When we think about how bank fees are being treated in the U.S., there is something very unique that, regardless of your company’s size, industry or banking partners, if you operate in this country, your bank fees will inevitably be tied to your operating balances through an earnings credit rate (ECR) mechanism.

You have probably been told that, for better or for worse, the fate of your ECR depends solely on the evolution of the fed funds rate. But is it really so? And does it mean that with the current downward rate environment, your only option would be to gracefully accept that your ECR will go down? Before we address this, let’s take a look at the past and understand how we ended up asking ourselves these questions.

When it comes to the fed funds rate evolution, you can essentially divide the last decade into two major eras.

First era: 2009-2015

From 2009 to 2015, the fed funds rate was steadily and consistently nearing zero after a huge collapse throughout the prior years. During this first era, companies started to diversify their investment and sought alternative options to generate better yield on their operating balances. Because the rates were so low for so long, everybody forgot about ECRs and adjusted to the new reality of paying gross bank fees.

Second era: 2015 to present

Late in 2015, the wind began to change, and the fed funds rate finally came out of hibernation and started rising again. The upward trend was steep and steady, and by early 2019, the fed funds rate peaked at 2.5%. The rest of the year has been a little rocky, as we are now experiencing a downward trend again.

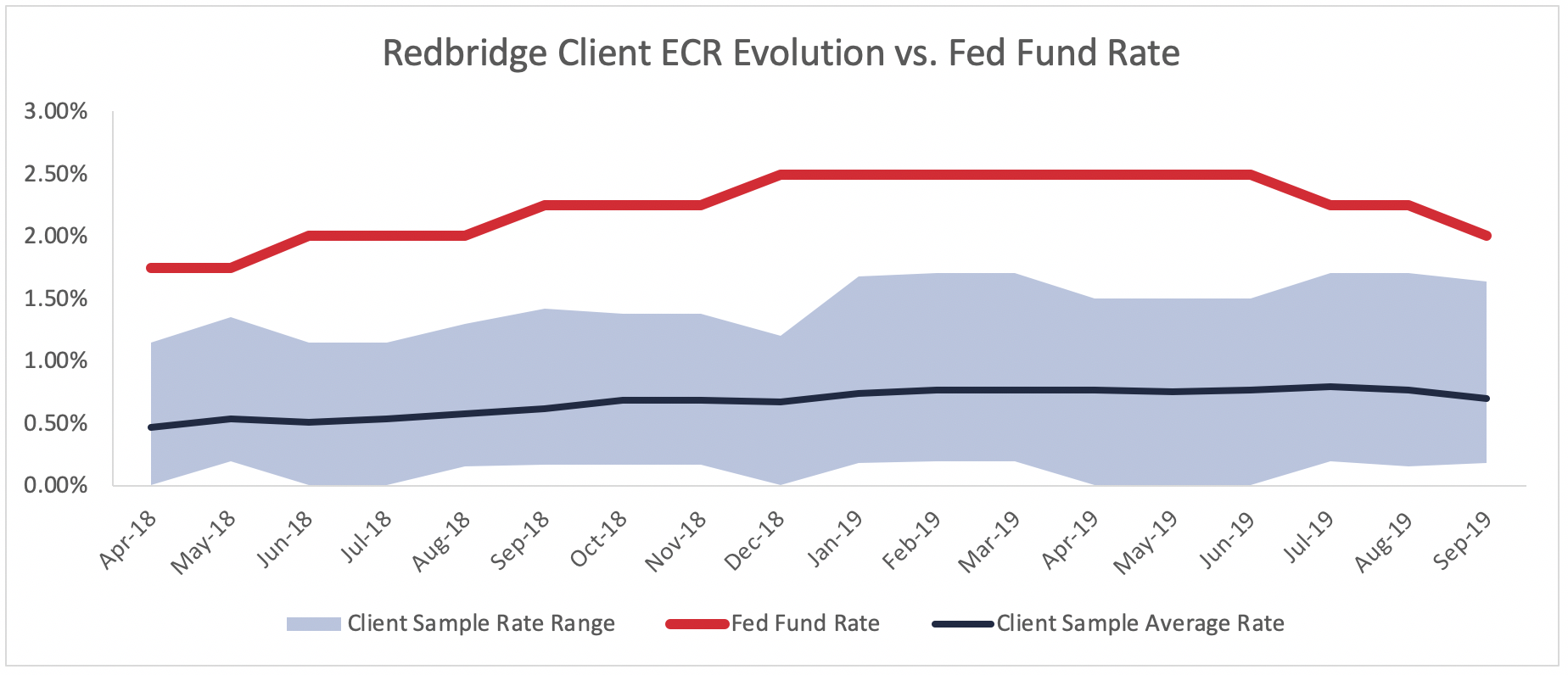

Redbridge clients’ ECR vs. the fed funds rate

We looked at data from the last 18 months, where we actually experienced the rates rising, peaking, and decreasing, and analyzed a panel of Redbridge clients. What we found contradicted two of the most widespread assumptions in the industry: ECR and fed funds rate are strictly tied together, and there is almost no room for negotiation in this downward rate environment.

We randomly selected 27 large corporations within the same range of balances to provide a representative panel of companies in every industry and vertical.

The first observation from our study is how wide the range of ECR is among the sample. Over the 18-month period, the average spread between the lowest ECR and the highest ECR of the panel was 123 basis points (bps).

But certainly, the most important observation is the difference between the evolution of the fed funds rate and the evolution of the average ECR in our sample. Although both rates tend to follow the same upward or downward pattern, there is no absolute correlation between the two rates. And the truth is the fed funds rate has been rising at a faster pace, when the average ECR has been struggling to catch up, especially during periods of frequent fed funds rate increases.

From May to December 2018, the fed funds rate increased five times, but the spread between the average ECR went from 122 bps to a record 183 bps. Only after the fed funds rate started to plateau in the first semester of 2019 did the spread start to very slowly and marginally close. But even after two decreases in rates in the second semester, the spread between ECR and fed funds rate still hasn’t come down to the lowest point of 122 bps that we observed in May 2018.

Monitor your ECR

So, I think you all know what I am getting at: even though the rates are going down, there is still ample room for negotiating your ECR to not only catch up with the Fed, but significantly and sustainably reduce the gap. The average spread between ECR and fed funds rate among our sample over the 18-month period was 156 bps. I would argue that after the next Fed meeting on December 10, 2019, even if the rate decreases again, there would still be room to negotiate.

Reactivity and consistency are critical factors for success. If you are a large corporation paying significant bank fees and keeping a substantial balance, dropping the ball on your ECR for only a couple of months could cost your organization millions.