The world of payments is in a permanent evolution but some changes are bigger than others. In today’s environment, where commercial exchanges are globalized, payment transactions are tremendously varied, numerous and complex. To tackle this point, the payment industry is preparing itself for the largest migration of the century: the migration to ISO20022.

Why is the MT standard being phased out?

Created in 1973, SWIFT (Society for Worldwide Interbank Financial Telecommunication) is a private company that developed the SWIFT network, which enables all businesses and financial institutions to connect and exchange financial messages.

In 1977, the first electronic message using the MT standards was sent. Since then, SWIFT has introduced many changes and innovations to the MT messaging system. Although the new MX standard was introduced in the early 2000s, the old MT standard remains predominant.

The industry, however, has decided to replace the old MT standards entirely with MX messages because they are compliant with ISO 20022 standards.

When will the MT format no longer be available?

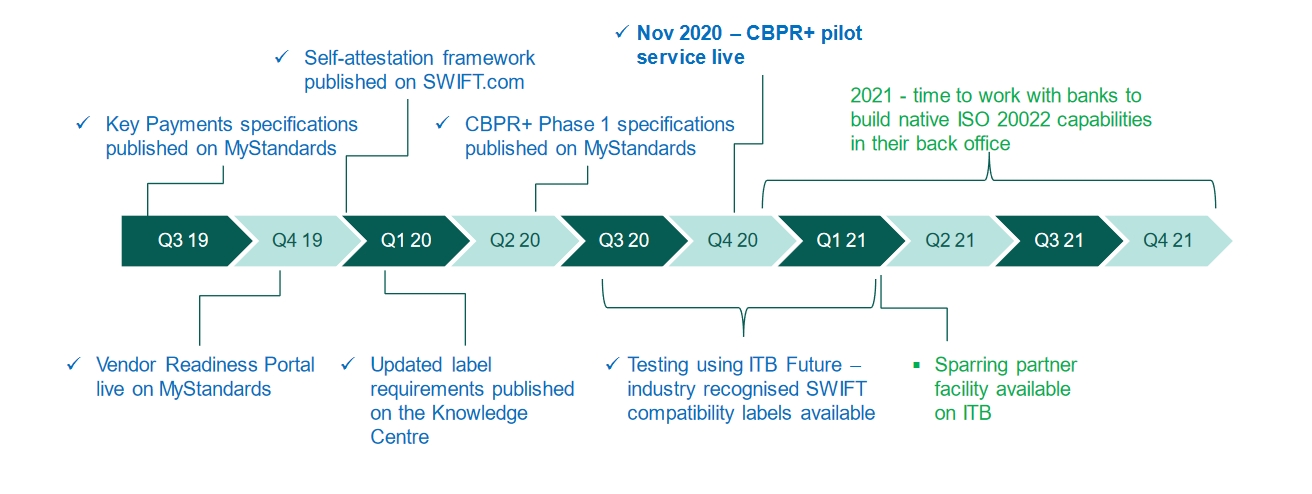

The adoption of the MX format will be progressive and depends on countries or regions. In the European Union, cross-border / high value payments across the regions going into the SWIFT Network, Target2 and a few others in scope will be transitioned first in November 2022. The U.S. Federal Reserve will transition in November 2023. Both formats will coexist until 2025 (the deadline set by SWIFT), and most of MT messages will then no longer be permitted. The following figure shows the timeline planned for the interbank space.

Source: ISO 20022 Programme – Quality data, quality payments

What is the main difference between MT and MX messages?

Message type (MT) messages are structured according to the specifications of the ISO 15022 standard, using the FIN protocol. MX messages are structured according to the ISO 20022 standard and use the XML protocol.

Message structures

MT messages are followed by a three-digit number:

- The first digit indicates the message category

- The second digit indicates the message group

- The third digit specifies the message type

The MX message is composed of four parts:

- 4 alpha characters indicate the message type

- 3 alphanumeric characters identify the message number

- 3 numeric characters highlight the message variant

- 2 numeric characters indicate the version number

For example, a single customer credit transfer MT 103 will appear as pacs.008.001.0x in MX format.

MX messages will be composed of 940 separate fields and will incorporate more structured, robust and comprehensive data.

What are the advantages of the MX format?

The goal of this new standard is to use the same message structure, form and meaning to relay financial transaction information around the world.

Who does the ISO migration affect and how?

The migration will affect all SWIFT members: banks, brokers, corporates, non-bank financial institutions, service providers and others.

The impact on banks

Some banks already support ISO 20022 for corporate payment and account statements services. However, if they do not, process changes are required to transform the internal processes to be interoperable with future market infrastructure ISO requirements.

Most banks have legacy messaging platforms that have been in operation for years. The new ISO 20022 migration, along with the overall shift in the payment industry to “instant,” will place immense pressure on banks by making these platforms obsolete. Banks will have to choose between fully upgrading their platforms or building an external, integrable system. If they do not act, they risk making their existing products and services inoperable.

The impact on corporations

The migration will impact end clients in multiple ways while also offering new opportunities.

For example, some legacy payment messages allow address information to be inputted into a nonspecific field and in no particular order. ISO messages, however, require filling in building number, street, city, and other specific data fields. Breaking down the addresses, coupled with procuring any missing data fields, will likely prove a cumbersome task for end clients. If the migration of data fields is not mapped and prepared properly, a significant risk of data loss or data integrity arises.

Corporate treasurers should ask their ERP providers when they plan to migrate from the MT format and the formats they will able to receive. Treasurers should also ask their banking partners what formats they will be able to send and receive in the future.

The impact on treasury management systems

Regarding banking communication, some treasury management systems (TMS) are already integrated with a transcoder that converts data to any target format. As a result, there is no impact in terms of development. This transcoder is available for all clients, enabling them to be autonomous.

However, this integrated solution required that, on the company side, the ERP must be able to provide the needed data to build the target file because MX messages contain more information than MT messages. In some cases, the transcoder permits the user to apply rules in case the ERP is unable to provide all of the information to build a viable file.

In terms of information processing, the capacity of the TMS to manage large volumes may be a concern. MX messages are very dense, which will test the robustness of the existing banking communication, posing potential speed and storage issues for vendors.

SWIFT is offering a Test Sparring Partner to enable members to test to confirm that their systems can send and receive the messages to validate functional integration testing. Most SWIFT users are aware of this offer, but some may be unaware. Detailed information on this migration is available on the myStandards web portal.

Achieving a successful migration

TMS providers remain highly dependent on the ability of banks and ERPs to provide the new formats. The new MX standard involves several parties and requires all of them to coordinate and communicate to ensure a successful migration.