Banks invest to improve and digitalize both their internal processes and their customer offers. Even so, there are still huge differences among them, as all banks did not start this race at the same point and do not move at the same speed, write Samantha Felipe-Lopez and Wesley Johnson.

Looking at the banking and banking services industries, digital capabilities have now become a vital need for both individual consumers and for corporates. Having to now handle day-to-day business activities virtually, the need for banking’s digital transformation has become a necessity.

The digital transformation

With the recent increase of many companies adopting the latest digital trends, there has been a boom in the ecommerce space. Ecommerce has been on the rise over the last decade, but the pandemic has contributed even more to the success of online shopping with physical shops being forced to close indefinitely. Corporates without an online/ecommerce presence have rushed to join those who already invested in the infrastructure.

What exactly is digital banking?

Digital banking refers to the use of both online and/or mobile tools to access various financial services and activities that were historically only available through physical bank branches. Driven largely by individual consumers (mobile banking apps, personalized financial planning, contactless payments, voice banking or on-demand loans), banks have expanded their digital offering to corporates both large and small(cash flow forecast, working capital, artificial intelligence – AI). Even though the needs for consumers and corporations are not exactly the same, they both have one thing in common that is now the new normal for our society: the need for real time digital banking.

Contributing even more to the ongoing ecommerce boom, the acceptance of digital wallets by corporates and the use of digital wallets by consumers grew rapidly in 2020 where they were used in “44.5% of the e-commerce transaction volume, up 6.5% from 2019” according to FIS from their annual global payment report. Even though there has been a rise in the use of digital wallets, it does not mean every region is on the same level. Some regions clearly had a higher usage of digital wallets when compared to others. However, all regions have seen an overall increase in the usage of digital payments in general. As more and more consumers switch to different forms of digital banking, one payment method suffers greatly. In today’s digital age, consumers and corporates have accelerated their transition away from holding, accepting, and paying in physical cash.

According to FIS’ Global Payments report, cash sales at the POS fell from 32.1% in 2019 to 20.5% in 2020 and have no sign of gaining back any market share lost to the other digital payment methods.

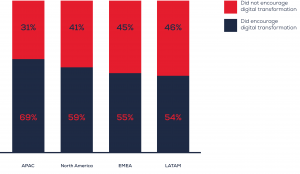

The treasury teams within most global corporations are no strangers to the digital transformation within their business function. However, the outside pressure of Covid-19 has expedited their need for innovation. (See graph below)

How has the pandemic impacted the digital transformation of your treasury

(Question asked to corporations with more than $2bn in revenues)

Source | JP Morgan

In this current environment, treasurers and their teams are focused on improving current processes around developing new key API’s, cash flow forecasting, and their liquidity and cash management. Identifying new data points and improving the teams overall data capabilities with more accurate forecasting, even with uncertainty ahead, is critical for the company’s survival. According to JPMorgan “40% of companies are exploring initiatives to enhance their data capabilities in treasury” A further one-third have already invested significantly in these” which is a clear indicator of what direction treasury is moving towards.

Where do banks stand in the race for digital?

Banks invest to improve and digitalize both their internal processes and their customer offers. Even so, there are still huge differences among them, as all banks did not start this race at the same point and do not move at the same speed.

Indeed, some of the oldest banks (especially the international ones) have a heavy legacy that might slow their evolution down and make it more difficult to innovate. Their 25-year-old banking platforms are not compatible with today’s varying needs. Sometimes, they even have to deal with layers of different platforms depending on the banks they have as acquirers over the past years.

What is a neobank?

A neobank is a bank fully digital, operating entirely online without a single physical branch.

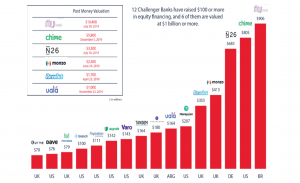

Banks are now facing the fierce competition of neobanks and fintechs, which are more flexible, agile, and innovative. Neobanks such as, Nubank, founded in 2013, in Sao Paulo, Brazil offer a more streamlined approach to banking. Claiming 3 million clients in 2018 and now up to 48 million clients as of September 2021, this neobank has been seeing tremendous success. They are planning to raise up to 3,000 million dollars (2,590 million euros) and reach a valuation of 50,000 million dollars after its introduction into Wall Street. Nubank will likely soon be more valuable than the main Brazilian bank iItau Unibanc. Yet, Nubank is not the only one seeing success, they are followed by Chime in the US, N26 in Germany, and many others.

It is no surprise as to why neobanks are so successful. These fintechs focus on client needs and are agile enough to adjust their solutions based on what people are looking for. Nubank has specifically targeted people that traditional banks have neglected for years, offering bank accounts and credit cards for free to the unbanked. This offer along with the sweet promise of a simplified service accessible on a smartphone has captured many new customers.

In the past, banks used to predominantly focus on being compliant with the many heavy regulations placed upon them, but today they have changed their strategy. In order to keep up with this fourth industrial revolution, they have become more client oriented and are embracing relevant digital trends (while continuing to comply with regulations; if we had to specify).

To keep up with the industry, some banks have chosen to collaborate with fintechs, while others have decided to internalize their developments and innovation strategy.

Generally speaking, small or local banks tend to build partnerships with fintech. For example, ING has recently concluded a partnership with the fintech Minna Technologies. The objective is to launch a new digital banking service: an online subscription to new services or products. ING’s customers will be able to directly manage their subscription in the banks digital channel without being redirected to another environment. Customers will have a clear view on all the services or products they have subscribed to and they will be able to cancel or upgrade them.

Other banks combine self-developed innovations and partnerships with fintechs such as the US bank JP Morgan: “We have an annual technology budget of $12 billion and in the last 18 months have added over a hundred new team members focused on treasury innovation, exposed dozens of treasury services APIs, engaged several hundred clients on corporate treasury innovation & co-creation, and engaged over a hundred FinTechs in this space.”

Navigating the digital banking landscape

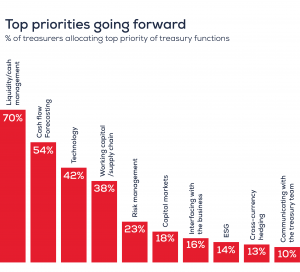

In recent years, we have seen a race for innovation in which companies seek to be the first in launching a new product or service that will address a customer’s (new or growing) needs. For example, since the Covid crisis, the need to improve cash forecasting processes and the desire for more accuracy are more important than ever (as we can see in the graphics below).

With innovation in mind, banks will try to address the needs of their clients, whether they are large corporates or everyday consumers. Their goal will focus on becoming the first player in that market and if they are not able to achieve this, then they will try to differentiate their solutions above the others. Nevertheless, all of these services are relatively new and we cannot truly determine their effectiveness or efficiency for the future.

Source | EF-Treasury report

The main risk corporates will face, and are currently facing, is the uncertainty of investing in a service and its infrastructure that may not fully answer their needs. Now more than ever, consumers face increased risk, such as fraud, due to the rise of digital banking. Consumers are not alone in their concerns, as fraud prevention and management is always a large topic for corporates. That is why it is very important to always spend time in assessing your core needs and doing an RFP to assess the quality of the offer. Regardless of if you are just a consumer or a large corporate, due diligence should always be done when it comes to decisions around banking digitally.

Read our new special report on the cash management & payment trends that will transform your treasury department in 2022

The growth and vitality of the payments industry has fascinated all observers during the past two years of the pandemic. Now with recent geopolitical developments arising from the Russia-Ukraine conflict, it is being tested again.

Our new publication analyzes the most prevalent trends and innovations in the treasury world today.

Included in this publication:

- The Global Resurgence of QR Codes

- Choosing the Right Payment Terminal in an Ever-Changing Environment

- The Rise of Buy Now, Pay Later

- PCI Compliance in an E-Commerce World

- Where Do Banks Stand in the Race for Digital?

- Virtual Accounts, Which Companies Should Implement Them?

- The Future & Alternatives to SWIFT GPI

- Global Digitization in the Depository Space

- “Switching Banks Was the Right Decision”: An Interview with Olivier Bouillaud from Albéa

Download the full publication