts (or “wallets”), and co-branded payment cards. Another example is the rise of APIs (Application Programming Interfaces). These are based on old technology, but have achieved new-found fame. APIs have re-emerged with the rise of Open Banking, which is offering retail and institutional clients alike new options to access their bank accounts and send payment. Faster, cheaper and, arguably, safer…

But consider the following point. Apart from asking you to use their online portals (which are often similar), how often have your banks helped you better leverage your data, or suggested that you use APIs to better connect between your treasury management system and themselves? By the way, do they offer a single API globally, or one per country?

As an anecdote, in my previous role as a banker, I was asked by clients whether the bank could help them optimize their cash flow forecasting. Each time I shared the request with the Product team (which was arguably a great business opportunity), the Cash Management colleagues told me that such a request was for software providers, not banks… Funnily enough, that solution was launched by a few banks last year. When I asked how they leveraged Artificial Intelligence to provide that service to our clients, I faced an awkward silence followed by the promise to provide that option within four years (which in IT terms often means ten years).

Last year Redbridge collaborated with a Fintech firm to offer AI-based cash flow forecasting to corporations. To be fair, implementing AI is everything but a plug-and-play solution. But this story reminds us once again of the importance of listening to customers to identify their needs and being agile enough to offer a solution quickly. Neither does ignoring what new competitors can offer.

Core banking platforms are over 20 years old in most instances. For international banks, despite sharing the same names in the various regions in which they operate, most of the time they are a collection of very different platforms, communicating as well as they can via multiple layers of other platforms. Making a change to one of those platforms involves the not inconsiderable risk of derailing the rest of the system. A good example of this is the black-out that TSB went through when switching away from the Lloyd’s banking platform. That incident was a powerful reminder to many CEOs of banks that their platforms need to be handled with extreme care, and that they could lose their job if mistakes are made.

The result is that most of banks’ IT budgets are dedicated to keeping their existing systems operating, with the rest allocated to innovation. These figures make it easy to understand why neobanks can innovate faster than many incumbents as they leverage state-of-the-art platforms, without even mentioning the different kinds of culture in the two environments.

The bottom line is that even if a bank is talking more and more about digital transformation, you need to make sure it’s truly innovating and making a genuine attempt to meet your needs.

Should you always try to optimize working capital?

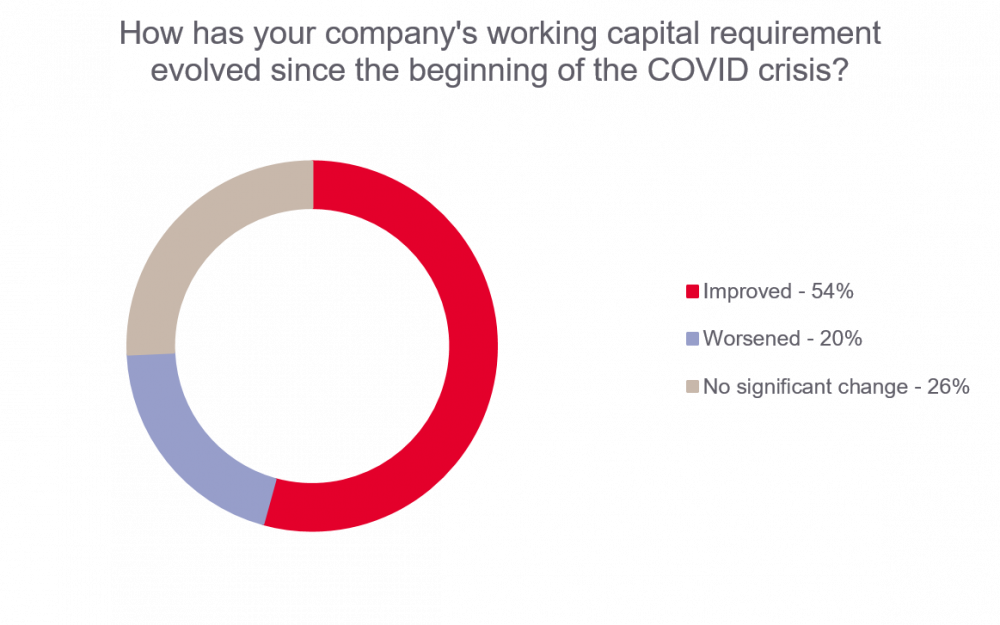

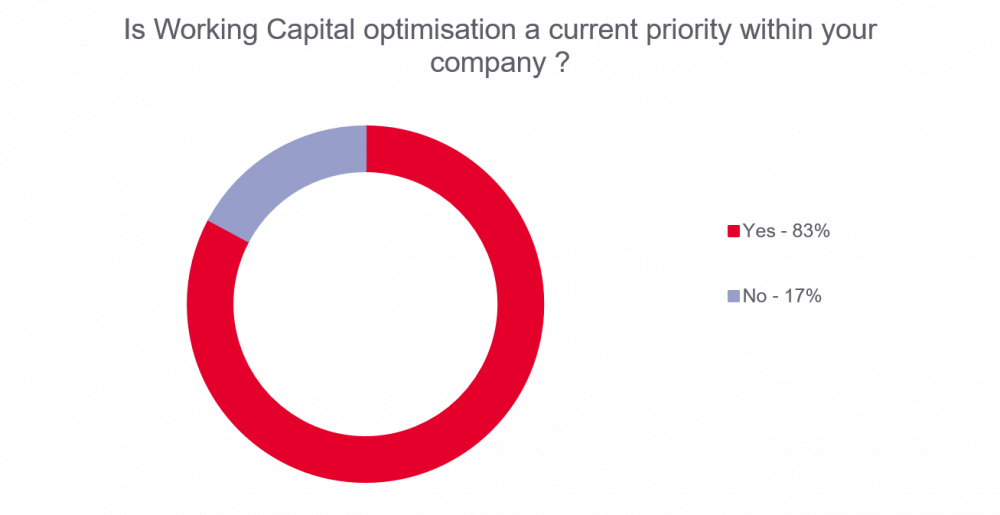

– Ten years ago, working capital optimization was essentially a topic reserved for treasurers, but slowly but surely it’s become a key consideration for CFOs. The Covid crisis has acted as a catalyst to accelerate an already existing trend.

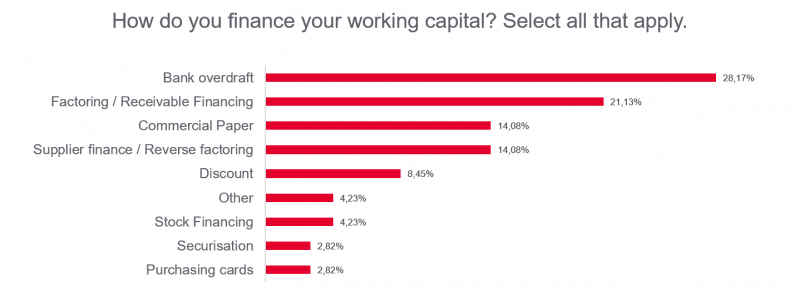

Liquidity does not only have a cost: it’s vital for any company’s survival. This is why banks are rediscovering old solutions like Receivable (or Factor) Financing or Supplier Financing. In essence, they are helping you improve your Day Sales Outstandings (DSOs) and Day Payment Outstandings (DPOs) without increasing your debt, and hence achieve a lower Net Debt/EBITDA ratio (to be confirmed by your auditor, as always). It may also help you better comply with some financial covenants and reduce your cost of funding.

Is your bank willing and able to help you optimize your working capital then? Well, yes and no. Yes in most instances, and for obvious reasons.

The “no” is more complex. Some corporates currently enjoy material liquidity buffers. Even better, increasing liquidity further would not trigger an improvement of their external bank ratings. So as long as you keep some liquidity (in case of bad times), why don’t you use part of it to pay your suppliers faster in exchange for early-payment discounts? True, your liquidity would fall, but by reducing your direct costs, you would improve mechanically your EBITDA. It’s therefore an interesting trade-off between liquidity and profitability. Not to mention how some suppliers can take advantage of obtaining fresh liquidity faster, when they often struggle to source additional bank funding.

The question, then, is what is the appropriate level of liquidity to maintain in order to protect your existing rating? Banks used to have in-house Corporate Finance or Rating teams to run this kind of analysis, although their focus was more on investment banking products than receivable financing. But years of cost-cutting have resulted in many of those teams being dismantled. As a result, it is now difficult to get that support from banks, all the more so as it does not generate additional business for them.

Redbridge has developed a rating advisory expertise over the course of several years as we believe it is key for our clients to be able to understand how to optimize both their external (if any) and bank ratings. As long as there is a market need, we shall support our clients around those questions.

Have we already seen the worst of Covid-19 and its impact on the economy?

– When the Covid crisis broke out, most of us knew we were facing a threat we were not properly prepared for. Central banks quickly realized the potential impact on banks, essentially through an increase in non-performing loans. Defaults were expected to rise. Hence there were some direct requests to banks, depending on the region, to check their models and review their provisions accordingly. Some banks made judgement calls to downgrade those of their clients that were expected to face the greatest negative impact from the crisis. Those customers, often without knowing it, faced downgrades by one or two notches, which increased their RWAs and reduced their profitability. Add to that some automatic provisions (IFRS-led) and the pressure to either reduce loans or increase margins (if not both at the same time) suddenly became a tough reality for many corporates.

Unfortunately, all this is not yet over. As we explained, the downgrades were applied to some clients, not all of them. We now know that most companies have unfortunately been impacted negatively by the pandemic. However, the scale of that impact will only be apparent in their 2020 full-year financials. As most companies close their accounts in December, banks will have started reviewing those financials in April 2021, which may lead to additional downgrades as part of their annual review processes. The surprise may be even bigger as, for instance, banks asked were by governments/regulators to be particularly “understanding” when receiving waiver requests, sometimes giving the false impression that they would always show the same levels of support. Unfortunately, there are signs that banks are now less keen on granting waivers than they have been over the past months.

So will you be one of those corporates to be downgraded by your banks? Will all banks adopt the same approach at the same time? Will that impact your pricing and the amount of your facilities? If so, to what extent?

More importantly, have you run some stress tests to assess the potential impact of banks’ decisions and identify funding contingency plans? If the answer is no, then it may be worth considering such an option. Purchasing teams often assess the solidity of their suppliers and alternatives in the event of an unexpected crisis. Why not do the same with your banks? Besides, do you often discuss with your banks to find out how they are rating you and what is driving your bank rating?

Our advice, based on providing 20 years of support to our clients, is simple: run some scenarios and design contingency plans, which may include finding new or alternative partners and diversifying your funding options.

– One last important point. This article should not be read as a blanket criticism of banks. Banks are still at the center of our economies, and despite ten years of Bitcoin, we cannot yet consider a system without banks. I’ve had the pleasure of working with countless professional bankers who have worked hard to support their clients. What’s more, banks are following different paths. Some in the US, for instance, have invested heavily in new technologies to genuinely make a difference for their clients. This is an excellent development.

Your bank is one of your key partners, but every partner needs to be assessed regularly and benchmarked against others. After all, a bank is a supplier to your company.