Amid the chaos of COVID-19, layoffs, furloughs and businesses closing, there are still things businesses cannot avoid, like payment card brand fees, and the need to manage both the current fees and the constant changes put out by the card brands.

Payment card processing fees are the third largest expense that businesses have after rent and payroll, and Visa, Mastercard, and Discover historically make changes to their interchange fee schedules (the fees paid by merchants for processing credit and debit card transactions) twice a year in April and October. The plan was to increase fees in April of this year as well, but when COVID-19 happened, both Visa and Mastercard stated that they would postpone these changes until July 2020 in the hopes that the world will return to “normal.”

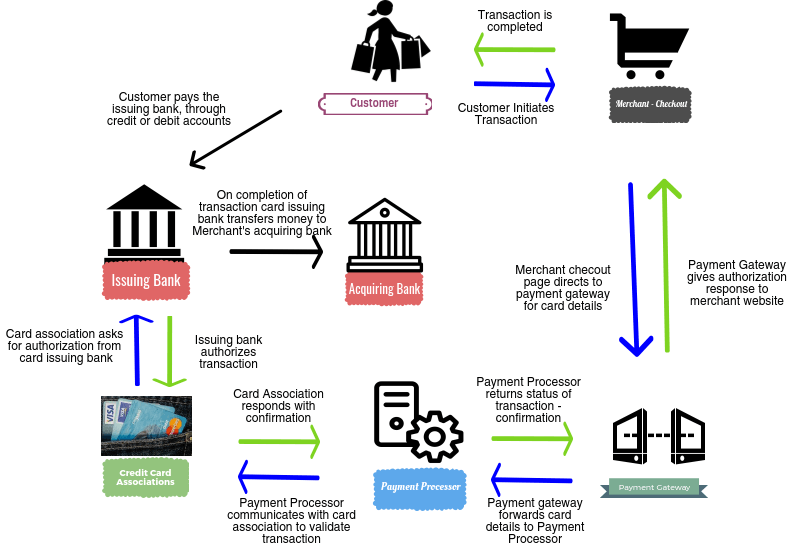

Complexity of the payment card industry

The payment card processing environment is confusing enough with only the regular card brand changes, but when you add in all the parties involved, it becomes exponentially more complex. For example, you have the acquirer/processor/bank, the gateway to get the transaction from the point-of-sale equipment that you use to process the transaction to your processor/acquirer/bank and potentially the middleware that provides the detail level information that determines how the transaction will clear with the card brands.

Visa, Mastercard, American Express and Discover have their own proprietary standards that determines how a transaction will clear their systems resulting in how much the business will pay for that particular transaction. Then there are the individual contracts with each party involved and the statements received each month that are multiple pages long, with line item details of each transaction that you processed for each customer, how the transaction cleared with the appropriate network, the interchange qualification levels and the type of cards that consumers and businesses use when paying. It is no wonder businesses are confused.

Below is a diagram of the potential parties involved in the transaction and remember, each of the parties have a fee that the business will be charged for their part in the process.

An action plan is necessary in order to take control of your payment card processing expenses

To manage cost effectively, it is vital that your business has visibility into the process:

- Review the pricing in your agreement from your card processor/acquirer/bank, your gateway, and any middleware you use.

- Make sure you receive detailed statements so you can see how the fees are charged and if they are in line with your agreements.

- Review your interchange fees, network fees, and assessment fees.

Reviewing this information monthly to make sure that the fees your acquirer, gateway, and middleware are charging the correct fees based on your contract and your card mix can help you control one of the largest expenses your business has.

HawkeyeCard, a software solution to monitor, manage and reduce card fees, is all about visibility into your payment card process and your fees, accessibility to be able see what is going on and negotiate your fees, and accountability to hold your processor/acquirer/bank/gateway/middleware accountable to the fees they quoted in the agreement and going forward. (For more information about HawkeyeCard, please contact Judy Desomma at jdesomma@redbridgedta.com.)

It is important to understand and manage these relationships and fees. If you are not sure where to start, contact us to start a conversation.