In this article, Pauline Lion, Director, Cash Management Consulting at Redbridge, discusses a cost that many medium-sized companies unknowingly pay too much for. Through deducing the margins companies are paying banks for FX operations, benchmarking based on more than €1.5 trillion of historical FX transactions and disciplined renegotiations, she sets out a way to reduce foreign exchange costs.

Why medium-sized companies pay too much for FX transactions

You state that nine out of ten companies overpay for their foreign exchange transactions. Why is this a particular problem for medium-sized firms?

Pauline Lion, Redbridge: It is typically only companies with sophisticated foreign exchange management practices that are able to optimize their FX costs and closely monitor transactions. Such firms are generally handling large transaction volumes and using multi-dealer platforms such as FXall or 360T to create competition among banks.

In practice, this level of sophistication generally only emerges among large companies whose FX volumes exceed €300–500 million per year. Medium-sized companies, by contrast, usually transact bilaterally with one or two banks and do not use multi-dealer platforms. As a result, the spreads they pay are often well above the market average – in many cases ten times higher than what could be achieved through a structured negotiation process.

One example comes to mind: we worked with a company with an otherwise sophisticated treasury function that paid little attention to FX transactions because it did not make many. Some banks were charging the company spreads of up to 220 basis points for its FX transactions. After renegotiating the terms, we were able to reduce its FX costs by 75%.

The cost can be even higher for account-to-account transactions executed at automatic exchange rates. In these cases, bank margins can reach several percentage points.

“For companies that trade bilaterally with their banks, spreads are often ten times above the average level in the market – and can be ever higher.”

The margin the bank applies increases for each level of intermediation. Source: Redbridge – Cash Management Consulting, 2025.

The “all-in” rate: a blind spot in FX pricing

How is it possible that companies, even large ones, can fail to notice the excessive costs they are faced with?

Most simply do not have a clear view of what they are being charged. That’s because banks typically provide an “all-in” exchange rate that combines the market rate and the bank’s margin in a single figure.

While the FX confirmations sent by banks accurately describe the characteristics of each transaction, they generally do not disclose either the cost or the margin that is being applied. This is precisely where Redbridge steps in, whether for transaction-related FX activity or hedging operations.

The all-in exchange rate combines the market rate and the bank’s spread without distinguishing between them. Source: Redbridge – Cash Management Consulting, 2025.

Measuring, benchmarking and renegotiating

How do you determine what a company is actually paying?

We deduce the bank’s margin using the transaction confirmations that banks are required to provide to their clients combined with the extensive market data available to us.

Our benchmark database contains information about more than €1.5 trillion of FX transactions and is continuously updated. This enables us to accurately determine the spreads a bank is applying by comparing the executed rate with the interbank market rate at the exact time the transaction was carried out.

Once we have established the spread, we calculate a fair market price based on the bank involved, the currency pair and the size of the transaction.

Using this information, we engage in structured renegotiations with the company’s banking counterparties. Our objective is not to strain the banking relationship, but to secure transparent pricing schedules and market-aligned conditions without changing execution channels or disrupting day-to-day operations.

“We calculate the spreads banks are applying using transaction confirmations and the extensive market data available to us.”

Transactional FX versus hedging

You distinguish between transactional FX and hedging transactions. Why is doing so important?

Because they are fundamentally different activities.

Transactional FX covers day-to-day payments such as supplier invoices, payroll and import-export flows. They are processed through banking channels at automatically applied rates that are rarely negotiated. The underlying data about them is often fragmented and poorly structured.

By contrast, hedging transactions – including spot trades, forwards and swaps – are part of the risk management process. Pricing is negotiated at execution, and confirmations are detailed and time-stamped.

Both activities offer opportunities for optimization, but they require different approaches. We can help with both.

Tangible results and long-term monitoring

What results can companies expect when they work with Redbridge?

First and foremost, significant savings.

For example, we helped Gerflor reduce the cost of its FX operations across three banking partners and 13 currencies by 40%.

However, our work goes beyond cost reduction – it also helps foster a more constructive relationship between a company and its banks. Foreign exchange services represent an important source of side business for banks. Restoring information symmetry creates a healthier and more transparent relationship.

We also place considerable emphasis on making sure the savings a company makes are sustainable. In Gerflor’s case, its banks committed to transparent pricing schedules, and we implemented a joint monitoring process over a three-year period to ensure that the negotiated conditions are adhered to over time.

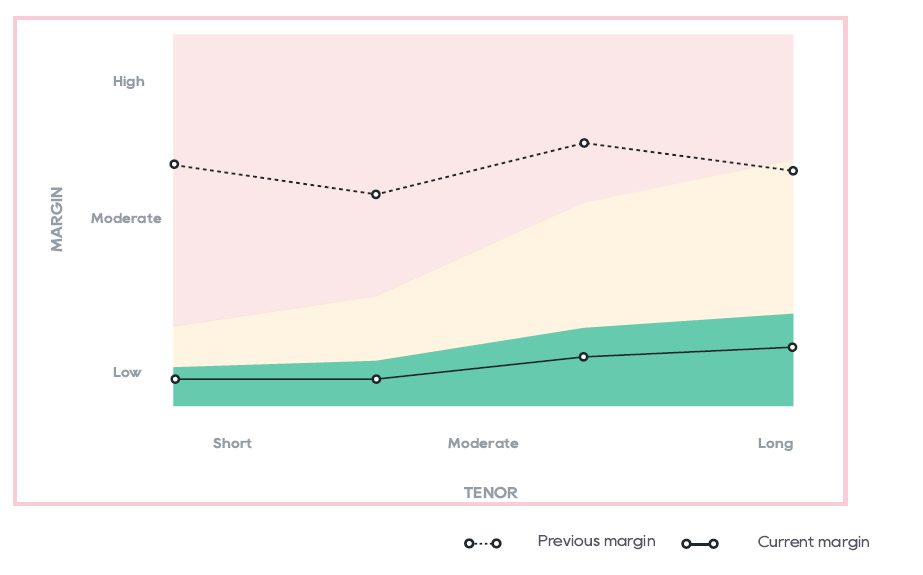

Your FX spreads benchmarked against fair market levels, by transaction maturity.

Source: Redbridge – Cash Management Consulting, 2025.

“Reducing information asymmetry between a bank and its client is always beneficial.”

What if a bank refuses to disclose the details of its margins?

This is a common concern, but rarely is it a major obstacle.

Most banks abide by the FX Global Code, Principle 36 of which requires accurate, time-stamped recording of orders. This audit trail, combined with our market data, enables us to calculate spreads even when the information has not been disclosed.

Where should a medium-sized company start?

It should begin with a no-obligation assessment of the potential to optimize your FX operations.

At Redbridge, we carry out such an assessment using what we call an FX Scorecard. We benchmark the cost of each transaction against a large universe of prices charged by banks to comparable companies at the point in time that each transaction was carried out.

You only need to provide us with a limited amount of data: one to six months of FX confirmations, which are readily available through your banking portals. We then provide you with our findings in under a week.

In my view, this is the simplest way to quantify an issue that companies often mistakenly regard as insignificant.