With all of the uncertainty in today’s world – economic turbulence and political turmoil – it’s more important than ever for businesses to be able to forecast future cashflows accurately.

The value of cashflow forecasting

Forecasts are not only important for defining and making investments, but also for ensuring a company’s future viability. A 2019 study conducted by Redbridge showed that 94% of companies carry out some form of cashflow forecasting*. So, for most companies, the question is not should they predict what cash will be generated in the future, but rather how should they produce their forecast?

Methods for forecasting cashflow

Cashflow forecasting involves estimating cash inflows and outflows over a specific period of time. Companies use two main methods to predict what their future cash situation will be. Each has its individual strengths and weaknesses and may be used for different reasons.

The indirect method

The first method is known as the indirect, or budget method. It involves the use of balance sheet items to determine the company’s monthly ability to generate cash for the year as a whole. This method makes it possible to define long-term strategic objectives. It also creates a cash culture within the company, which can have a positive impact on working capital and the cash conversion cycle.

Because the budget method involves a production delay (lasting anywhere from 8 to 30 days following the end of the month), there may be a lag of as much as a month before it can be determined if the original forecast was correct. Consequently, there may be more political overtones to the forecast, with a need for more buy-in from other teams. And as the financial year goes on, the objectives may need to be adjusted. As a result, with this indirect method, it isn’t always possible to monitor the performance of the cash and transform the reporting into a useful management measurement tool.

The indirect method is relatively easy to manage, as you can rely on the balance sheet data, but…

- non-cash transactions (such as depreciations, losses and bad debts) need to be added back in

- cashflow receipts and payments are less granular and less accurate

- this method can’t spot intramonth funding shortages

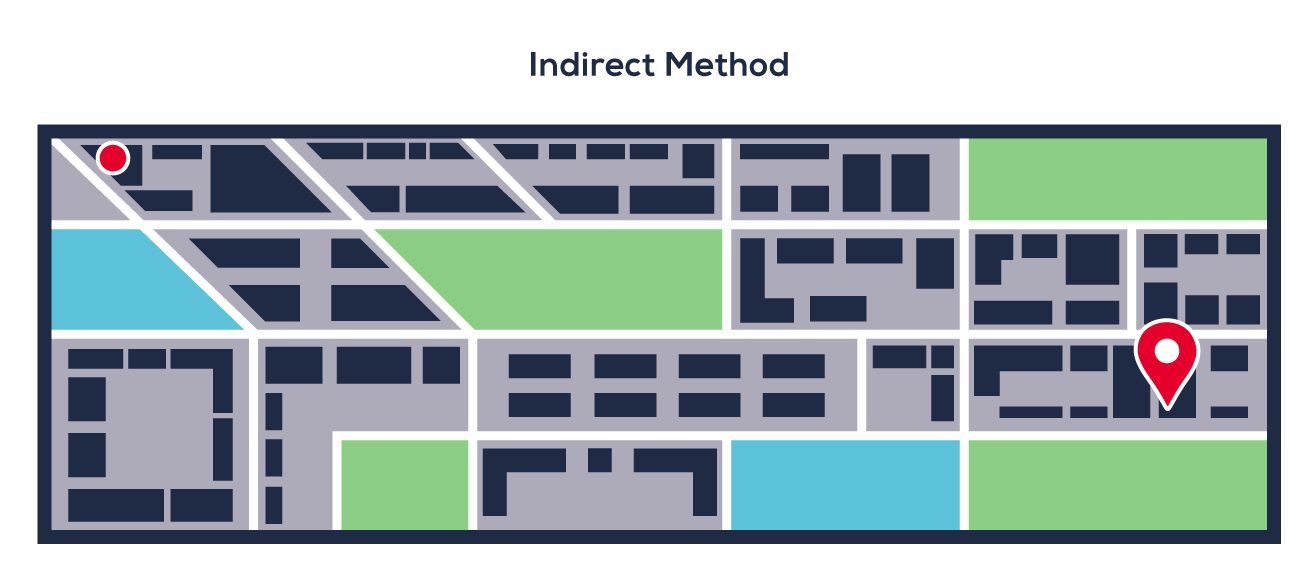

A good way to visualize the indirect method would be to look at it as a type of map. Looking at a map using the Indirect method, you would only know your own position as well as your destination. Based off of that, you would have to head in the general direction of your destination and hope you picked a good route.

The direct method

The second method is known as the direct, or bank balance method. This method uses bank balances to define the cash the company generates on a weekly or monthly basis over the course of the quarter. This enables real-time monitoring of the cash conversion cycle. In addition, the group can use reconciliation to compare actual cashflows with the forecast to ensure close monitoring of cash to prevent fraud as well as for investment and management purposes.

The direct method might seem cumbersome at times because of how long it takes to set up with the proper amount of data as well as the regular updates it will need. However, it should allow you to overcome the limitations of the indirect method and to monitor whether or not the cash creation objectives of the year will be reached.

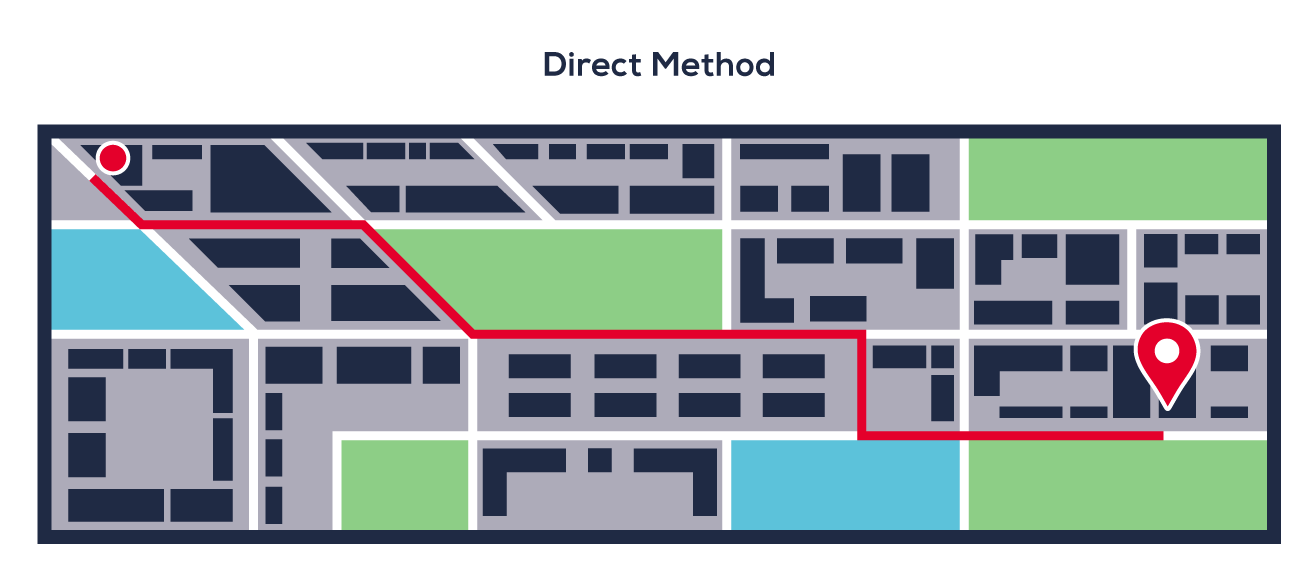

When it comes to visualizing the direct method, you could look at it as another type of map, similar to the direct method but with different information. On a map of the direct method, you would be more focused on the best route to get to your destination before you embark on your trip.

Reconciling both methodologies is a management necessity

So, what’s the best method among the two? That depends on what a company’s goals are, since both methodologies have different strengths and weaknesses. However, rather than simply choosing one method or the other, most of the time the best approach is to blend the two to create a hybrid approach. This provides greater flexibility that can be used to maximize the strengths of each methodology, while limiting their weaknesses.

Once they have been combined, both methodologies also balance out one another and provide senior management with both a long-term strategic objective and cash that can be used for short-term debt and liquidity investments.

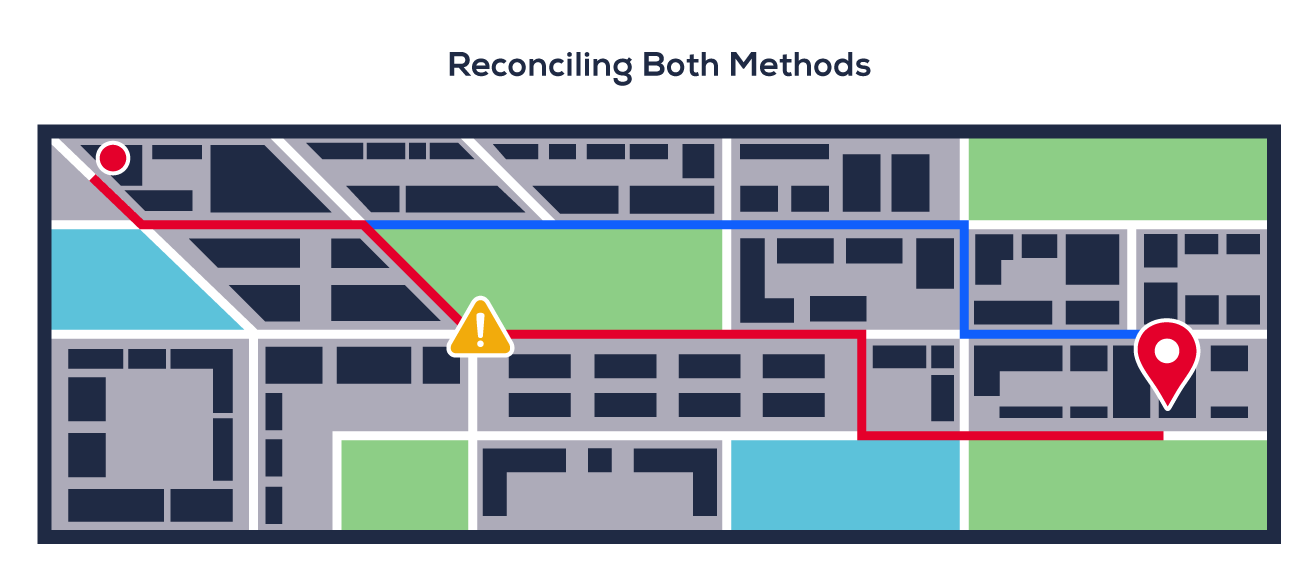

Visualizing the reconciliation between the two mythologies can be seen as another type of map. Reconciliation would be a hybrid map that takes what was provided by the previous two maps and provides live updates throughout your trip if anything were to change. For example, if there was a road closure, your route would be updated and a newer more efficient route would be chosen.

The Redbridge approach

Although it may seem straight forward, the first step in a cashflow forecasting project is not determining that a tool is needed. Even the best tool will be useless without high-quality data and efficient processes. The project also requires the involvement of other departments, including IT, because they will be closely involved in implementing it.

For this reason, when Redbridge works on a cashflow forecasting project, it takes the following approach to ensure success:

- First, we assess the quality of the source data. Future cashflows cannot be forecast properly without good data. We look at the quality of the data and determine how easy it is to access it. This leads to the question of system interaction and integration.

- We then determine your group’s goals and the accuracy objective at the legal entity, regional and country levels. This leads to a focus on the pattern of how the different data is collected.

- Finally, we assess production capacity. Do you need a tool to automate production? Is it better to use your treasury management system or a dedicated tool? Do you want to create a liquidity stress test to better understand your cash situation? Is artificial intelligence (AI) cost-beneficial for you? If you use AI, do you have historical data and does it accurately represent your activities?

Only after these and other questions have been answered can we help you determine what the right tool for your particular situation is. In addition, it is important to ensure that the data quality is sufficient and that there is buy-in from other key departments, such as IT, as they will serve as key partners. Taken together, all of these elements will ensure the success of your cashflow forecasting project.

While blending together different methodologies is a good strategy to ensure accurate cash flow forecasting no matter the situation, it is only one solution. In our next article, treasury consultant Solene Moyne will assess the different TMS and vendor solutions to produce accurate cash flow forecasting.