There is still appetite for highly-rated corporates, but the size of financing must be consistent with a company’s business plan. Since last summer, credit committees have been becoming increasingly cautious and this trends looks set to continue, writes Muriel Nahmias.

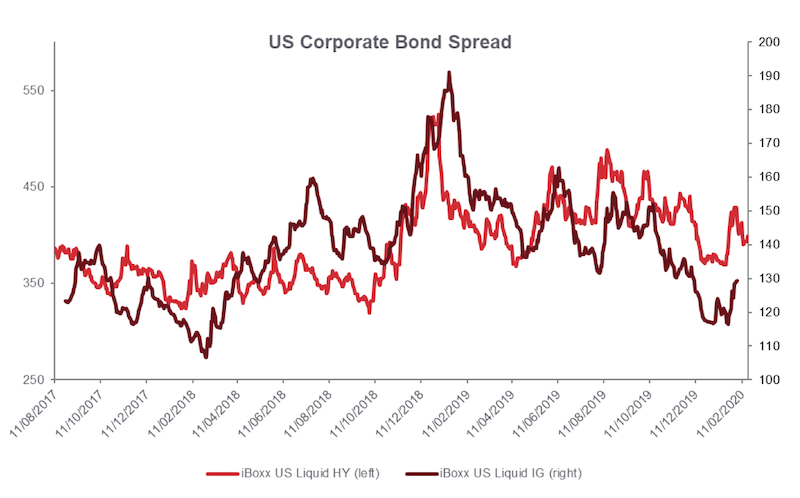

At the beginning of 2020, companies still had ample access to banking liquidity, but the resurgence of geopolitical tensions and contingencies such as coronavirus outbreak may put an end to narrow credit spreads.

The macroeconomic outlook based on a soft landing in Europe and the Federal Reserve taking action to support the US economy, encouraged companies to raise funds in 2019, in anticipation of external growth. Fast-growing SMEs in particular revisited their financing structures, resulting in transactions to support future growth and investments, which typically included setting up their first syndicated loans and diversifying their financing sources to the likes of bond debt and / or commercial paper.

But this situation has changed. Lenders have started to distinguish between investment-grade borrowers and high-yield firms, which are deemed to have a greater risk. Having emerged in the United States, this trend looks set to continue.

Banks and investors are focusing on their top-rated clients, which are therefore benefiting from a sort of flight to quality, while there is a more mixed attitude towards crossover or sub-investment-grade corporates. In fact, the terms and conditions offered to non-investment-grade borrowers has been seen to worsen in the most recent bank loan and private placement transactions.

In an environment in which credit committees have adopted a more cautious stance, corporate CFOs should ensure that they have an attractive story to tell and be able to demonstrate a good level of cash flow generation to service the debt and eventually repay it.

For companies falling short of these requirements, the concept of ample liquidity is just an illusion. The temptation to obtain more financing than necessary can lead to significant carrying costs. Credit committees and coverage teams are paying close attention to the size of existing facilities and are seeking to downsize them. There is still an appetite for high-rated corporates, but the size of financing must be consistent with the company’s business plan. This is a first step toward normalization of credit conditions.