The pandemic has demonstrated the value of mobile payment solutions in helping mitigate the risk of virus transmission at points of sale. For Mélina Le Sauze, Director at Redbridge, the challenge for every retailer is no longer whether or not to accept mobile payment solutions, but to determine without delay which ones are best suited to their business and the needs of their customers.

In the future, the majority of payment methods will be digital and mobile, based on QR codes or NFC technology, and will offer value-added services such as promotional offers, multi-currency cards, deposits or instantly approved loans.

The following overview of innovative payment solutions outlines a vision for the future of payments.

Mobile payments as an alternative to cards

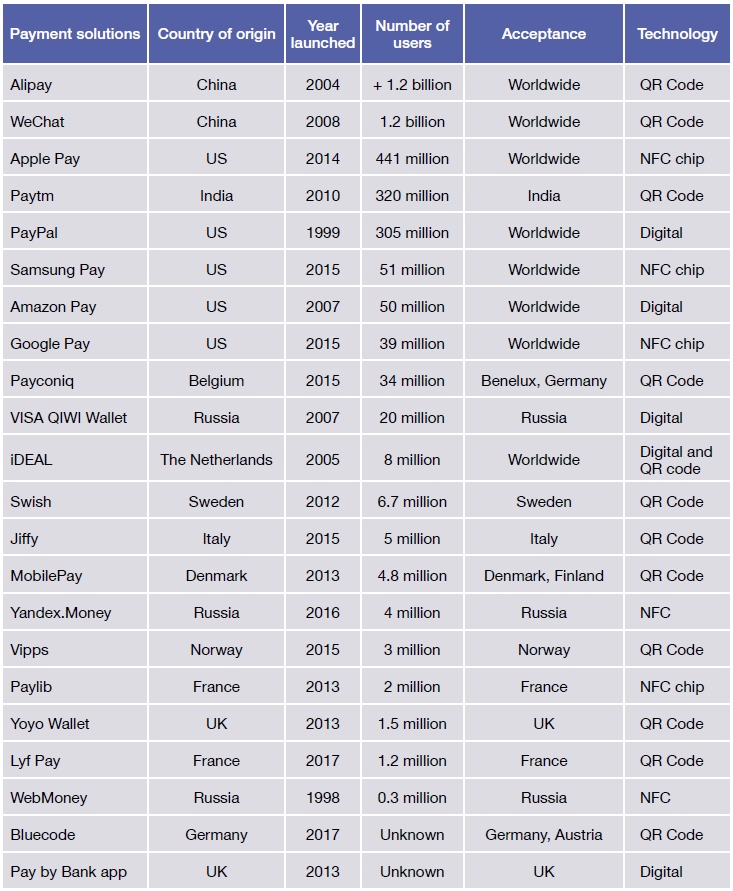

Over the past decade, mobile payments have been developed using a variety of technologies, transforming our smartphones into payment methods, whether for in-store or online transactions. Digital wallets (e-wallets) have emerged to make contactless payments using different technologies: NFC for a large part of Europe and North America, or QR code reading, especially in China.

The number of digital wallet users across the world exceeded one billion in 2019. More than two-thirds of these people live in the Asia-Pacific region, with China alone accounting for almost 50%, using services such as Alipay and WeChat. In China, the digital wallet is the preferred national choice among the different payment solutions.

Most e-commerce and in-store transactions rely on these applications rather than cards, and they also offer a wide range of related services, such as promotional offers, investments, insurance and travel reservations. There’s a similar picture in neighboring countries such as Singapore and India.

Solutions developed in the US that can be used anywhere in the world, such as Apple Pay, Google Pay and Amazon Pay, now account for over 5% of card payments, with Apple Pay currently the leader. The outlook for Apple Pay’s development is impressive, with forecasts that it could account for up to 10% of card payments by 2024. This would be achieved through further penetration of the European and Asian markets.

In Europe, millions of people make mobile payments every day, using a wide range of options. In addition to international solutions, such as Apple Pay, Google Pay and Samsung Pay, there are a considerable number of local initiatives available in Europe, such as Payconiq (Germany, Belgium, the Netherlands), Bluecode (Germany), Paylib and Lyf Pay (France), Yoyo Wallet (United Kingdom) and Jiffy (Italy). In the Nordic countries, almost 50% of the population use a digital wallet, thanks in particular to MobilePay solutions launched by Danske Bank in Denmark, Vipps by DNB in Norwayand Swish, which has been developed through a joint effort by a number of Swedish banks. These solutions have thus managed to acquire 13 million users from among the 27 million inhabitants of the Nordic countries.

The success of these wallets in Asia and the Nordic countries is such that, gradually, they can be used beyond their borders. Good examples of this include Chinese giant Alipay, which has deployed its payment solution in 110 countries, and the iDEAL solution, which is used by more than half of the population in the Netherlands, where three major Asian merchants decided to try to attract more Dutch buyers to their e-commerce sites by offering iDEAL as a payment option. As a result, their orders from the Netherlands increased by almost 80% (source: Stripe’s report “The state of European checkouts in 2020”).

Obstacles to the development of e-wallets

As it stands, iPhone users cannot use their e-wallet to make payments in some European countries because the majority of national banks have not yet implemented Apple Pay. This is particularly the case in Belgium, where only one of the major financial institutions, BNP Paribas, Fortis, offers the service. In France, 90% of banks have an agreement with Apple.

Digital wallets supporting QR codes have a weakness when it comes to further penetrating the market in Europe: a lack of the appropriate equipment able to support this technology at points of sale. With the exception of supermarket-type integrated POS system with barcode scanners that can read QR codes, the merchant must invest in a suitable device (POS terminal) to scan or generate a QR code. This equipment can be 20% more expensive than terminal models without this technology.

For contactless payment at the point of sale, the POS terminal must accept this feature. In France, this payment method is in high demand today. It accounted for 20% of purchases before the Covid-19 outbreak, but is only offered by 70% of local retailers, according to the Groupement des Cartes Bancaires.

Finally, only 70% of e-commerce sites are able to accept payments using these e-wallets. Not all merchants have flexible solutions that can onboard all payment solutions, so they need to review their partnerships with their payment gateway to enable the appropriate e-wallets to be accepted.

Changes in customer journeys

With the closure of many points of sale during the Covid-19 outbreak, and the ongoing issues surrounding in-store social distancing, consumption patterns have been profoundly disrupted. This set of circumstances will accelerate the evolution of the purchasing journey. Retailers and their providers have had to rethink experiences in order to cope with these constraints. E-commerce, drive-throughs, and click & collect were widely accepted, but these digital solutions were not the only ones to be popular with retailers.

With Paybylink, a store or a call center can simply create an online payment page after taking an order and automatically send the link by email, SMS or QR code for payment. The way in which products are made available will then vary, with either in-store pick-up or home delivery. Many stakeholders are positioning themselves on this topic. These include Adyen, Stripe, SSP, Paytweak, Worldline…

With the acceptance of cash becoming more limited, retailers have quickly equipped many of their outlets, or employees if they are making deliveries, with mobile points of sale (mPOS). These products have been growing in popularity rapidly over the past few years and are gradually moving toward technologies that accept the integration of an application on a mobile phone, enabling it to become a payment terminal (TapOnPhone). Many proofs of concept are pending until the PCI Security Standards Council releases its certification specifications.

Against this backdrop of research into innovations in online payments, the four credit card giants – Visa, Mastercard, American Express and Discover – joined together in 2019 to create a “click-to-pay” option for online shopping sites. The aim is to provide a more convenient way to pay for online purchases without having to enter payment card information, while securing the transaction. This system aims to reduce fraud in the e-commerce environment, like the EMV chip does at a physical point of sale. The experience is very similar to the PayPal payment process; the consumer only enters their details once via this system and can log into their payment account when the click-to-pay logo appears, and then choose their stored payment card.

What does the future hold for credit cards around the world?

Despite the significant breakthrough in digital wallets, cards remain the preferred payment method for most consumers. As a result, banking institutions are investing in the development of a new generation of cards.

The first to begin testing secure credit cards with biometrics, using fingerprint recognition, was NatWest last year. Thanks to a biometric sensor, the cardholder will be able to pay by validating their purchase with their digital fingerprint, and without any ceiling limit. The appetite for this technology was strong before the COVID-19 outbreak and it looks like it should be highly successful as soon as it is available on the market. In France, BNP Paribas, Crédit Agricole and Société Générale plan to launch biometric cards by the end of the year, having tested them with their employees in recent months. BNP Paribas is also planning a card with a fingerprint sensor for the end of 2020. It should reduce the risks of fraud for cardholders by using an “anti-contactless” system to reassure those who are the most resistant when it comes to contactless payment.

Requests for virtual cards are increasing for personal and professional uses: it is delivered instantaneously to customers remotely without any irksome administrative procedures. Such a card can be linked to both the local and international mobile wallets. In France, Société Générale has launched the Instant Digital Card – IDC, in partnership with Apple, with Android versions set to be made available by the end of the year. This totally virtual card enables any customer who has canceled their card to have a digitized version of their future card on their cell phone, which can be used immediately.

Banks are accelerating their process of digitization and are proposing more attractive offers by combining card and payment technologies with value-added services such as instant online loans, deposits and multi-currency transactions.

The number of cross-border transactions is growing significantly. In France, 61% of the leading sites now sell internationally and 27% have a presence in international markets, based on the latest statistics from the French Federation of E-commerce and Distance Selling (FEVAD). Offered primarily by online banks or neobanks, such as Revolut or N26, multi-currency cards enable their holders to make very large savings on overseas transactions. The principle is to link several accounts in different currencies to the same card. They are fed by money transfer. This product increases the transparency of cross-border payments by communicating the exchange rates applied at the time of payment to the cardholder. The bank derives its revenues from conversion of the currencies that it buys directly on the stock exchange or online through a partner.

Read our new Payments Report – Shifting to faster payments

Redbridge’s 2020 Payment Report is a source for trends and insights into today’s dynamic payments environment. This second edition presents how various stakeholders position themselves in the payments industry and explores topics related to innovative payments, instant payments, e-commerce and fraud mitigation.

Contributions from treasury practitioners, bankers, payment service providers and vendors are coupled with in-depth analysis from our treasury consultants.

Included in our review:

- Analysis: An overview on the future of payment

- Analysis: E-commerce, a strategy to maximize sales while limiting fraud

- Instant payment survey with banks, vendors and PSPs

As well as our interviews with:

- Michel Yvon, Decathlon

- Charles Lutran, Criteo

- Isabelle Olivier, SWIFT