Redbridge’s annual study of corporate debt structure reveals that the credit profile of France’s leading listed companies has moved from “A” to “BBB” over the past 18 months. Tensions in negotiations with banks and private bond holders are prompting finance departments to prepare for a more stressful environment.

The introduction of IFRS 16 and the COVID-19 crisis have changed the debt profile of listed French companies

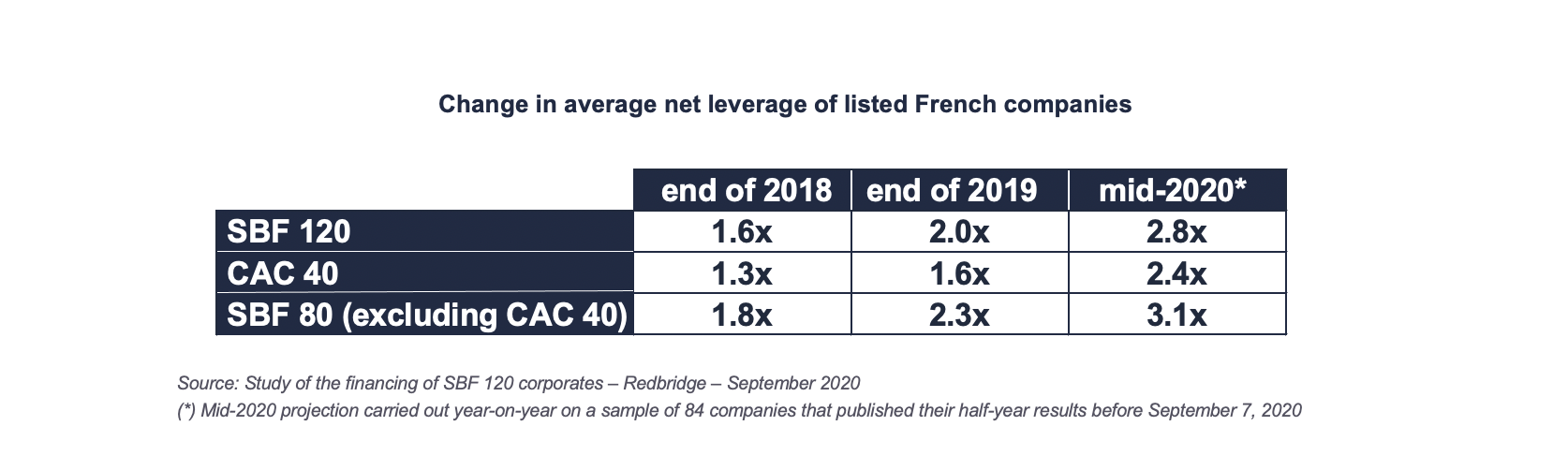

- The average credit profile of listed French companies, as illustrated by their nominal net debt/EBITDA ratios, fell from category A to category BBB in just 18 months.

- The average amount of leverage at the end of 2019, after the introduction of IFRS 16 on leases but before the COVID crisis, was at its highest level in the past ten years (2.0x versus 1.7x at the end of 2012).

- In 2019, credit ratios fell due to the introduction of IFRS 16, with net leverage falling by an average of 0.3x.

- The acceleration in the decline of corporate credit profiles over the first half of 2020 and the ongoing uncertainty about economic prospects are changing the relationship between companies and their lenders.

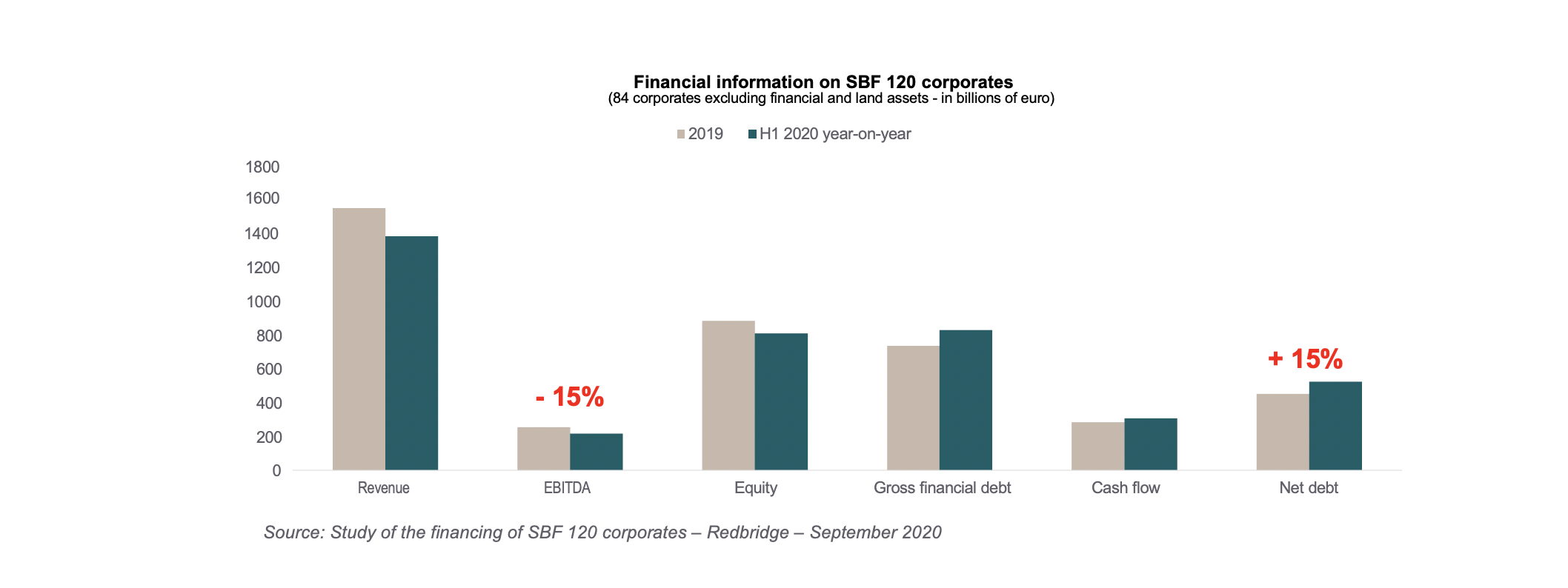

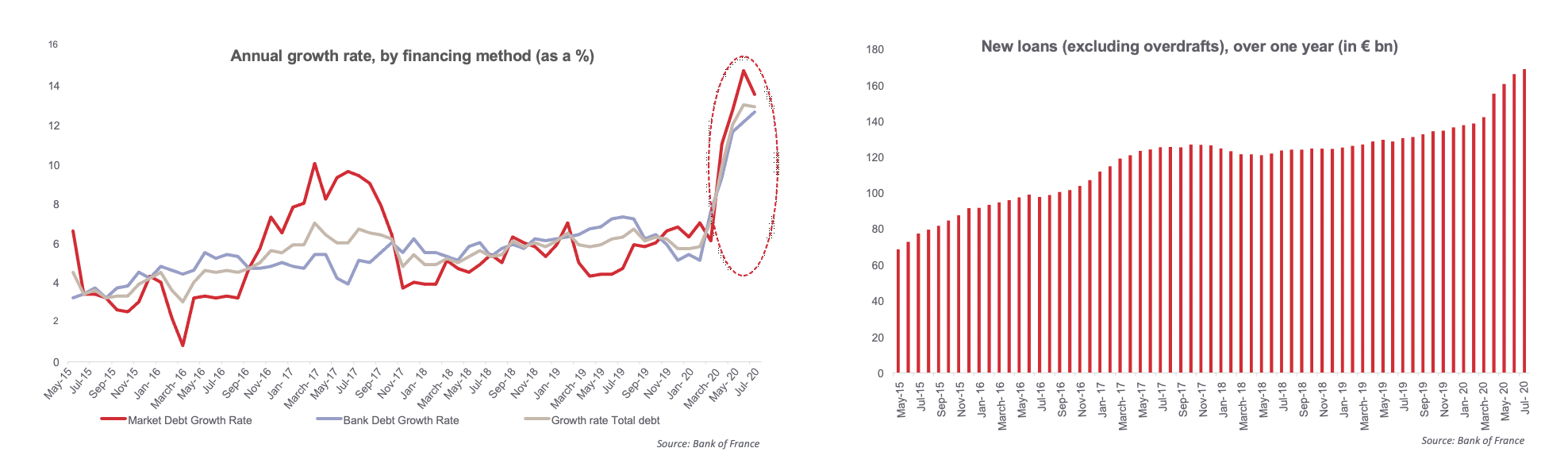

In the first half of 2020, the gross debt of listed French corporates jumped by 13%

Main financial metrics of non-financial SBF 120 companies as of the end of June 2020*

- When focusing on a sample of 84 corporates that published their half-year results before 7 September 2020, the drop in revenue at the end of June was 10.7% year-on-year.

- EBITDA also fell sharply: by 15%.

- The gross debt of the 84 companies increased by EUR 94 billion to EUR 829 billion (+12.7%) during the first half of 2020.

- Cash flow increased from EUR 283 billion at the end of 2019 to EUR 306 billion (+8.1%). This represents 37% of gross debt.

- Net debt increased by EUR 71 billion to EUR 523 billion (+15.6%).

(*) Analysis carried out on a panel of 84 corporates. The impacts

of IFRS 16 are taken into account for the years 2019 and 2020.

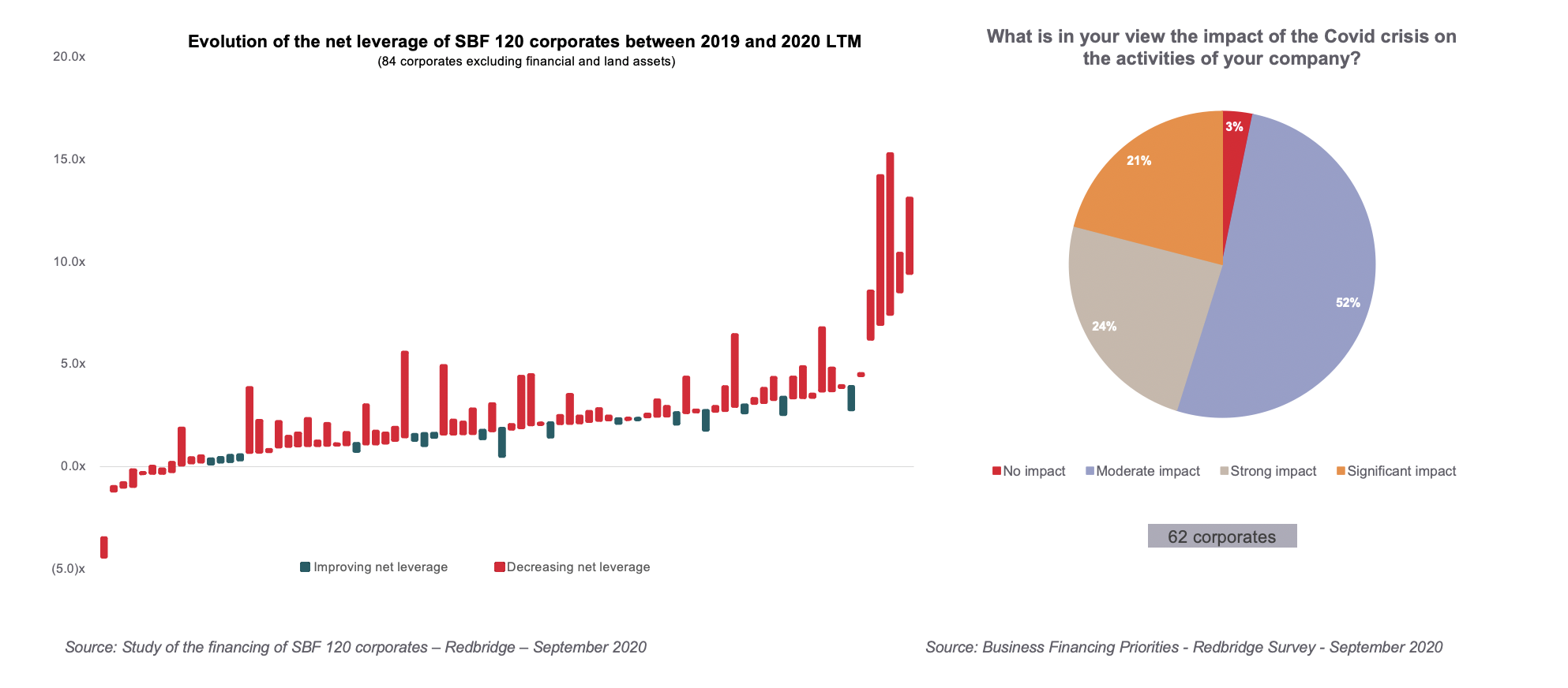

Corporate performance diverged significantly in the first half of the year, which is suggestive of a K-shaped economic recovery

- While there was a sharp increase in the average leverage of listed French companies in the first half of the year, three large groups of companies stand out in terms of the impact of the pandemic on business activity (see below).

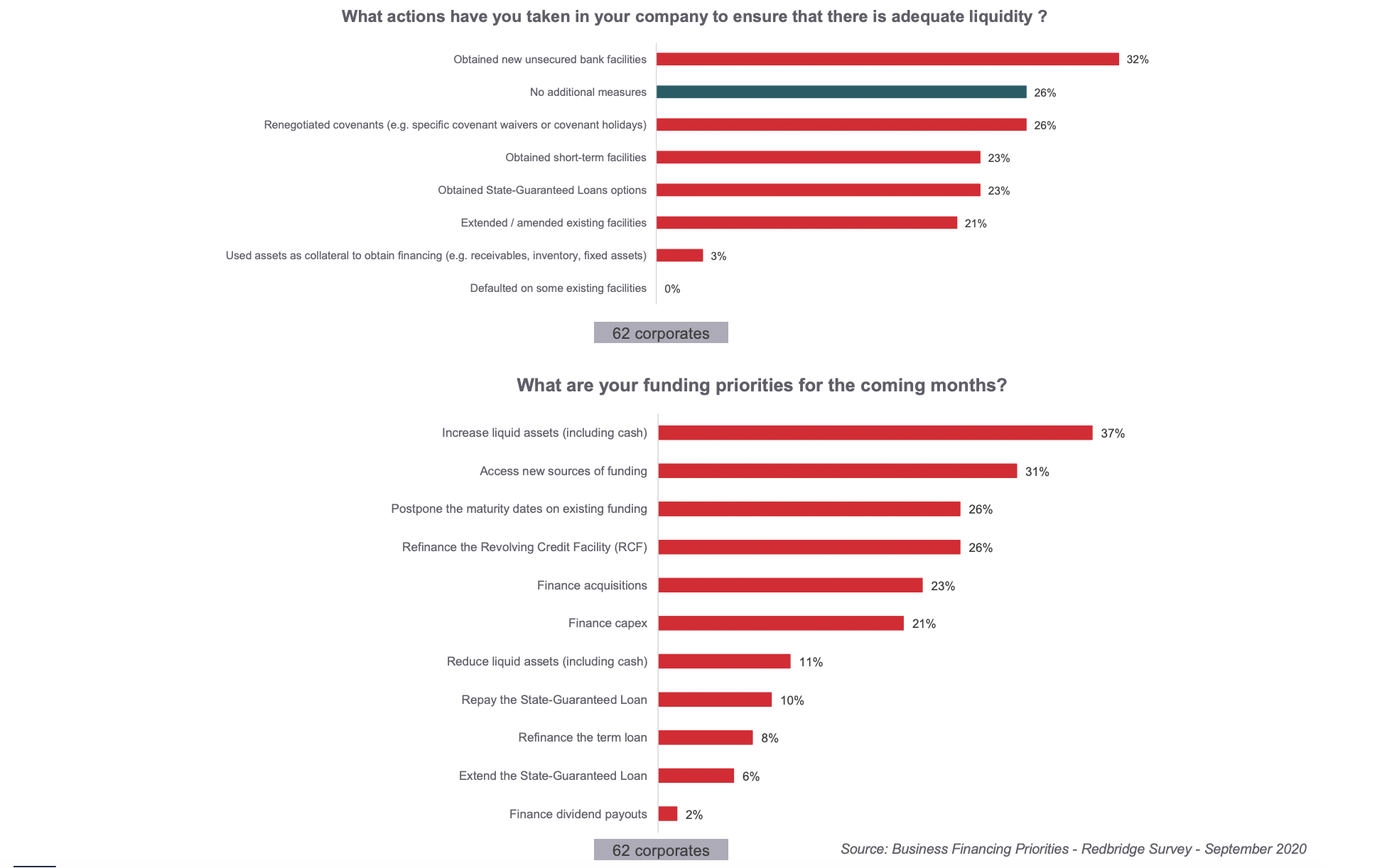

The main priority for companies is strengthening liquidity

- 23% of the companies we surveyed have set up a state-guaranteed loan.

- Just over a quarter of respondents (26%) have renegotiated their covenants.

- 26% of companies have not adopted any measures in addition to their initial financing strategy.

- Accessing new sources of financing is the priority for almost a third (31%) of respondents.

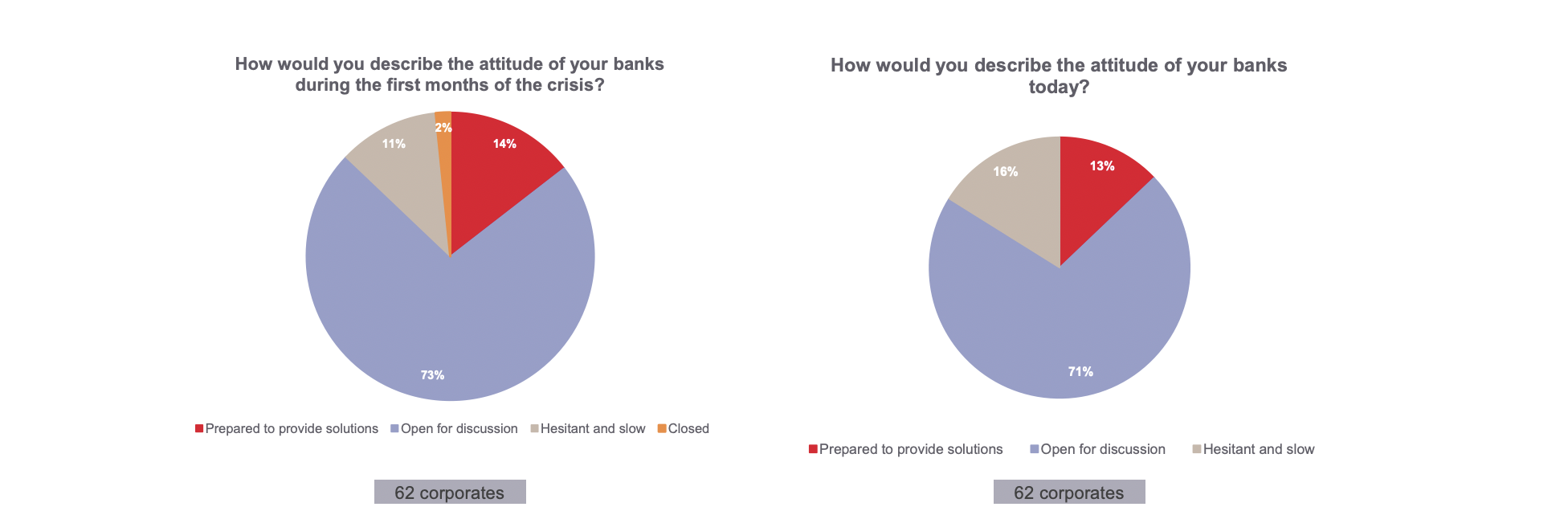

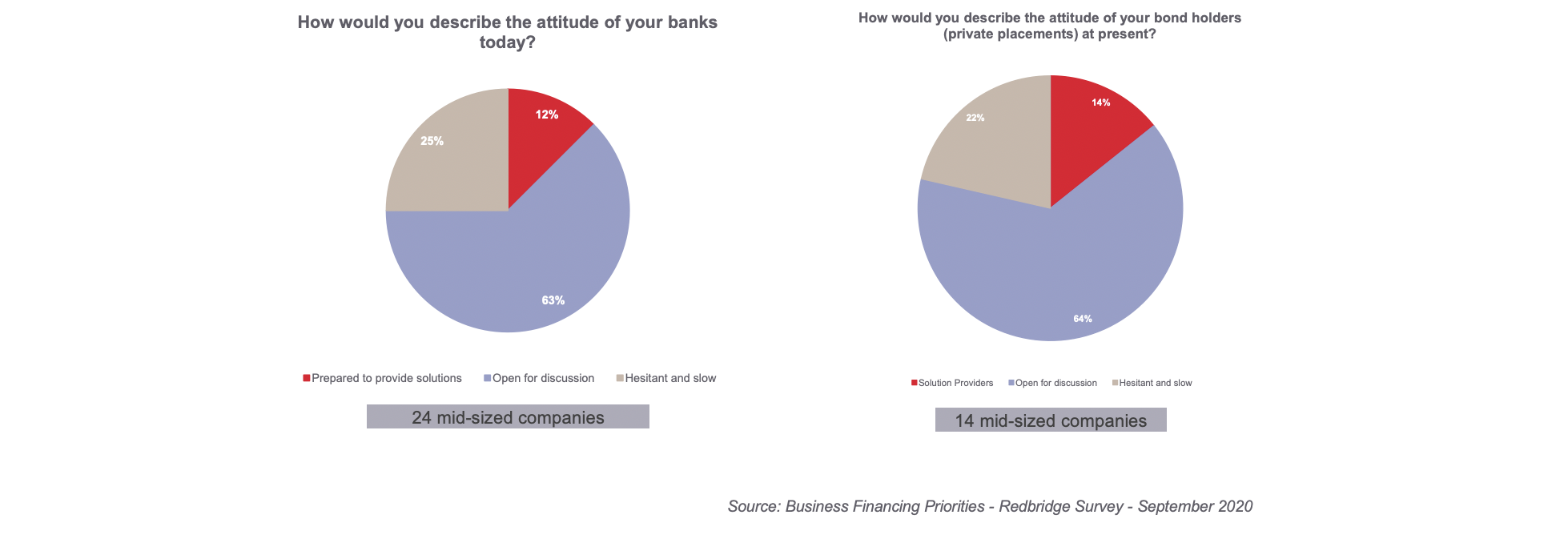

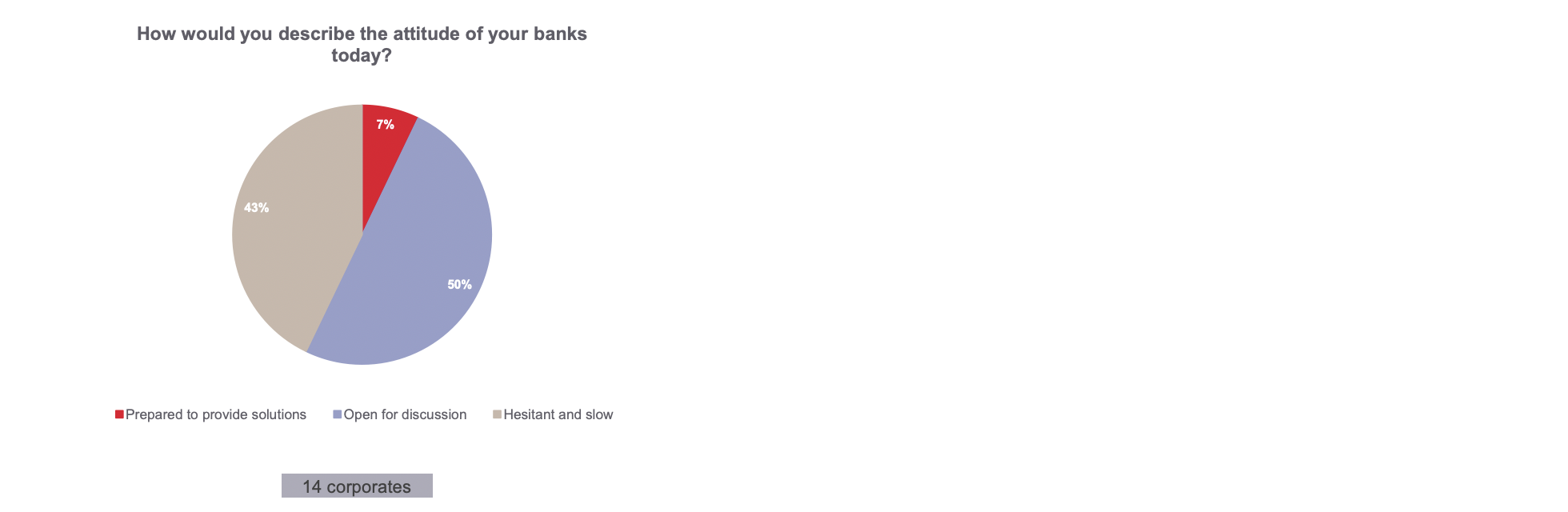

According to corporates, banking relations remain good

- 71% of respondents felt that banks are open to discussion about new funding.

- However, 25% of the mid-size companies surveyed believe that their banks are currently stepping back.

- Likewise, just over a quarter (27%) of the mid-size companies surveyed believe their relationships with bond holders are under strain.

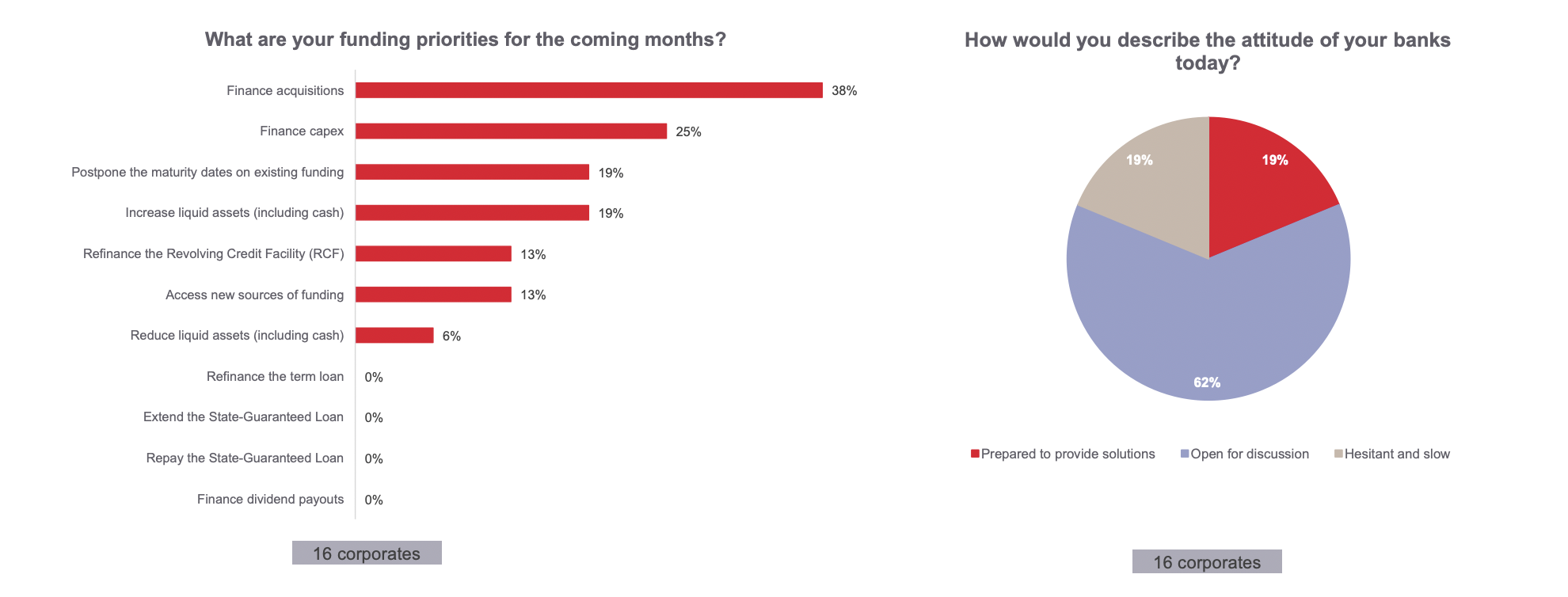

For corporates with a solid financing structure, access to financing for growth remains the top priority

Circumstances of respondents who have not adopted measures in addition to their initial financing structure

- The main priorities for companies that have not taken any additional post-crisis measures are to ensure they have access to finance in order to fund acquisitions (38%) and capex (25%).

- It is interesting to note that 19% of respondents who have not taken any measures in addition to their initial strategy believe that their banking relations are under strain at the moment.

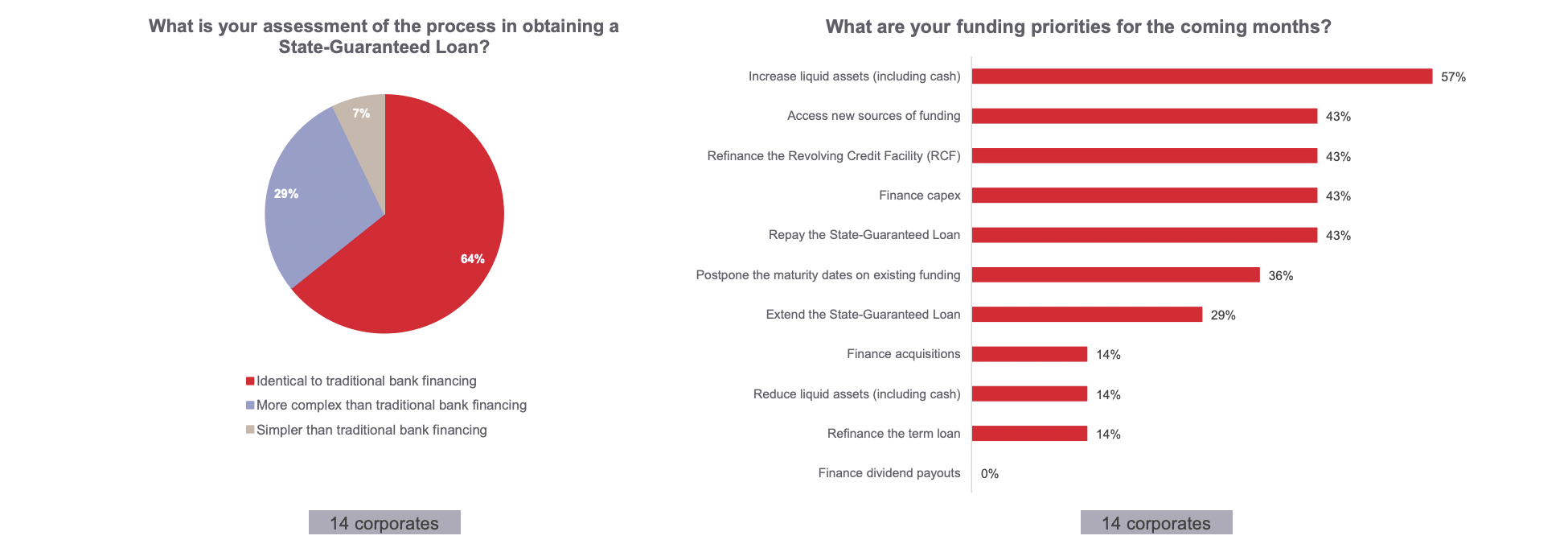

At least 43% of respondents who have benefited from a state-guaranteed loan wish to repay it in the short term

Circumstances of respondents who have set up a state-guaranteed loan and/or other forms of finance subject to a guarantee by the state

- 29% of corporates who have opted for a state-guaranteed loan consider it harder to set up than traditional bank financing.

- 43% of respondents receiving state-guaranteed loans believe that their banking relations are currently strained.

- About 30% of respondents wish to extend their state-guaranteed loan.

- A quarter of state-guaranteed loan borrowers are yet to decide wether they will repay or extend their financing.

Central banks and governments will continue to play a key role in stabilizing bank credit markets

Banking market

- The sharp increase in the indebtedness of SBF 120 companies reflects that the health crisis has not resulted in a credit crunch.

- State-guaranteed loans

- Additional one- or two-year crisis liquidity lines

- Waivers / covenant holidays

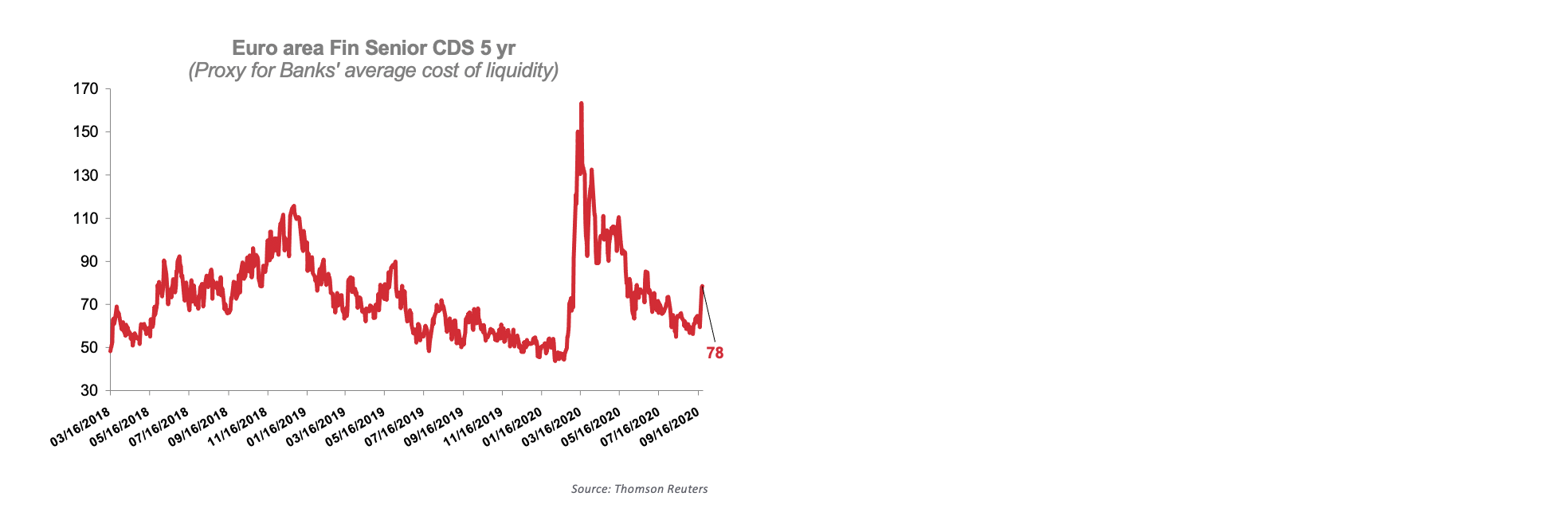

- Even though cash flow support operations between March and this summer took place without undue strain on banks, fall was marked by a clear repricing of spreads, which could reach 50bps, particularly for the most highly “leveraged” companies.

- Despite the massive liquidity injections, the cost of refinancing banks has stabilized at around 15bps above its average pre-crisis level after soaring in March/April, while the cost of risk is skyrocketing.

- The sharp rise in deposits has also facilitated the development of credit.

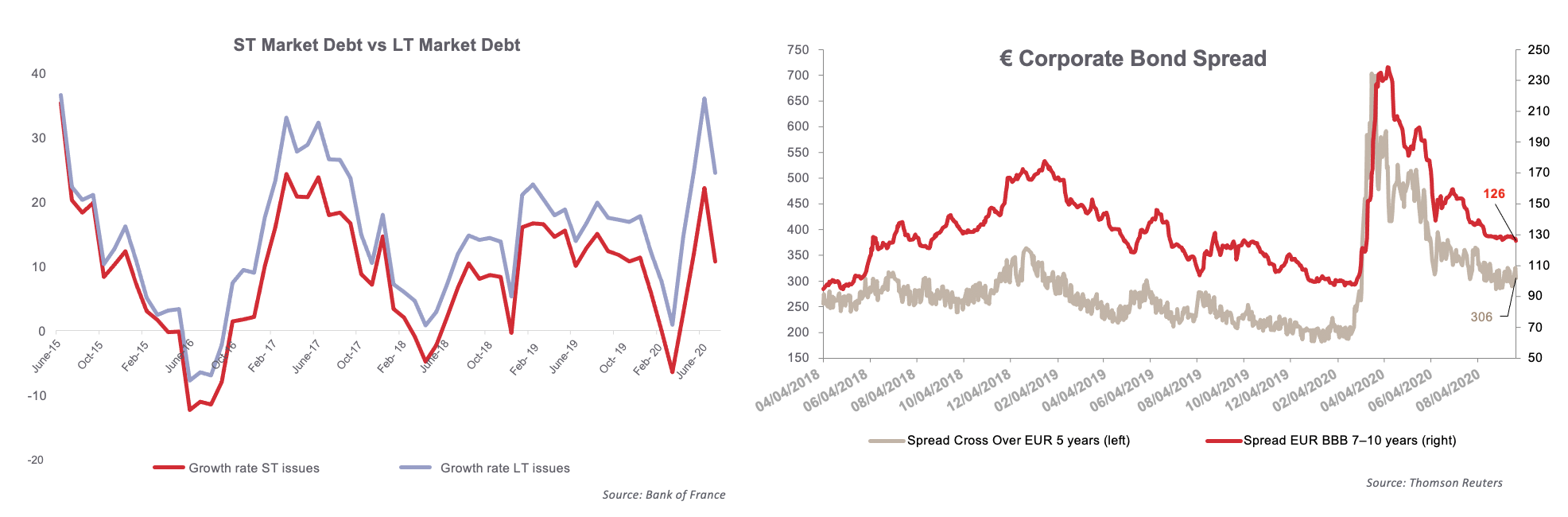

Corporates have issued bond debt on a massive scale against a backdrop in which the over-supply of liquidity has led to risk premiums contracting

Bond market

- In addition to the banking market, companies have relied heavily on the bond markets to secure liquidity cushions.

- It has been another record year for the primary market (following on from 2019, which was in itself a record year). There has been EUR 380 billion of corporate issuance so far this year, around 20% above the 2019 level.

- There has been considerable investor appetite for these issues in the form of high oversubscription rates and low new issue premiums (NIPs).

- Despite the macroeconomic uncertainties, central bank policy should remain accommodative, stimulating the bond markets.

- How well will central banks support the financial markets against a backdrop of an overall increase in risks at the end of the year?

Some final thoughts

- The supply/demand balance in bank credit is changing, and it is becoming more expensive.

- For the most complicated credit profiles, the documentary framework is becoming stricter.

- When it comes to disintermediated debt, the private investments sector is not as attractive as public markets.

- The most fragile companies (those in complicated industries, with high leverage and liquidity problems) are being affected the most, but even investment-grade lines of credit are suffering from the uncertain macroeconomic outlook.

- State-guaranteed loan arbitration / other source of financing: companies that have benefited from a state-guaranteed loan should take into account the increasing cost of credit in their decision-making process when considering repaying the loan.

- Companies should not underestimate the flexibility provided by WCR solutions.

- In this particularly complicated environment, the advice we gave at the start of the crisis still stands: communicate openly about credit profiles, based on reliable and detailed information (in particular, cash flow projections in the event of a second wave of the virus); secure liquidity and extend maturities.