The world often appears large and disconnected, with differences of religion, culture, language and currency that reinforce our independence. Despite these perceived differences, we are, in reality, linked closely together. Our points of connectivity expand with each technological advancement –write Justin DiCioccio, Redbridge Senior Analyst, and Constance Veron, Redbridge Associate Director.

Technology and the development of vast electronic networks fuel an ever-growing global economy that relies on cross-border payments and our ability to send and receive funds from one side of the world to the other, despite our differences and recurring challenges to overcome.

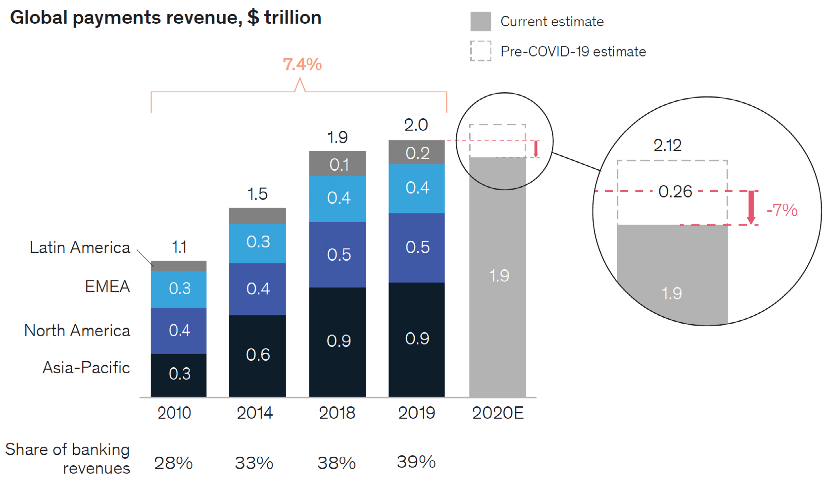

The impact of COVID-19 on global payments revenues

Due to the disastrous economic impact of the COVID-19 virus around the world, revenues from global payments for the first six months of 2020 were 22% lower than the same period in 2019, according to the 2020 McKinsey Global Payments Report. In the last six months of the year, as business regained some level of normalcy, global payments revenues rebounded. By the end of the year, total payments in 2020 were just 7% below 2019. B2B payments—nearly 80% of all cross border payments—are projected to reach $35 trillion by 2022, up almost 30% from 2020 levels, as reported by emerchantpay.

Source: 2020 McKinsey Global Payments Report

How vital are payments revenues in the global banking ecosystem? They make up about 40% of overall banking revenues. Transaction banking remains a huge revenue source, but it is time to give cross-border payments the attention it deserves.

Cross-border payments through bank transfers

There are many different methods to complete a cross-border payment, but bank transfers remain one of the most popular. A transfer typically takes 2-5 business days to complete, depending on the number of intermediary or correspondent banks the transaction must pass through. The lengthy processing time results from the numerous parties required to process the transfer and regulatory delays. About one in every 200 international payments is affected by a regulatory or investigatory delay.

The status of a payment and its associated fees is difficult, if not impossible, to calculate in advance, track, and reconcile at settlement due to the number of entities typically involved in the process.

Determining the cause of a payment failure or where in the process the failure occurred is equally challenging and time-consuming. It is not a surprise that many corporate treasurers rank payment traceability and fee visibility at the top of their priority list when it comes to overhauling cross-border payments.

Fortunately, two new payment options—SWIFT gpi and Visa Direct—are now available to address these cross-border payments issues.

- SWIFT gpi

Around since 2017, the SWIFT global payments initiative (gpi) continues to evolve and gain market dominance in the banking industry with daily volumes of $300 billion. SWIFT gpi allows corporates to track the status of a cross-border payment and gain visibility into the associated fees. SWIFT gpi uses a unique end-to-end transaction reference (UETR)— similar to blockchain technology—to track the status throughout the process. Each bank in the process, from initiation to delivery, is required by gpi to confirm the status and fees of each transaction in real time. When the status report reaches the originating bank, it is subsequently available to the customer, so that all remittance information is transferred to the beneficiary.

Using this same UETR, payments can be prioritized and processed to make payment information available immediately. The beneficiary can use the funds even if the actual transfer occurs at end of day since only the information regarding the payment is sufficient for remittance. Under the legacy cross-border and correspondent bank systems, correspondent bank charges can range anywhere from $5 to $50 for cross-border remittance while a SWIFT gpi message only costs $0.04. Even though banks may not voluntarily reduce their charges, the transparency provided by SWIFT gpi will gives users leverage to negotiate.

SWIFT gpi’s latest development—low-value cross-border payment service—is in the pilot stage and set to be available to all gpi financial institutions in 2021. This service is designed to help retail and small- and medium-size enterprises (SMEs) complete their cross-border payments with the same high-speed rails already in place. As cross-border payments, especially B2B payments, continue to grow with the expansion of SMEs, the dominance of legacy systems and correspondent banking will not continue.

- Visa Direct

Visa Direct provides cost, arrival time, and data transparency for cross-border payments. However, what separates Visa Direct is its ability to send funds to other cards and bank accounts, without integration with correspondent banking networks. Though Visa Direct has been around for a few years, it continues to expand its capabilities in functionality, countries, and currencies. Today, it is available in 200 countries and over 160 currencies for sending and receiving funds. In over 75 countries, customers can receive real time or same day cross-border payments. A faster simpler payment experience than that of international wire transfers or other legacy bank transfers, Visa Direct is a viable crossborder payment option for B2B, B2C, and even peer-to-peer (P2P) payments.

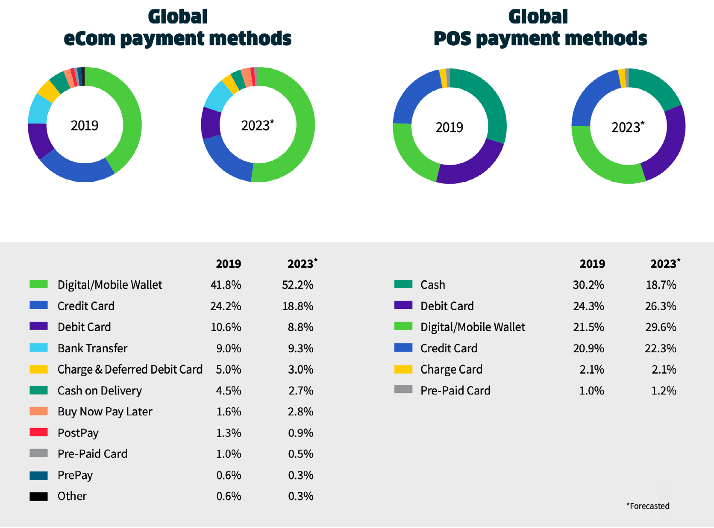

As borders gradually blur with the development of cross-border payments, local payments are still required for a full panel of payment options. Local payments are regional payment methods such as digital wallets, bank transfers, cash vouchers, local debit networks, open invoicing, and many other methods.

Providing options for customers to pay with their preferred local payment methods permits merchants to widely expand their market. From one region to another, these methods can be different as they relate to the country, culture, and technology. For example, credit cards are mainly used in the U.S. Alipay and WeChat Pay are by far the preferred method in China, while cash is still king in Latin America.

Source: Worldpay Global Payments Report 2020

It is crucial that merchants think globally but act locally

Local payment options overtook card payments in 2019 for e-commerce and point of sale (POS) transactions globally. A Worldpay study predicts this trend will intensify in the coming years as payment providers observed a reduction of up to 30% in cart abandonment rates by adding local payments methods.

Cross-border payment trends

- Digital wallets and solutions

Digital wallets are becoming more popular across the globe as payments shift to digital and mobile payments. The pandemic demonstrated the benefits of digital payment solutions by preventing close interactions at the point of sale, thereby reducing the risk of COVID-19 transmission.

Though available beyond a country’s borders, the most popular digital solutions—PayPal (US), Alipay (China) and WeChat Pay (China)—are primarily used locally, accounting for 46% of the e-commerce transactions in Asia-Pacific (APAC). European customers are beginning to follow the same trend using PayPal, Vipps (Norway), or Mobile Pay, while more than 70% of customers in Germany pay with their e-wallet or bank transfer.

- Cards

Credit cards continued to dominate the North America market in 2019, though a large portion of the volume is expected to shift to mobile and digital transactions over the next few years. North America remains a leader in technology payment.

Nevertheless, debit cards and local networks remain essential to perform business in Europe, Latin America, and APAC. These local cards need local processing locally as international payments are unavailable for customers. For example, most of the cards issued in Brazil are domestic use only and cannot be used for cross-border payments. A wide variety of local networks, such as PagoBANCOMAT® in Italy, Cartes Bancaires in France, and BankAxept in Norway, remain essential for buyers in Europe.

Last but not least, even in China where global networks like Visa and Mastercard are available, they still only represent a small portion of the cards issued as CUP is the overwhelming market leader.

- Cash

While cash is king in Latin America at POS, it is also a very popular option for ecommerce transactions. Its market leadership is due to a sizeable underbanked population, high customer fees, and fraud. PostPay is very popular in Latin America, especially in Brazil, with Boleto Bancário. PostPay services, like Boleto Bancário, allow customers to make purchases electronically and then complete their transaction with cash at ATMs, convenience stores, and bank branches. This payment method is popular across Latin America, with Rapipago in Argentina and PagoEfectivo in Peru.

- Bank transfers

This cashless payment method endures in Europe and Asia. The customer does not need a credit card, simply confirming payment by a transfer from his or her bank account to the merchant at the end of the process. This can be done online or by email or phone. Almost 60% of Netherlands customers prefer to pay their e-commerce purchase with Ideal, while 51% of German customers use Giropay.

Multiple payment methods exist around the globe, locally and internationally as well as legacies and new. Despite technological advances, most legacy payment methods like cash or use of the correspondent banking system are unlikely to vanish.

While new payment methods offer many positive features, legacy payments have a place in the local and global economies. However, one thing is certain: the relationship between a business’ success and its access to a plethora of payment options cannot be ignored.

An Insights From the Field special report on the treasury trends and innovations that swept 2020

Every crisis provides an opportunity for change and often produces dysfunctions and accelerates the need for immediate and disruptive actions. Change was already in motion in 2020, and the pandemic only acted as an accelerant.

This publication analyzes the trends and innovations in the treasury world that were already in motion before the COVID-19 pandemic began and that either accelerated or gained tremendous publicity during the pandemic.

Included in this report:

- Deposit Strategies in a Changing Banking Landscape

- The Pros and Cons of Faster Electronic Payments

- COVID-19 Forced My Digital Transformation. Now What?

- Where We’ve Been and Where We’re Going: An Overview of 2020-2021 Card Brand Changes

- Transitions in the Global Payments Market