Gabriel Lucas, associate at Redbridge, takes a closer look at the basic elements of chargebacks, the standard chargeback process, and the ways merchants can mitigate chargeback risks and reduce their losses.

Chargebacks are usually one of the main concerns for merchants when accepting card not present (CNP) payments. However, apart from considering them an important risk to mitigate, I still come across many merchants who have a variety of questions, including:

- What is a chargeback?

- How do I perform a chargeback?

- What does the chargeback process look like?

- What are the chargeback codes? Why does a code sometimes not reflect the real reason?

- When does a chargeback become a financial loss for merchants? How do I deal with chargeback fraud prevention? Is there a reliable way to ensure chargeback protection for merchants?

Let’s take a closer look at the basic elements of chargebacks, the standard chargeback process, and the ways merchants can mitigate chargeback risks and reduce their losses.

What is a chargeback?

A chargeback is the process in which a cardholder disputes a debit or credit card transaction with their issuing bank, instead of the merchant, in order to claim a refund or recover potential fraudulent charges.

How do consumers perform a chargeback?

Consumers do not need to contact merchants, and sparingly do, before filing a chargeback, even though it might seem like the natural first step.

To initiate a chargeback, the cardholder contacts their bank and provides information about the dispute, such as fraud or not receiving an order. Banks have made this an easy process: often consumers can initiate a chargeback through their mobile banking app. The bank then reviews the transaction, and, if it judges the reason for the dispute to be valid, it issues a provisional credit to the customer’s account and immediately debits the merchant for the disputed amount. The bank will sometimes provide the customer with a provisional credit for the charge while it investigates the validity of the claim. The customer will have to provide evidence of the claim.

What’s the chargeback process for a merchant?

Chargebacks are initiated by the cardholder, evaluated by the cardholder’s bank, and either accepted or represented by the merchant. A representment, or resubmitting the transaction, occurs when the merchant believes the validity of the transactions or had already issued a refund. If there is a disagreement between the cardholder and merchant (and their respective banks), either party can go into arbitration so that the card network can make a final decision. Arbitration only occurs after the transaction is represented and the customer files an additional chargeback.

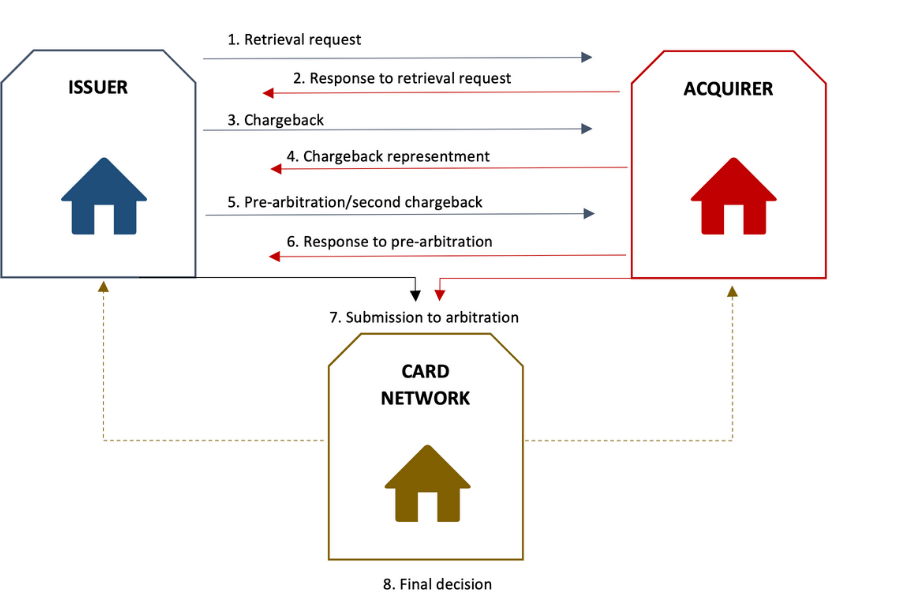

The standard chargeback process involves eight steps:

- Retrieval request: The card-issuing bank requests that the acquiring bank provide additional information for a given transaction.

- Response to retrieval request: Based on the information provided, the acquiring and issuing banks resolve the dispute, if possible. Otherwise, the acquiring bank transmits a chargeback notification to the merchant.

- Chargeback: The cardholder disputes a transaction that was made on their bank account. The issuer will first review the credit card chargeback dispute and then notify the acquirer, which notifies the merchant.

- Chargeback representment: The merchant either accepts the chargeback or fights it by submitting the necessary evidence (compelling evidence) to its acquirer, which sends it to the cardholder’s bank.

- Pre-arbitration or second chargeback: After reviewing the evidence provided by the acquirer and checking with the cardholder, the issuer either approves or rejects the dispute. If the issuer approves the dispute, the provisional credit will be reversed and returned to the merchant. If the issuer rejects the dispute, the issuer opens a pre-arbitration (Visa) or a second chargeback (Mastercard).

- Response to pre-arbitration (or second chargeback): The merchant has to provide an answer and confirm whether it accepts or rejects the pre-arbitration or second chargeback.

- Submission to arbitration: At this stage, if the issuing bank still does not accept the evidence provided by the acquirer, the chargeback can be submitted to the card network for a final decision.

- Final decision: The card network will examine the evidence and make a final decision. The losing party is then debited for both the chargeback amount and processing fees.

What are chargeback reason codes?

Reason codes inform merchants about the reason why the customer is disputing a transaction, based on the information they provided to their bank. Issuing banks follow standard rules to validate a chargeback and then associate it with a specific reason code according to the evidence that was provided.

Types of chargebacks

Chargebacks can be classified into three types: criminal fraud, friendly fraud, and merchant error. Each of them come from different circumstances, and banks will handle them differently.

Criminal fraud

Criminal fraud chargebacks occur when a scammer or identity thief makes an unauthorized transaction on a credit card. We strongly advise merchants not to waste time or resources attempting to dispute them; however, merchants can reduce these chargebacks by implementing powerful antifraud systems that utilize either a pre-authorization, post-authorization, or combined strategy.

Merchant error

Merchant error chargebacks happen when the chargeback is due to an error made by the merchant, such as shipping the wrong product, a damaged or defective product, or not delivering the product. This type of dispute can be sometimes represented effectively but the most recommended action is to identify and fix the root cause of the error.

Friendly fraud

Friendly fraud chargebacks refer to customers who abuse the chargebacks procedure by reporting valid transactions as being fraudulent to get a refund. Customers can behave this way on purpose, or they might do it by mistake or out of confusion.

Surprisingly, friendly fraud is the most common type of chargeback, accounting for 60% to 80% of all chargebacks. Merchant error, which makes up 10% to 20% of all chargebacks, is the next most common type. Only 5% to 10% involve criminal fraud.

Chargeback code vs. chargeback real reason

When the chargeback procedure is used legitimately, chargeback reason codes correspond most of the time to the underlying reality, based on the evidence provided by the cardholder and the cardholder’s bank’s analysis. The only exception would be a mistake from the cardholder’s bank when filing the chargeback.

However, especially in the case of friendly fraud, customers misuse the chargeback procedure, and, as a result, a chargeback reason code might actually be hiding a friendly fraud. For example, a customer claims they did not receive a shipped product when they actually did. For this reason, chargebacks need to be analyzed thoroughly to identify the root cause, and merchants need to implement solutions to prevent or at least limit these cases from happening.

Chargeback risks for merchants

Liability and Strong Customer Authentication

Merchants are by default liable for chargebacks and carry the burden of proof in case of a dispute. If the merchant takes no action, the consumer wins by default.

Since October 1, 2015, merchants accepting card present (CP) transactions that are not equipped with an EMV card reader are responsible for certain types of fraudulent transactions. If a fraudster pays with a counterfeit EMV card, and the merchant does not have an EMV card reader, which means that the merchant would have to swipe the magnetic stripe instead of insert the EMV chip, the merchant would be responsible for that charge. The liability shift has played an important role in accelerating the adoption of EMV, which is a much more secure way to pay for both customers and merchants.

In addition to the financial risk, using an EMV card for payment has become standard for most customers because it is much more secure. Accepting chip cards not only protects merchants against fraud but also lets customers pay in their preferred way.

For CNP transactions, the merchant is automatically liable unless Strong Customer Authentication (SCA) is used. Even though most acquirers currently dispute chargebacks due to criminal fraud—with no action needed from the merchant—some acquirers still require merchants to provide proof of 3D Secure authentication. If they do not provide this proof, the merchant incurs a loss that could have been easily avoided.

In either case, the merchant is still liable for chargebacks occurring due to merchant errors.

3D Secure may seem to be the perfect solution to mitigate chargeback risk because the liability is transferred to the issuing bank. However, applying SCA systematically can become a real conversion killer.

Developing a chargeback strategy

Every dollar lost to fraud costs companies $3.36, compared to $3.13 in 2019 and $2.40 in 2016, according to LexisNexis Risk Solutions. This makes developing an effective chargeback strategy essential for merchants.

The first step in merchant chargeback prevention is to determine how vulnerable the merchant is to chargebacks and its risk appetite. In other words, what level of risk is the merchant willing to take to maximize revenues?

The second step is for merchants to analyze the source of chargebacks. The analysis should start with the chargeback reason codes, followed by a deeper analysis to identify the real root causes in case they differ. This step aims at identifying the chargebacks that are really due to criminal fraud, those associated with merchant errors, and those that are most likely due to friendly fraud.

Taking the necessary actions

The third step should consist of taking steps to start eliminating each type of chargeback.

The first type of chargebacks to tackle is criminal fraud. There are many different ways to improve chargeback fraud protection. You must be equipped with a powerful scoring tool that enables you to identify fraudulent transactions before they happen (chargeback fraud prevention), while limiting the false positives (legitimate customers blocked by the antifraud tool). Merchants do not realize how much money they are leaving on the table by blocking real customers who are willing to pay and have funds in their bank account.

Merchants’ errors are the next type of chargeback that should be reduced because this type is the merchant’s responsibility. Merchant errors can range from having useless steps in the customer journey to having an unclear refund policy. A proper analysis of the merchant’s payment environment and needs is necessary to identify which processes and tools should be implemented to help avoid merchant error chargebacks.

The most challenging type of chargeback to reduce is friendly fraud. Friendly fraud is nearly impossible to prevent because by definition this type of fraud is perpetrated by real customers. Therefore, implementing an efficient chargeback representment process is key.

Merchants can adopt and follow several best practices to help reduce chargebacks due to bad refund and return policies.

In general, a deep analysis of the merchant’s environment can help prevent some types of chargebacks. One size never fits all because every merchant has its own unique needs, depending on its strategy and internal organization.