The card brands – Visa, MasterCard, Discover and American Express – make changes to their interchange rates and fees twice a year, usually in April and October, and are generally non-negotiable. This article highlights the major changes introduced in April 2022. Unless otherwise noted, all of these changes are effective 4/22/2022.

Covid 19 resulted in an increase in online commerce and, for merchants, a significant switch in their card transaction structure from card present to card not present transactions.. However, during the past year, we have observed a slow but steady improvement in volume compared to the challenges we all experienced in 2020 and early to mid-2021. We have identified the major changes made to Visa, MasterCard, Discover and American Express’ rates and fees.

Payment card processing fees are broken down into three categories:

- Interchange

- Assessment

- Fees

Interchange is paid directly to the issuing bank and are associated with a particular interchange category, depending on the criteria of the transaction. Visa and MasterCard publish their interchange rate tables online. American Express does not have interchange per se – they assess ‘discount rates,’ which essentially operate the same way as an interchange fee.

Visa

Visa fees vary based on a wide range of circumstances, such as card type (consumer or commercial), Merchant Category Code (MCC), transaction environment and more.

One of the changes that really stands out is to Visa’s Non-Qualified Consumer Credit interchange, which will increase from 2.70% + $0.10 to 3.15% + $0.10, an increase of 0.45%. Generally, merchant account providers apply Non-Qualified fees because the customer used a commercial card, foreign credit card or certain rewards cards. Additionally, the Non-Qualified rate may be applied to retail merchants that key-enter a transaction or fail to batch out at the end of the business day.

MasterCard

Regarding MasterCard, the highest rate increase we’ve observed is with their Standard interchange, increasing from 2.95% + $0.10 to 3.15% + $0.10, an increase of 0.20%. Standard rates are the highest rates that you can be assessed on a MasterCard transaction. Typically, standard rates are applied when the transaction does not match any of the basic qualifications, including but not limited to missing AVS data (Address Verification Service), not settling sales daily or failing to submit otherwise required data based on your merchant type.

MasterCard Enhanced Standard and World US Standard will also increase from 2.95% + $0.10 to 3.15% + $0.10. Conversely, High Value Standard and World Elite Standard will decrease from 3.25% + $0.10 to 3.15% + $0.10, a decrease of 0.10%.

Discover

Discover is one of the four major credit networks and is unique compared to other card networks. Rather than issuing cards through a third-party bank, Discover issues cards direct to consumers and commercial entities. Their interchange fees are not split between the card network and issuing bank; Discover fills both roles. Discover is therefore paid directly through the merchants credit card processor for each transaction.

The change that really caught our attention is the increase to their Commercial Electronic Prepaid interchange which is increasing from 2.30% + $0.10 to 2.65% + $0.15, an increase of 0.35% +$0.05.

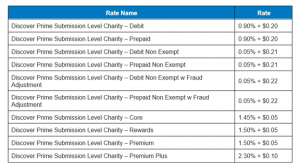

Discover will introduce a new Charity US Consumer Interchange Program, MCC 8398. Both card-present and card-not-present transactions are eligible for this program, and the rates are as follows:

American Express

American Express also issues cards direct to consumers and commercial entities. Unlike Visa or MasterCard, American Express credit card processing is not straightforward. Visa and MasterCard are both open credit card networks, meaning any financial institution can issue these cards. But American Express is a closed network, which gives them much more control over payment card merchant fees.

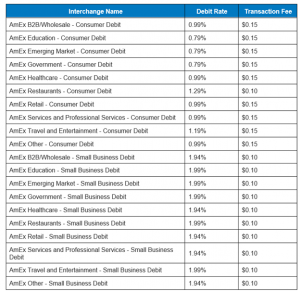

American Express is introducing a new Debit Card Program, which includes Unregulated and Regulated Consumer and Small Business Debit Products. Unregulated transactions are subject to the OptBlue Assessment, OptBlue Card Not Present, OptBlue App Initiated Tran and OptBlue International Fees. Transactions from these new products will attract the Debit Rates and Transaction Fees, as shown below:

American Express is introducing an OptBlue Acquirer Assessment and Transaction Fee of $0.165% + $0.02, effective 4/22/2022. This fee is applied to all American Express non-debit card charges (credit and prepaid), not credits/refunds, submitted under the Program for all industries in the American Express Program Pricing Signing Guidelines.