Almost eight in ten MT 103 cross-border payment messages are now sent via GPI, making Swift’s initiative to improve the level of banks’ services in cross border payments a great success. However, will the rise of new technologies such as blockchain and cryptocurrency now challenge Swift’s dominance in the cross border payments field?

Before and after GPI

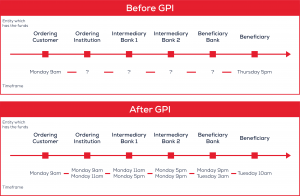

Cross-border payments are renowned for their pain points, hidden costs and opacity. Historically, neither the sender nor the beneficiary had any details on the location or date of arrival for payments. As a response to these issues, SWIFT introduced a new and improved service, SWIFT Global Payments Innovation (GPI) in 2016 and has continued to make improvements to this service over the years. SWIFT gpi is based on a multilateral Service Level Agreement (SLA) across banks to implement common processing standards that improve speed, transparency, and tracking mechanisms of international payments.

Since its launch, adoption has been slow but steady. Today, 78% of all cross border MT103 messages are now being sent via gpi, this equates to nearly $438 billion daily. Including both financial institutions and corporates, there are over 1,800 live gpi clients. According to Kalyani Bhatia, SWIFT’s Global Head of Payments, banks and corporates are seeing the benefits of using gpi. She explains that banks are seeing less inquiries and investigations since clients have access to real-time information, saving client’s time and money. Additionally, cross-border payments through gpi are considerably faster than before. Around 44% of payments are credited within five minutes, 70% under 30 minutes, and nearly 100% under 24 hours.

Source | iBanFirst

Source | iBanFirst

The GPI initiative

Overall, SWIFT has three main goals with GPI:

- Empowering customers and smaller banks

- Modernizing and digitizing global payments to meet new standards

- Accelerating embedded finance

In order to achieve these goals, banks and other financial institutions have invested a significant amount of time and resources on improving and adopting SWIFT gpi. A complete list of banks that are members of the SWIFT gpi community are included here. According to a major American bank, SWIFT gpi can be leveraged in different solutions. The bank does this by offering multiple gpi solutions to its customers. First, clients can use online banking module to visually track and trace outgoing payments in real-time and see any charges that have been deducted along the way. In addition the bank offers an online portal which is publicly accessible. Clients can leverage this tool by providing a URL to their payees who can then keep track of the payments made to them in real time. The bank also provides solutions enabling clients to integrate gpi data with their TMS or ERP systems through APIs. Using these APIs clients can integrate outgoing and incoming transactions enabling optimized use of intraday liquidity and forecasts.

Advantages

According to a global firm in the commodities industry, the main advantage of SWIFT gpi is traceability. Users can now track and trace international payments through a unique tracking number called a UETR (unique end-to-end transaction reference). In North America, clients can choose their own UETR. This new functionality is very important because before gpi, each bank had the ability to change the tracking number throughout the process, making it very difficult for clients to track payments. The tracking number enables users to check the status of payments as well as the fees paid each step of the way. The latter is a key advantage for this firm as they are now able to tell their beneficiaries the status of payment, which contributes to building stronger partnerships with suppliers and avoid long and costly investigations. Additionally, transactions that go through gpi are significantly faster, which enables liquidity efficiencies. Transactions that used to take days now take a matter of minutes for most companies.

Drawbacks

However, corporates still encounter issues with gpi. SWIFT gpi’s capabilities can vary from bank to bank. While larger banks offer gpi data with a considerably high level of detail, this is not always the case for medium-to-smaller banks. For instance, while some banks allow their clients to access SWIFT gpi’s tracking system directly through their internet portals or APIs, others require corporates to pass through the bank’s customer service. Overall, corporates need to keep pushing their financial partners to adopt the latest services available to fully benefit from SWIFT gpi’s advantages.

Future of GPI & alternatives to SWIFT GPI

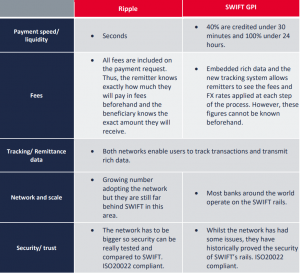

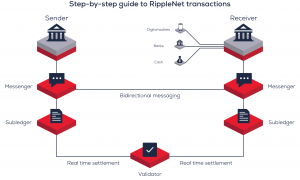

The rise of new technologies such as blockchain and crypto currencies is now challenging SWIFT’s dominance on the cross-border payment industry. Several fintechs are developing innovative solutions that intend to improve the services offered by the rigid traditional players in the financial industry. One that stands out on the cross-payment market is Ripple. Branded as the “internet of value”, Ripple is a global decentralized network that connects payment providers around the globe. Ripple promises to solve most of the issues related to cross-border payments such as payment speed, fees, and transparency. This is achieved by the use of a decentralized consensus model in which a set of computers determine which transactions sent by the network are valid. In addition, Ripple’s cryptocurrency, XPR, uses the power of the blockchain to confirm transactions in seconds with a very small cost. Below is a step-by-step guide to transactions on the Ripple network.

Their three main products, xCurrent, xRapid, and xVia enable members of the Ripple network to process real-time payments, lower the costs of processing and settlement, and minimize liquidity costs. Over one hundred banks and other financial institutions, such as Santander Bank, American Express, and MoneyGram, have joined the Ripple Network. The table below summarizes and compares the Ripple Network and SWIFT gpi.

Source | Ripple

Source | Ripple

Updates and Improvements

SWIFT and its members are constantly listening to the marketplace in order to make updates and improvements to current and new gpi features. Two other gpi products that SWIFT offers are Pre-validation and SWIFT Go. The pre-validation feature enables the sender to validate the beneficiary’s account prior to sending the payment. This enables the payment process to be faster and smoother allowing financial institutions to catch problem areas at the beginning, 75 banks have already signed up for this service. SWIFT Go specifically targets consumer low value retail payments. The normal SWIFT gpi SLA is 24 hours, for SWIFT Go they have reduced the SLA to four hours. Ten customers are live on this service and 100 more are in the implementation process.

SWIFT is updating the gpi platform in November 2022 with features to bring ISO20022 to all of its members. By 2025 all financial institutions have to switch from MT messages to ISO. SWIFT understands that all banks will transition at different times and the new platform will allow its members to switch at their own pace. The ISO format provides more information than MT messages and SWIFT wants to ensure corporates do not lose any valuable information during this transition to ISO. To do so, the new SWIFT platform will keep all of the information along the payment process on its own platform to ensure the integrity and security of data.

SWIFT is still the principal network used for cross-border payments, with over $100 trillion USD being transferred through the SWIFT gpi network. A considerable number of financial institutions and corporates across the globe have adopted the SWIFT network and several of their underlying products such as SWIFT gpi. However, an increasing number of new solutions for B2B cross-border payments are being developed. When making cross-border transactions, corporates should seek to understand and evaluate their options, taking into account the pros and cons of each solution.

Ashley Krause & Pedro Hernandez

A special report on the cash management & payment trends that will transform your treasury department in 2022

The growth and vitality of the payments industry has fascinated all observers during the past two years of the pandemic. Now with recent geopolitical developments arising from the Russia-Ukraine conflict, it is being tested again.

Our new publication analyzes the most prevalent trends and innovations in the treasury world today.

Included in this publication:

- The Global Resurgence of QR Codes

- Choosing the Right Payment Terminal in an Ever-Changing Environment

- The Rise of Buy Now, Pay Later

- PCI Compliance in an E-Commerce World

- Where Do Banks Stand in the Race for Digital?

- Virtual Accounts, Which Companies Should Implement Them?

- The Future & Alternatives to SWIFT GPI

- Global Digitization in the Depository Space

- “Switching Banks Was the Right Decision”: An Interview with Olivier Bouillaud from Albéa

Download the full publication