The Earnings Credit Rate (ECR) is a mechanism offered by US banks to help businesses operating in the US offset their bank fees. Functioning similarly to an interest rate – it’s often linked to the Effective Federal Funds Rate – the ECR is applied daily to the balance in a company’s non-interest-bearing account. Instead of generating cash earnings, however, the ECR results in a credit that is taken away from the cost of cash management services. This rate is an important part of a company’s relationship with its banks, but is frequently overlooked in banking negotiations.

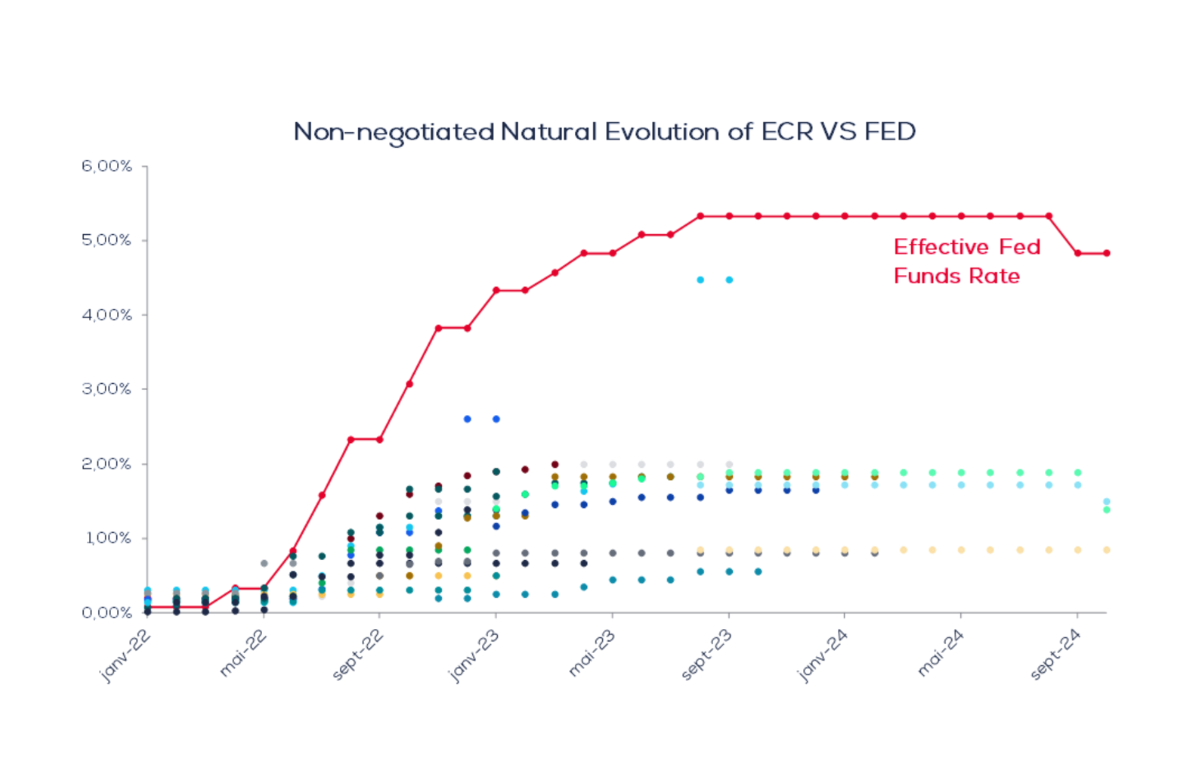

Imagine yourself in the position of a treasury professional relying on the ECR to offset your banking fees. When the Federal Funds Rate rises, you’d probably expect the ECR on your deposits to increase accordingly. However, when the Federal Reserve was hiking interest rates in 2022 and 2023, US banks only passed on some of the increase in rates to the ECR. They also took their time to do so, responding slowly after each rate hike. We can see this in the graph below, which shows the ECR yields for a number of US companies that shared their data with Redbridge prior to renegotiating their cash management services.

Fast-forward to today, and monetary policy is now being eased – the Federal Reserve implemented its first rate cut in September. Given banks’ actions when rates were rising, a treasurer might expect their bank to only reduce their ECR slowly now that rates are falling. And yet our initial findings indicate that US banks reacted promptly and in full to the September cut, reducing the ECR by 50 basis points.

This imbalance is clearly going to be frustrating for treasurers, who might naturally feel that all this is evidence of banks acting primarily in their own interests. They might now be expecting their banks to reduce the ECR by another 25 basis points if the Fed cuts rates again this week, as anticipated. That said, such adjustments are not set in stone.

Redbridge has a simple message for all companies operating in the US: the ECR yield you negotiate with your bank should be based on a transparent, automatic mechanism that’s fair for both sides. What’s more, it’s possible to establish a spread over the Fed Funds Rate the offsets your costs significantly more than your current ECR.

In short, even though US interest rates are expected to fall further, there’s still scope for firms operating in the US to reduce their costs of cash management.