Lucie Kunesova, Associate Director – Cash Management Advisory at Redbridge, shares her practical approach to renegotiating bank fees and services, drawing on concrete examples from recent engagements with treasury teams at groups in the insurance, construction, and real estate sectors. Her key words: analysis, benchmarking, and a holistic approach.

Tracking and negotiating bank fees – an often underestimated challenge.

Why are cash-management fees rarely examined closely by companies?

— Lucie Kunešová: Senior management often treats cash-management fees as a secondary matter within the wider bank–corporate relationship. For treasurers, monitoring and negotiating these fees is a demanding task. Billing is rarely transparent: fee statements are dense, full of opaque terminology, and difficult to interpret, which complicates accurate tracking and analysis. Many treasurers also admit they lack the benchmarks and tools needed to assess these costs in detail. Without reliable, comprehensive external price data, discussions around cash-management fees tend to remain vague. As a result, companies often accept fee levels that are significantly higher than necessary.

Another factor is the underlying fear of damaging banking relationships by pushing too hard on costs. Yet, with the right approach, it is entirely possible to achieve far more favorable terms while maintaining—or even enhancing—the balance of the relationship.

What are the key steps in a successful renegotiation of bank fees?

— The first step is to gather and centralize all bank fee statements so the data can be properly analyzed. At Redbridge, we begin with a detailed review to map services and volumes precisely. This diagnostic work uncovers inconsistencies, eliminates superfluous charges, and refocuses spending on services that the treasury genuinely needs. Painstaking, yes—but essential.

Once you have this clear view of the pricing applied by your cash-management banks, you can assess the competitiveness of each service. Redbridge has built a proprietary global database over more than 25 years of work with European and US corporates. Leveraging this database with our technology, we benchmark every service item to quantify potential savings.

Finally, equipped with these insights, we conduct a structured negotiation with banks—through an RFP process or bilateral discussions—while ensuring the dialogue remains balanced and constructive. This three-step approach—quantify, benchmark, negotiate—turns fees once thought immovable into an opportunity for lasting optimization.

Leave No Lever Unexplored! – FX Costs, Excess Cash, and a Global View.

Beyond cash management fees as such, what other options should treasurers explore to maximize gains?

— Do not limit your review to the cash-management fee schedule. Other savings pools are within reach—starting with foreign exchange (FX). In particular, the FX margins applied by banks constitute a material cost for companies with substantial international activity. We frequently observe wide margin differentials from one bank to another. By dissecting the components of these margins and benchmarking them against the market, a significant optimization potential often emerges. A structured renegotiation of FX terms can deliver far more competitive exchange rates—without changing platforms or disrupting day-to-day operations.

Continue reading – When segregated accounts unlock hidden savings

Another optimization lever: deposit yields. With interest rates back to normal levels, this topic has returned to center stage. During the years of negative rates, many treasury teams left liquidity idle in non-remunerated current accounts because the stakes seemed minor—some even paid to hold excess cash. Today, with positive rates, leaving surplus balances idle creates a real opportunity cost. There is clear value in enhancing these balances: negotiating deposit yields with your banks, or setting up short-term investments that respect security and liquidity constraints.

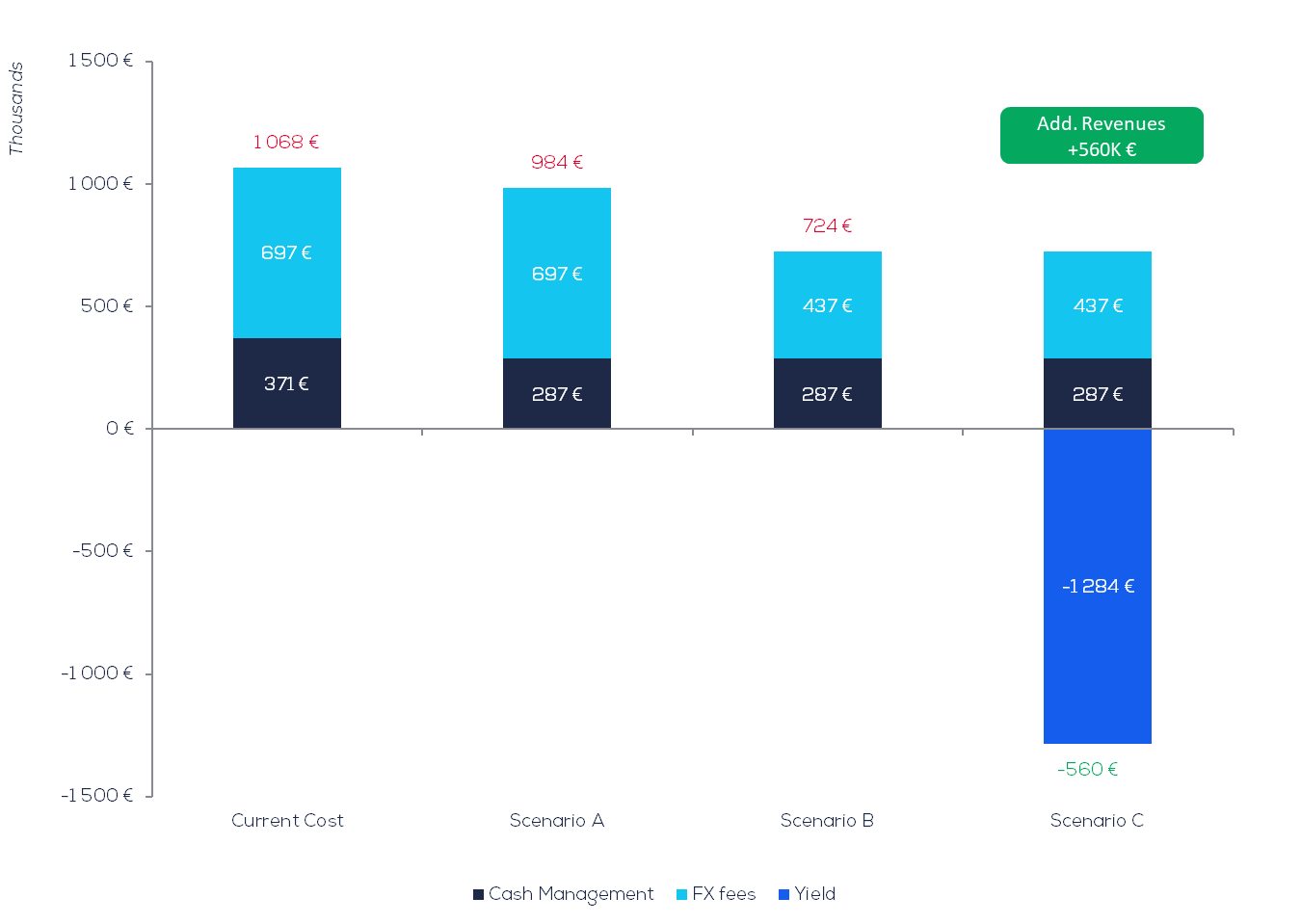

The winning approach is holistic. Instead of treating each topic in a silo—transaction fees here, FX there, and excess cash elsewhere—consider them together. These levers reinforce one another. In a recent engagement, renegotiating the cash-management fee schedule alone already delivered strong savings potential. Adding FX costs and deposit yields quintupled the overall upside. For an insurance client, we modeled three scenarios: (A) renegotiate cash-management fees only; (B) add FX cost optimization; and (C) also negotiate deposit yields. Each path produced meaningful gains, but the integrated approach maximized value. Ultimately, this large insurance group—paying EUR 1.07 million annually in cash-management fees across five countries—saw that cost line turn into a net income of EUR 0.56 million, all while respecting its banking-relationship strategy.

Figure — Example of a holistic renegotiation of cash management fees / Sector: Insurance

Scenario A: Cash Management Fees renegotiation

Scenario B: Integration of FX issues

Scenario C: Holistic approach including yields on deposits

Source: Redbridge – Cash Management Advisory, September 2025

To continue – read our next article

When segregated accounts unlock hidden savings

In the insurance, construction, and real-estate sectors, the treasurer’s role comes with distinct constraints that make optimizing cash-management services and fees more intricate. For Lucie Kunešová, Associate Director – Cash Management Advisory at Redbridge, these specifics are not a handicap but, on the contrary, a signal of greater savings potential in cash management. Proof by example.