With such a fast-paced and everchanging payment ecosystem, there are no providers that can cover everything a merchant may need. So, how can merchants turn this challenge into a competitive advantage? It all starts with understanding and leveraging payment architecture.

What is payment architecture?

Payment architecture is the carefully designed structure allowing a merchant to accept payments from anyone who is willing to pay or has previously agreed to be debited.

For each merchant, payment architecture may differ slightly depending on their overall goals and what systems are currently available to them. Looking at the payment value chain can give merchants a better idea of what they should be looking for based on their needs in each step of the payment process . The payment value chain is a series of steps that outline the entire payment process from beginning to end. It takes into account both “card present” and “card not present” transactions.

The Payment Value Chain

Today’s payment ecosystem is very fast-paced and operates in an environment where many different types of payment methods coexist. Some of them with international reach (e.g., Visa, Mastercard, American Express, UnionPay…), and others with a very local approach (e.g., iDeal in the Netherlands).

At the same time, payment providers face extensive regulatory requirements and ongoing evolution, which makes it extremely difficult for them to have global reach and accept all available payments methods at an optimized cost. Therefore, there is currently no single provider that can cover all merchants’ needs in every country or region at the most competitive price.

As a result, merchants must decide whether to pick specialized providers or go with one that offers full-service, then fill the gaps with complementary solutions. As usual when talking about technology, each approach has its pros and cons:

Specialized providers

Pros

- More flexibility

- Better performance

- (Sometimes) lower pricing per unit

Cons

- Complex integration and maintenance

- Multiple contracts, reporting, invoices, and relationships to manage

Full-service providers

Pros

- Simplified technical aspects

- Easier to manage

Cons

- Overall, more limited

- Increased risk of vendor lock-in

The key takeaway is that there is no “one size fits all” solution when it comes to payment system design. Rather, there is a myriad of providers that each merchant needs to carefully consider based on their needs.

Why is payment architecture important for merchants?

Deciding on the best payment processing architecture for a given merchant is particularly complex. This is because many different things need to be taken into account including, technological, business, finance, and compliance related implications.

When looking at a business’s top priorities related to payment architecture, there is always a push to have the most relevant payment methods with frictionless user experience. This is the case no matter how risky, complex, or costly these solutions can be.

From a compliance and risk point of view, accepting and collecting payments must be a bulletproof process. Meaning any associated risks need to be identified, properly mitigated, and controlled. One of the important security details to look for is PCI-DSS (Payment Card Industry Data Security Standard). As non-compliance may end up with the unilateral termination of the acquiring contract by the acquirer. Payment related fraud is also another big piece when it comes to payment risks.

When looking at how payments work from a system and process standpoint, the workload must be as low as possible to maximize efficiency. Lowering the workload can be done by relying on pre-built integrations or task automations offered by provider(s). For example, if a provider has a pre-built integration with an ERP or ecommerce platform already used by the merchant, the implementation will go much faster. Once a provider is selected, putting enough effort into the payment integration design will drastically reduce delays in the implementation process.

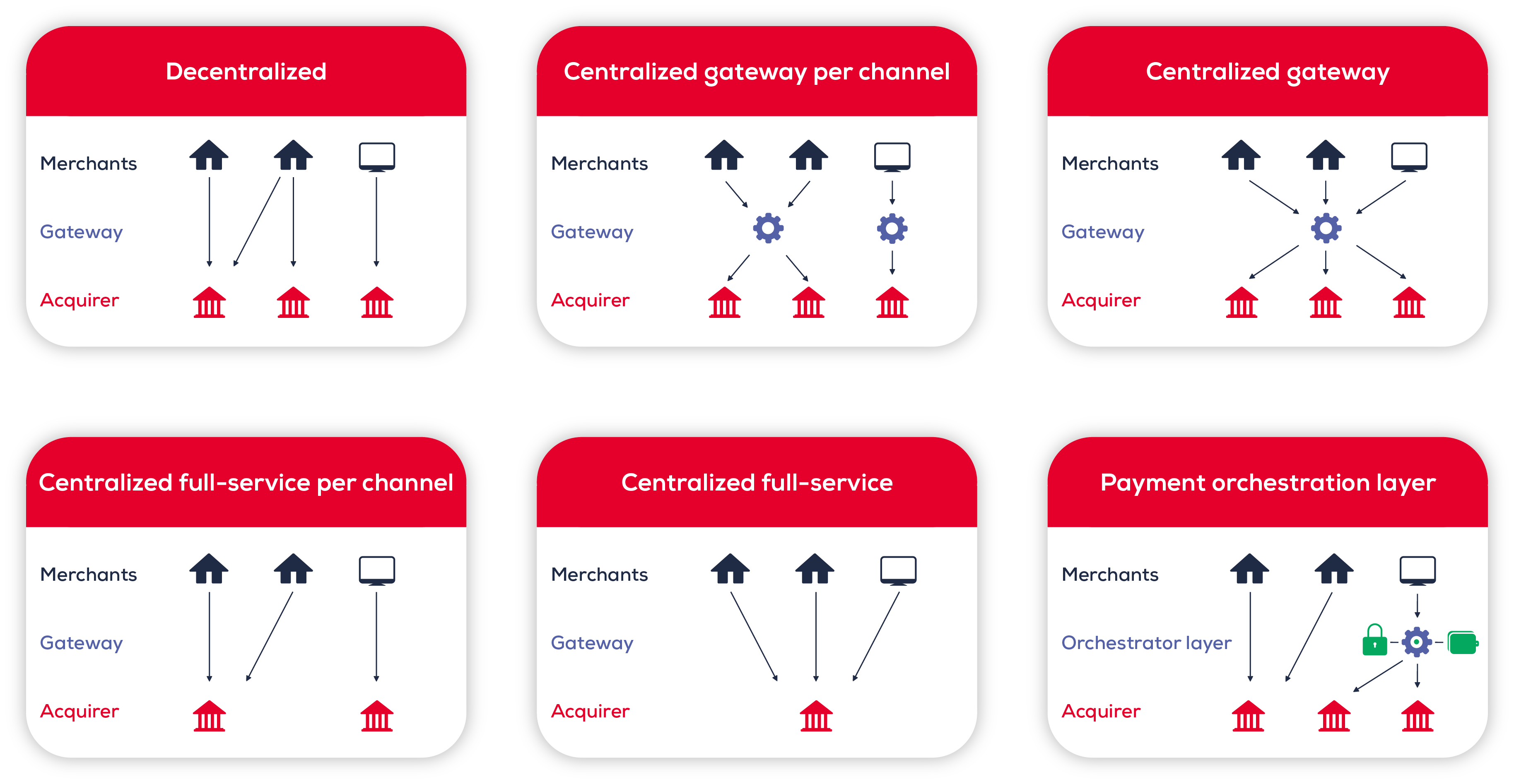

Different types of payment architecture

The best way for merchants to set up an efficient payment architecture

Setting up an efficient payment architecture starts with clearly identifying the merchant’s requirements and making sure nothing important is overlooked. An effective approach to this would be to tackle the main topics one by one and then weight and prioritize each to establish a consensus across different departments.

This 360º approach should include the following topics:

- Acceptance & customer experience

- Security, fraud management & compliance

- Technical architecture & internal organization

- Cost analysis and potential optimizations

- Provider’s relationship and selection

Once a list of requirements and their level of importance is defined, the exploration of possibilities and further assessment can start. Some of the main considerations a merchant will typically need to think about when defining the target payment system architecture are the following (list non exhaustive):

Multichannel vs omnichannel

When merchants have multiple sales channels, combining all of them in order to create an omnichannel experience may be a key objective. Combining them will determine if there is still a need to rely on omnichannel providers or if the setup can be done internally. Building it internally will allow for more flexibility but, require a more complex implementation (including how to remain PCI-DSS compliant).

One main payment provider vs multiple providers

There are any many pros to using one provider, such as aggregating volumes for better pricing or being able to simplify implementation and management. On the other hand, having distributed systems architecture also presents many benefits. These include flexibility to select providers better suited for the job or that are the least costly. A distributed architecture also helps reduce the risk associated with a provider going down, as the traffic can always be routed to another provider.

Full acquiring service vs payment gateway + local and / or international acquirers (banking or non-banking acquirers)

Full-service providers usually have a wide offering of payment methods and a centralized platform because their acquiring rails are either in-house or they rely on their own acquiring partners. However, this setup can significantly limit the options to optimize costs. On the other hand, a gateway + acquirers’ setup usually offers less payment methods and is more complex to implement/maintain, but let’s merchants negotiate and pick acquirers for fully optimized costs.

Terminal management

Traditionally, terminals were purchased directly by constructors, but now it is a common practice for terminals to either be rented or sold by payment providers with maintenance fees. However, because of this vertical integration, some payment providers limit terminal usage to their own acquiring services. Doing so increases the risk of vendor lock-in and limits the options for a merchant to optimize costs on specific payment methods. Methods such as American Express or services such as Dynamic Currency Conversion (DCC) can usually be optimized significantly when working with a direct connection or a specialized provider.

Payment orchestration layers

This payment platform has been a hot trend for a few years, and it’s currently only available on Card Not Present (CNP) transactions – Mail Order, Telephone Order (MOTO) and online transactions. It has a multi payment provider strategy while simplifying a lot of the technical implementation and maintenance. In fact, a payment orchestration layer becomes the single technical point of contact for a merchant, while offering connections to (almost) any payment gateway, payment processors / acquirer and other third parties like 3DS or fraud management providers. Therefore, an orchestration layer can facilitate the way merchants secure transactions while maximizing conversion by proposing a better payment experience.

Specialists

Depending on a merchant’s business and needs, it can also be worth looking into specialists for specific services or geographies. Specialists may offer a better level of service and/or better pricing conditions:

- payment service providers specialized on local and alternative payment methods

- token management

- fraud and/or chargebacks management

- dynamic currency conversion (DCC), VAT refund, maintainers