Dino Nicolaides, Managing Director for the UK and Ireland at Redbridge, encourages Treasury Centers, that are powerful drivers of operating performance within multinational groups, to strengthen their value add through the optimisation of bank fees and services. His insights into successful renegotiations are drawn from numerous engagements with international treasuries. They revolve around three key principles: transparency, benchmarking, and an end-to-end approach.

Tracking and Negotiating Bank Fees

An Often Underestimated Issue

An Often Underestimated Issue

Why do treasury centers so rarely take a close look at their bank fees?

– Dino Nicolaides: Treasury centres usually play a significant role in the efficiency and effectiveness of the treasury operations of a multinational group. Consequently, they are not exempt from the same challenges faced by any treasury department when it comes to tracking and optimising bank fees.

In general, the fees associated with bank services are often pushed down the list of priorities by finance departments, overshadowed by other, seemingly more strategic areas of banking relationships. For treasury centers—whose banking relationships are often determined at group level — managing the cost of these services tends to fall even further down their operational focus.

Furthermore, the inherent complexity of measuring and monitoring the cost of bank services imposes an additional challenge. Account analysis statements are rarely transparent: invoices can be difficult to comprehend as they are filled with technical service codes, which makes it hard to accurately assess service performance and cost. Many treasurers admit that they lack reliable benchmarks and analytical tools to evaluate these fees in detail. In the absence of a comprehensive fee database, discussions around cash management costs often remain superficial. Ultimately, treasury centers end up tolerating fee levels at far higher levels than what they should be.

There is also a lingering concern that pressing too hard on costs could damage the banking relationship. Yet with the right approach, it is entirely possible to secure far more competitive terms while preserving — and even enhancing — the balance of the relationship.

– What are the key steps to a successful renegotiation of bank fees?

– The process begins with collecting and centralising account analysis statements so that data and facts speak for themselves. We start with a detailed review of the invoices to clearly identify which services are being charged, and at what volumes. This analysis helps uncover erroneous charges, eliminate unnecessary services, and refocus spending on those bank services that genuinely add value to the treasury function. Because this is a laborious piece of work for a treasury function, we, at Redbridge, have a specialised Data Team who can seamlessly complete this task as it is indispensable to establish the facts.

Once this detailed analysis of partner bank pricing is at hand, the next step is to assess the competitiveness of each service. At Redbridge, we draw on a unique global database—built over 25 years of engagements with European and American corporations of a global spectrum. Using our proprietary technology tools, we benchmark every fee line in any part of the globe to quantify the savings potential.

Armed with this analysis, we then move into structured negotiations with banks — typically through an RFP, or via bilateral negotiations — while maintaining a balanced and constructive dialogue. This three-step method—analyse, benchmark, negotiate—makes all the difference. In the end, what was once seen as an unavoidable fixed cost becomes a source of lasting optimisation.

Leave No Stone Unturned

FX Costs, Excess Cash, and a Global Perspective

FX Costs, Excess Cash, and a Global Perspective

Beyond bank fees, what other optimisation opportunities should treasury centres explore to maximise gains?

– Optimisation should not stop at the pricing schedule. There are also other sources of savings available to Treasury Centres.

Let’s start with FX costs and more specifically FX margins. The spreads banks apply to foreign-exchange transactions (spot/forward/swaps) represent a non-trivial expense for companies with large international flows. We frequently observe significant margin differentials from one bank to another for similar currency pairs and transaction sizes. A detailed analysis of the components of these margins, benchmarked against market pricing, often reveals substantial potential. A structured renegotiation of FX terms can yield much more competitive rates without changing banks, FX platforms or disrupting daily operations. It is a form of painless optimisation of a cost line that is often under the radar.

Another avenue is the yield on deposit balances. This topic has returned to center stage with the normalisation of interest rates. During the years of negative rates, many treasury centres allowed liquidity to sit idle in non-interest-bearing current accounts, considering the issue of insignificant value — some even paid to maintain excess balances. Today, with positive rates, failing to put excess cash to work entails a real opportunity cost. It is therefore worth revisiting how these balances are remunerated by negotiating better terms with banks for surplus cash at the Treasury Centre or business unit level.

So, is it essential to take an exhaustive view of banking service optimisation?

– Precisely. The winning approach is end-to-end. Rather than treating each topic in a silo, cash management fees separately from FX or yield on deposit balances , they should all be considered holistically as there can be synergies in a holistic optimisation.

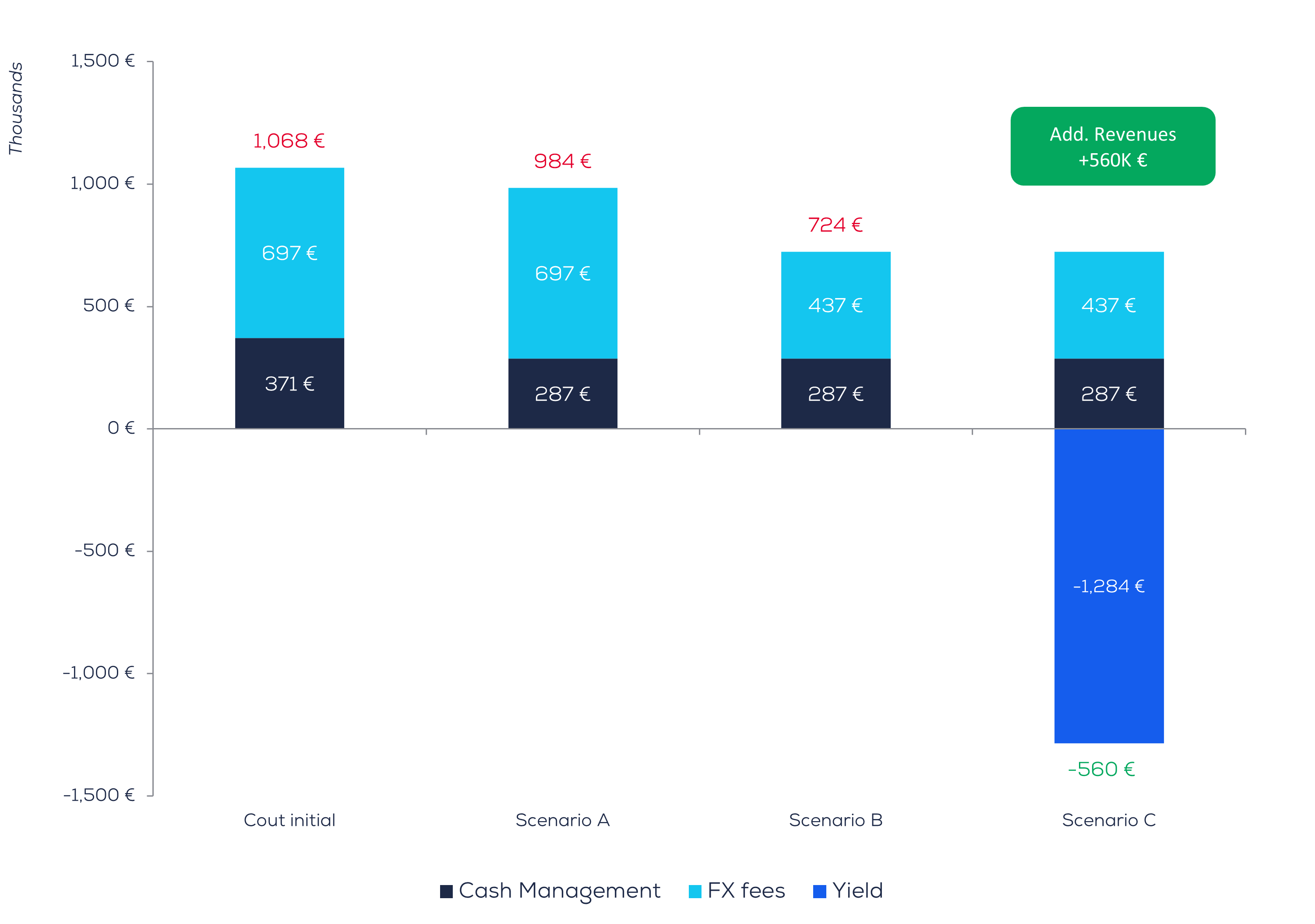

The results speak for themselves. In a recent project for a large international group, renegotiating cash management pricing alone offered strong savings. However, when the client decided to extend the optimisation to FX costs and yield on deposit balances, total potential savings increased by five times. To put things into context, before our project, the client paid €1.07 million annually in bank fees across five countries. After our optimisation across all parameters highlighted above, the cost line was transformed into a net revenue stream as the negotiated yield ended up being higher than the optimised costs — all achieved while safeguarding and reenforcing the client’s bank relationships (see graph below).

Example – Holistic Renegotiation of Bank Fees

Scenario A: renegotiation of bank fee pricing grid only

Scenario B: integration of FX cost optimisation

Scenario C: holistic renegotiation including yield on deposit balances

Source: Redbridge – Cash Management Advisory, September 2025

In conclusion

– Can you summarise Redbridge’s approach to optimising bank fees and services and explain why it is suited to even the most complex environments?

– At Redbridge, we explore a range of solutions to help clients manage multi-account and country treasury operations more efficiently. What matters is an end-to-end and dynamic perspective: combining the best technology, robust market benchmarks, and human expertise to drive continuous optimisation. In complex environments—with multiple banks, accounts, and currencies—this approach turns complexity into an opportunity. Every account, every bank service, every cent of fees can be reviewed within the framework of existing partnerships. The outcome is a triple benefit: substantial savings, enhanced operating efficiency, and greater transparency for the treasury function. To treasury centers, the message is optimistic: even with structural constraints, meaningful room for improvement exists. With a structured approach, you can regain control of bank fees and unlock value where none seemed to have ever existed.